RBA researchers released a paper yesterday modelling urban structure and house prices under conditions of population growth, zoning controls, and the provision of transport infrastructure. They use an Alonso-Muth-Mills model to demonstrate typical location, density and rent effects of housing in a mono-centric single land use disk-shaped model of a city (in fact their geographical scope is a hemisphere).

Given the debate surrounding price impacts of planning regulation on housing, this research input from our favourite central bank should be of some importance. However the gaping chasm between their descriptive model, the empirical evidence, and their policy conclusions leaves me concerned. The model doesn’t have legs.

While this partial equilibrium model is a valuable tool to describe relative rents due to transport costs given a mono-centric, mono-sector city (housing only), I suggest that the assumptions required make it a poor tool for analysing changes to the parameters. Particularly, the following assumptions justify extreme caution when translating the model estimates to policy suggestions.

- The wage rate and the rental rate on capital are taken as exogenous

- The price of land at the city fringe is equal to the cost when used in agriculture

- The units of this figure and subsequent ones are as follows: housing (rental) prices in dollars per square metre of living space per year… The model refers to the rental price of housing and land, but under an assumption of a given capitalisation rate, these translate directly to purchase prices, which we refer to in our discussion.

Like all models, the outcomes are set by the assumptions, so let’s consider each in turn.

First, the model suggests that wages do not respond to increased housing costs in a city. While reality may be imperfect, with migration choices available to other cities one would expect that wage differentials between cities reflect housing costs differentials to some degree. If house prices in Brisbane rise relative to other cities while wages stay constant, it makes Brisbane a less desirable city to live. As people are attracted by better real wages in other cities (and globally), it provides feedback from house prices or rents to wages.

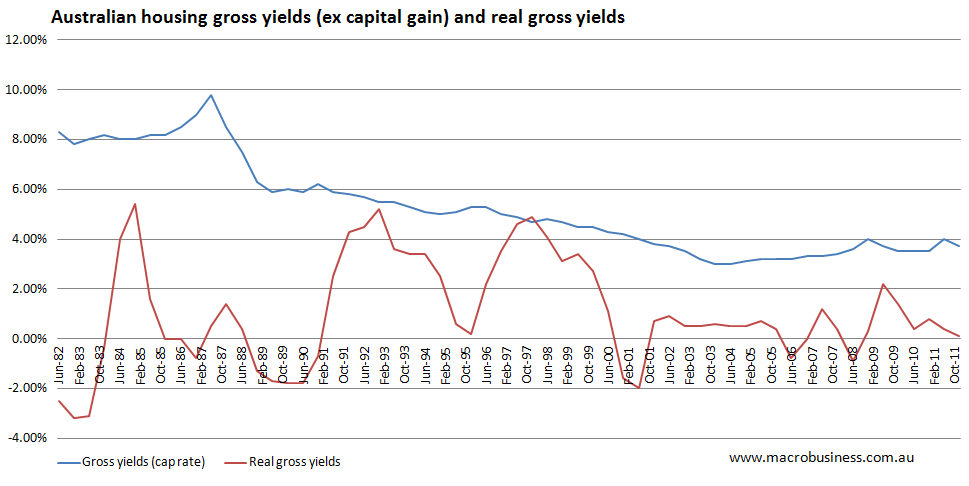

Second, the ‘rental rate on capital is taken as exogenous’ and ‘the assumption of a given capitalisation rate’ means that the yield is fixed. In fact it implies that the real yield on a per sqm of dwelling basis is fixed. This allows rent to be used as a proxy for prices. But reality has been nothing like this assumption would imply. The graph below shows the changes in real and nominal yields over time which need to be considered in the translation between modelled real per sqm rents and nominal prices.

Indeed it is quite odd to develop a model of per sqm rents, and then write a chapter entitled Empirical Evidence, and not examine the patterns of rental prices for housing on a per square metre basis – which is what the model itself actually estimates.

In fact the paper doesn’t publish impacts from increased transport costs, increased population and zoning changes on median rents (which could be calculated from model outcomes). Rather it shows a graphical presentation of impact on geographical rental gradients. If density restrictions lead to more people living in fringe areas (as shown in the second graph below), the changing composition of dwellings may leave the median (and mean) citywide rent unchanged even though the rents at each location are higher. I have demonstrated this composition effect before using the table below.

![]()

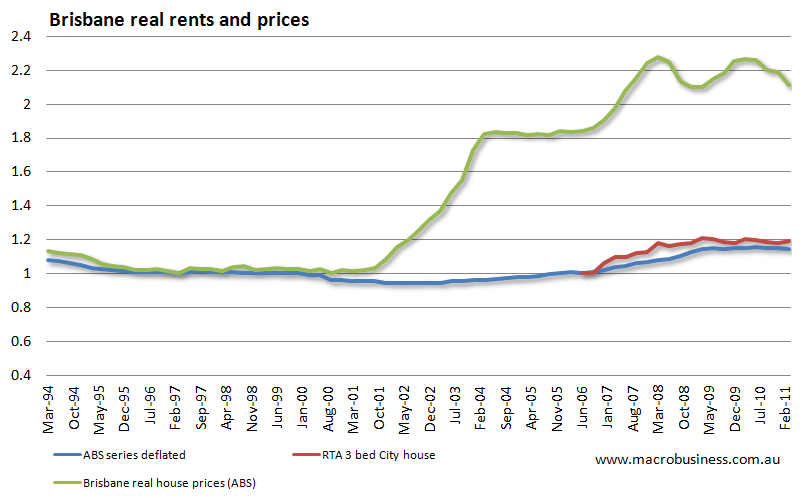

Further, empirical evidence seems to suggest that Australian rents have been relatively stable, and indeed were declining in real terms for a decade prior to 2003. The chart below shows Brisbane rents and prices from ABS data, which does have quality adjustment in rents. However, given that the model itself is quality adjusted (using rents on a per sqm basis), I expect this to be a reasonable presentation of the intended modelled measures. RTA data trends in rent prices for recent bond lodgements traces this trend almost exactly from 2006 when the data is first available. Similar trends are observed in other capitals.

The next assumption of marginal fringe land supply at agricultural rents is a little strange, since many of the arguments surrounding housing supply constraints use as evidence the difference between agricultural land values and fringe residential land values. So having a model where this cannot occur seems at odd with other arguments surrounding housing supply price impacts. The fact that the model is has no competing land uses within the city limits is another factor likely to skew results towards steeper rent gradients between inner and fringe locations.

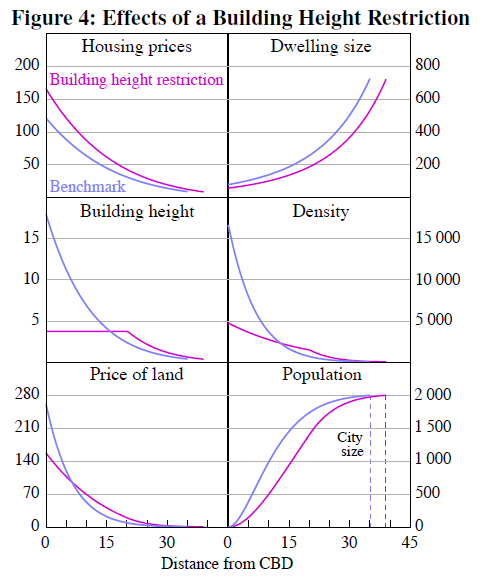

For me, the finding that “there is a trade-off between density and housing prices” is peculiar. Their model suggests the opposite is the case (see graph below), with lower density creating higher prices. Even though I think the model is flawed, the commentary accompanying this conclusion confuses the issue.

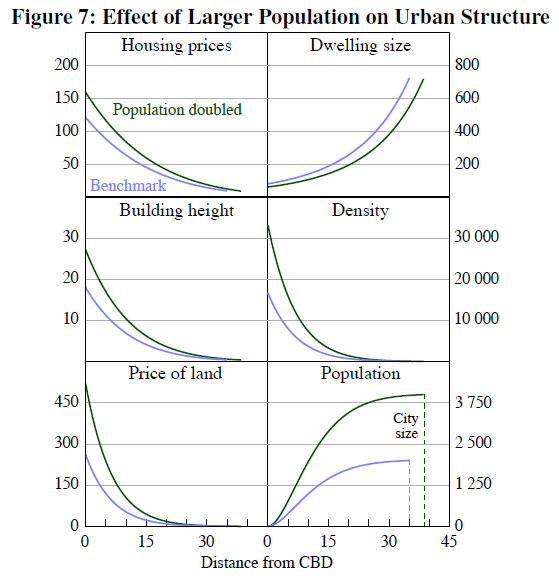

Additionally, the comparison of price impacts due to population growth simply compares two static ‘equilibrium’ conditions under the same model calibration with double the population. The results of this comparison are in the graph below.

The question one asks is that if there is no constraint on density other than construction costs, and no constraint on urban sprawl other than transport costs, how can equilibrium rents increase for a population with the same income level?

The answer is found in the model parameters that define the equilibrium conditions for profitable dwelling supply (as per the model calibration on p37). This arbitrarily limits the scale of housing construction, and there is no argument why this parameter would be constant when comparing two real world cities of different populations with the same income.

The researchers also note the lack of evidence of price impacts of zoning in the academic literature. Their paper cites numerous articles suggesting that zoning, density and land use controls can be effectively implemented without price effects if they provide adequate scope for markets to operate. I suggest this has been the case in Australia for some time.

Given the importance of the paper’s conclusions to planning regulation, one might consider that a better use of the model would be to determine whether ‘real life’ planning tools actually generate the patterns the model suggests. We could then determine the degree of impact that current planning tools have on home prices compared to model estimates (even given its various constraints).

It bothers me that our central bank, with its influential standing in the policy community, can release research with such obvious flaws. I prefer models with legs.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin