The economic commentariat gave mixed reviews, with Royal Bank of Scotland saying the result was reasonable whilst Goldman Sachs think it was weaker than expected. However, profit in all segments of Qantas improved on last years result so the market loved it – with shares jumping 5%. But is this exuberance justified?

No, not really – and a little fundamental analysis will tell us why.

Firstly Qantas has a habit of creating new definitions of profit, from the standard Earnings Before Interest and Tax (EBIT) to Profit before Tax (PBT) and “Underlying” PBT. None of these include income tax and some exclude hedging and currency movements – which as far as this blogger is concerned do not constitute abnormal items for an international airline.

Probing the financial results, we find the 2010 calendar year yielded $114M profit after tax, hedging and currency movements. This is a decent improvement on the $2M loss from the previous year, but anything is better than a loss. And coming from an equity base of almost $6 billion, 2010’s result looks even shabbier.

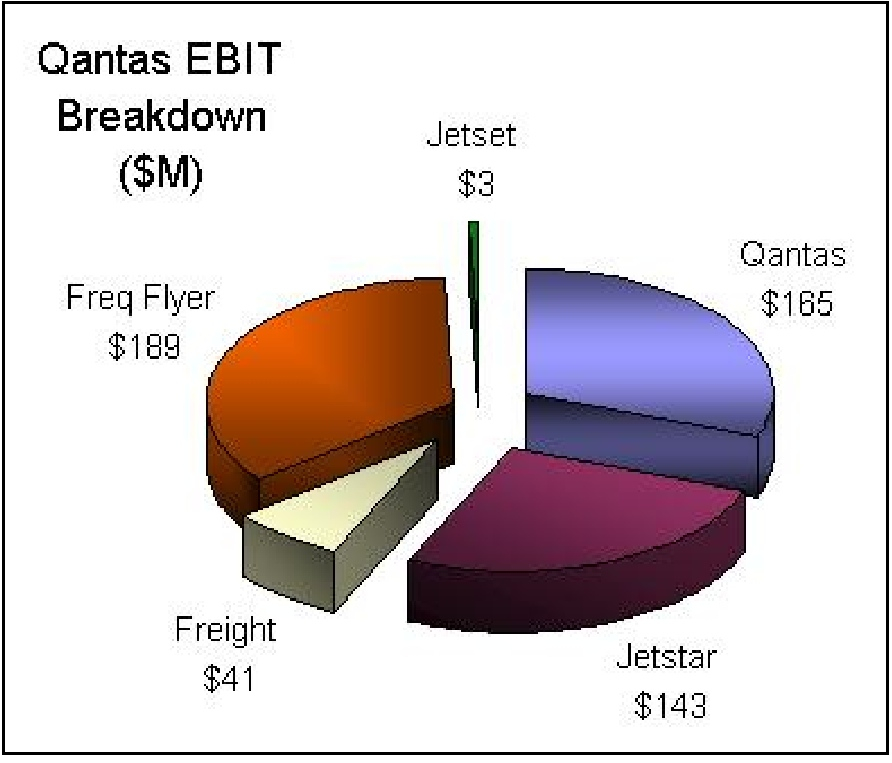

Secondly, the composition of Qantas’ revenue reveals a startling fact in the following graph:

According to the 2010 segment breakdown, the carrier now earns more money from its Frequent Flyer programs than it does from either Jetstar or Qantas operations. The Woolworths-linked points program brought in $189M (pre-tax) in 2010 versus $143M for Jetstar and $165M for Qantas.

In other words, Qantas is becoming a points program with two airlines attached to it. Strange times indeed.

Thirdly, CEO Alan Joyce has recently questioned the viability of his own full-service business. He claims capacity-dumping on Australian routes by protected foreign airlines is destroying Qantas revenues. A fact highlighted further by Jetstar’s continuing out-performance of it’s full-service brother. Throw in rising fuel costs, a sluggish home economy, troublesome Rolls-Royce engines and an upcoming EBA negotiation (covering about 1/3 of the workforce) and Qantas has a lot of headwinds.

Oh yeah – there’s also no dividend this year.

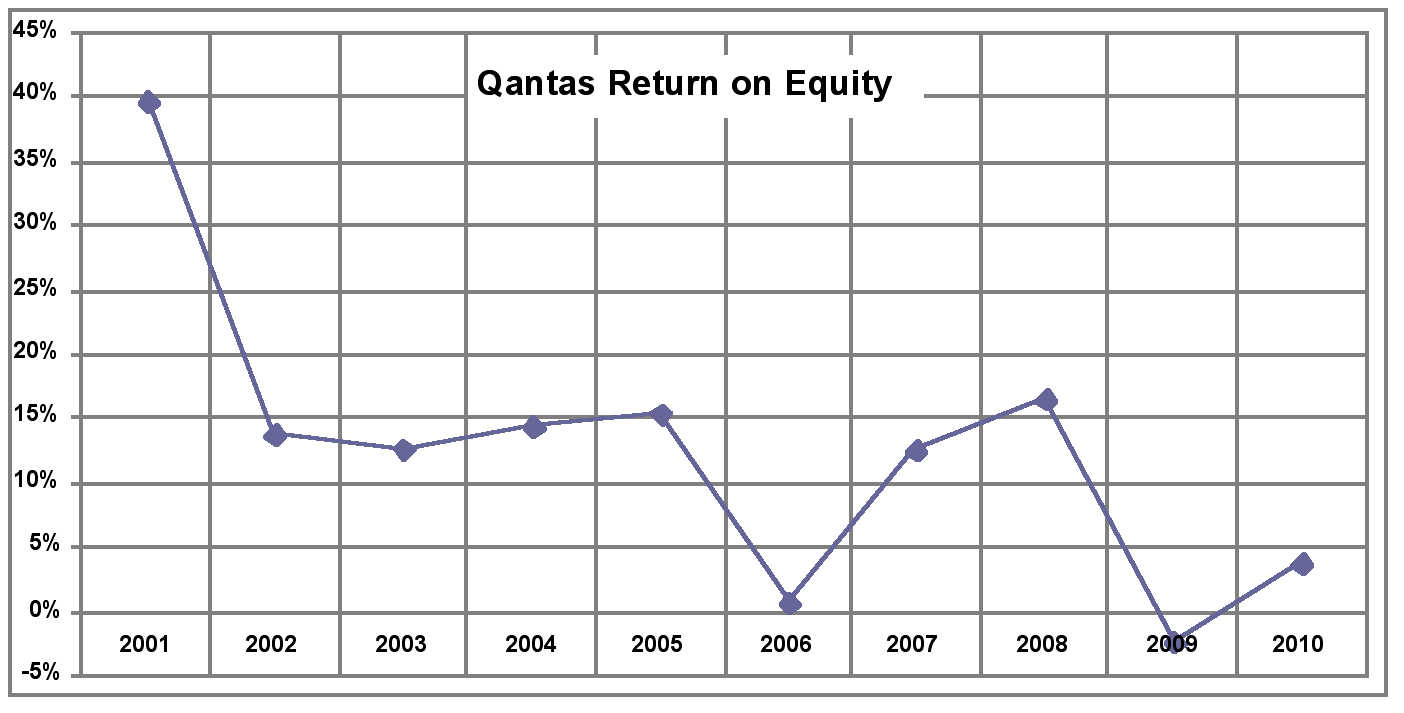

Nonetheless, it seems these issues are being ignored by the market, which seems to be predicting higher profits into the future. To see how well placed this faith is, we should take a look at Qantas’ historical performance.

Since 2002, QAN return on equity (ROE) has averaged about 10%:

For an airline this result is actually far superior to most others around the world, although in absolute terms it is pretty average. The likes of Woolworths or Cochlear average well above the 30% mark year in, year out. So from an investor point of view there are higher-yielding, lower risk shares out there.

However, when we delve deeper we find the ROE has actually been inflated by Qantas’ habit of destroying shareholder wealth. At the start of 2001, the equity base was $2.8 billion ($3.6B in today’s dollars – or no change at all if you are Gittins!).

By the end of 2010, equity was $5.9B – an increase of $2.3B. However during that 10 year period, $3.3B of new equity was added to the company through capital raisings, employee benefits and dividend reinvestment plans. That’s $1B more than the increase in equity. This means that over 10 years, $1 billion dollars of shareholder wealth was destroyed inside Qantas.

If we look at this through a dividend perspective, approximately one quarter of all dividends paid over the last 10 years were directly stolen from investor capital and not generated by the business. Had Qantas reduced their dividend payout, the capital may have been retained within the company but both ROE and dividends would have been slashed. Either way – not a good outcome – which is reflected in a share price that has decreased from $3.42 to $2.39 over a decade.

So, despite our love for the Flying Kangaroo, Qantas is still a bad investment. A decade of operations has destroyed both shareholder funds and the share price. And all the frequent flyer points in the world won’t change that. Whilst some analysts regard this as a share worth purchasing, I’d stay very, very far away. Unless you want to follow Richards Branson’s advice on becoming a millionaire:

“..start out as a billionaire and then buy an airline”.