Yesterday’s speech by the RBA’s Luci Ellis had some high points. Her reference to rent-seeking behaviour in the property and finance industries was a pleasure to read. I hope this reflects likely future efforts for more scrutiny of the industry by the RBA.

It was disappointing, if not unexpected, that Ellis continued to repeat the wrong-headed explanation for high prices most often pushed by a wide collection of vested interests, that a once-off macroeconomic adjustment to a low interest rate environment and inadequate housing supply is the cause:

Lower inflation means lower nominal interest rates. Households can then service larger mortgages with the same repayment. So of course the sustainable ratio of household debt to income has risen. Housing prices followed suit, having previously been constrained in the 1970s and 1980s by the same strictures – high nominal rates and regulation. Businesses can also service larger loans out of the same stream of gross profits.

The RBA covered the second part of this conceptually poor approach in their recent research paper. But the idea that current house prices are justified by a once-off adjustment to a low interest rate environment doesn’t stack up however many times it gets repeated.

While there is undoubtedly some truth in the idea that lower interest rates lead to higher asset prices, ceteris paribus, there is a considerable leap of faith required to use this idea as a justification for current price levels.

We can demonstrate the principle easily enough. Prior to the structural adjustment in interest rates, a buyer looking to buy a home that rents for $15,000pa, who is willing to pay a 20% over the cost of renting to buy the home, would capitalise $18,000 at the going rate of 12.8% (the average mortgage rate between 1982 and 1994). That’s a price of $140,625. After a structural adjustment, the cost would be capitalised at 7.3% (average mortgage rate since 1995), giving a price of $246,575. A 75% real price increase should be close to as sustainable as the previous price. That’s rough and ready as there is a consideration of the serviceability of repaying the loan capital as well. If we consider the costs of servicing a 30 year mortgage, a 58% gain is justified from new interest rate conditions.

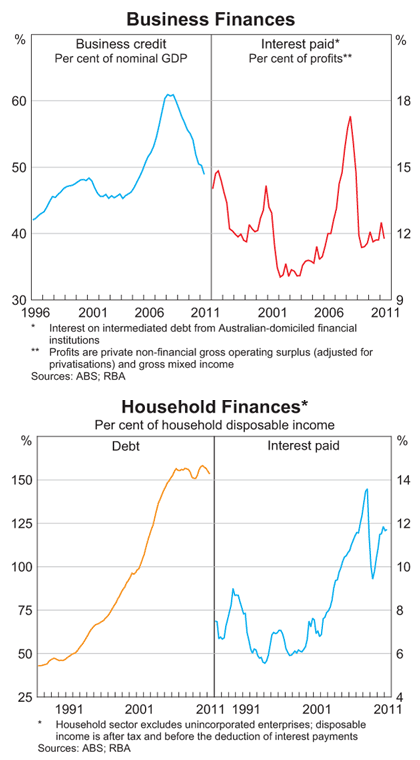

One piece of evidence to show just how much higher house prices are than is justified by the interest rate environment is in the charts below from the RBA’s own chart pack. The lower right panel shows that interest paid as a proportion of household income increased from around 6% in the 1990s to 12% currently (after reaching a peak of 14% in 2007). If the increased debt taken on, and associated price increases were due to interest rate conditions alone, the interest paid should have remained flat as a proportion of income. The fact that it has doubled indicates that around half of the current level of housing debt is not justified at all by this measure:

The ABS home price figures (though not ideal for this purpose) suggest that real home prices gained over120% since 1996. That’s far greater than what is expected from interest rate conditions alone.

To get back to that ‘sustainable’ point, either home prices need to fall by close to 30%, or interest rates need to fall by around 30% (mortgage rates to 4-5%), or some combination of the two (noting also the geographical disparity any correction is likely to have).

The top panel above demonstrates that business credit, which faced the same macroeconomic environment of declining interest rates and inflation, followed a much different pattern. While business credit did grow by around 30% as a proportion of GDP, and interest did surge as a proportion of profits, these indicators are currently falling back in line with historic trends.

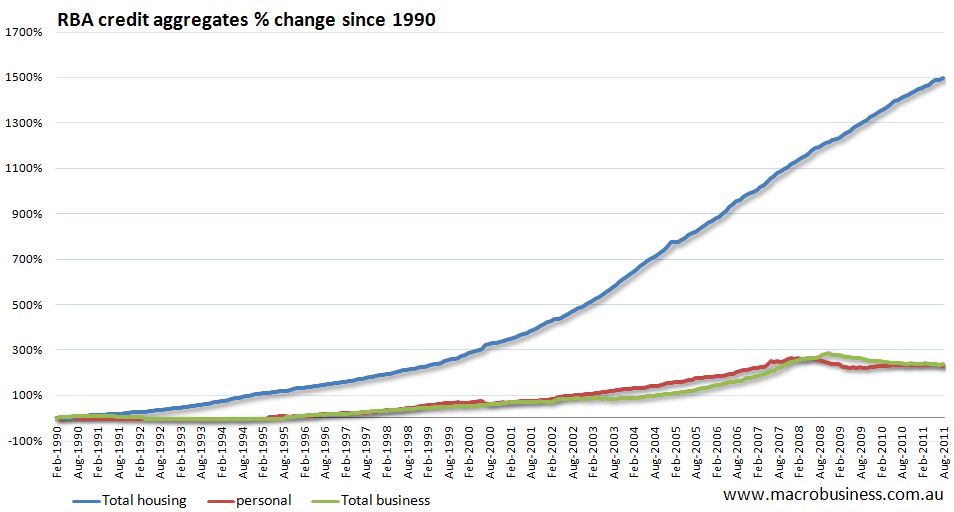

Finally, the graph below shows most clearly the divergence in credit trends between households and businesses since the early 1990s adjustment. If that doesn’t convince you that the RBA and vested interests are repeating a simple falsehood, then nothing will.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin