What few seem to appreciate, either inside or outside of Japan, is just how strong the resulting Japanese recovery from 2002-2008 was. It was the longest unbroken recovery of Japan’s postwar history, and, while not as strong as pre-bubble Japanese performance, was in fact stronger than the growth in comparable economies even when fuelled by their own bubbles.

How on Earth did Japan manage that with their ageing population and zero population growth? Indeed, Japan outperformed Australia in productivity growth since 2000 and very nearly kept pace with real GDP per capita growth.

Australia’s average annual real growth in GDP per capita since 2000 is 1.28%. While I can’t find a direct measure from the Japanese Statistical agency, using the World Bank data collection I can make a comparison of real GDP growth per capita of Australia and Japan using a common methodology. Using these statistics I find that Australia had a mean annual growth in real GDP per person since 2000 of 1.8% while Japan’s was 1.4%.

Notice in the graph, however, that Australia’s growth in real GDP per capita fell considerable from 2004, when population growth rates began to push up from 1.2% to a peak of 2.16% in 2008. Since 2002, when Japan’s real growth per person increased, the population growth rate declined from 0.2% the preceding 2 years to near zero (average 2003-2008 is -0.002%) till the financial crisis hit at the end of 2007.

Australia’s economic performance is terms of productivity growth looks pitiful in comparison to Japan. Average annual Total Factor Productivity growth since 2000 was a shy 0.47% (including a productivity recession in 2004-05) while Japan recorded a strong 1.77% over the same period (data from OECD here).

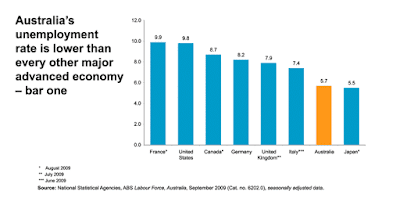

Of course there is always unemployment to consider. The graph below shows that on this measure, Australia is also behind Japan (having been in front for just the period 2007-2008). Some longitudinal data is here.

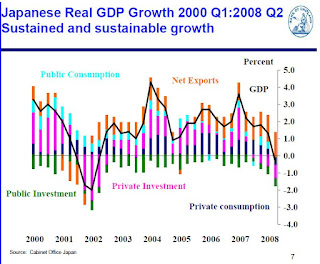

Recent research also suggests that Japan’s economic track record was unfairly blemished by asset price deflation followed by short recessions in the 1990s (1993, 1997 and 1998). The graph below (from here – including 20yr data set), shows Japan’s solid performance over the past decade, with their longest boom since WWII occurring from 2002-2008.

It appears that turning Japanese is not the tragedy it is made out to be by popular economic commentators. Here’s just one example of the popular perception-

As it turned out, Japanese investors lost nominal wealth equal to three entire years’ GDP. And the economy today hasn’t grown in 17 years or created a single new job.

Nor has the debt been reduced. Instead of permitting the private sector to destroy and pay off its debt, the public sector fought against it…borrowing heavily to try to bring about a recovery. Result: no recovery…and almost exactly the same amount of debt. But while the private sector paid off its debt, the public sector picked up the borrowing. Now it’s the government that owes money all over town.

Detractors cite the massive and growing public debt in Japan as a problem. But if the debt is denominated in Yen, and interest rates are set near zero, the burden from the debt is minimal. In fact, Modern Monetary theorists might claim public debt in ones own currency is never a burden because government can enact future policys to pay down debt with freshly printed money. I’ll leave that particulars of this option to a future MMT debate.

The above graph confirms that Japanese government debt has replaced a substantial portion of private debt since the early 1990s. In my view this is a justified effort to keep the value of the yen stable by maintaining money in circulation – an approach that could be adopted in Australia in the coming decade, with government debt replacing household debt for the same reason.

One must keep in mind that it is probably not the intention of the Japanese government to ever pay off this debt. I am sure they are happy to continue to progress with a high savings rate, high productivity, high GDP, net exports and almost every other fundamental ingredient for economic success. Turning Japanese appears to be about fundamental economic prosperity cradled in an unfamiliar monetary framework.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin