Australian Data

TD Inflation Index

Inflationary pressures continue to ease in Australia according to the TD-MI inflations gauge with headline inflation rising by 0.1% in September following a fall of -0.1% in August with the annual pace of inflation slowing to 2.8%. The trimmed mean index also rose by 0.1% in September with the annual rate also at 2.8%. More importantly over the past 6 months headline inflation rose at an annualised pace of 1.6% while the trimmed mean was running at an annual pace of 1.2%.

Inflationary pressures continue to ease in Australia according to the TD-MI inflations gauge with headline inflation rising by 0.1% in September following a fall of -0.1% in August with the annual pace of inflation slowing to 2.8%. The trimmed mean index also rose by 0.1% in September with the annual rate also at 2.8%. More importantly over the past 6 months headline inflation rose at an annualised pace of 1.6% while the trimmed mean was running at an annual pace of 1.2%.

Trade Balance

Australia’s trade balance continued to grow in August, hitting its second highest level on record at $3.1bln. The surge in the trade balance came as a result of an 8% surge in exports with the exports of metals, ores and minerals rising to an all time high while exports of coal and fuel both rose over the month. Imports were quite evenly spread with services, intermediate and consumption goods all rising over the month with the only sub-component to register a fall being capital goods. Exports from the QLD region through the Gladstone port are back running at their long run average through the 3rd quarter

Australia’s trade balance continued to grow in August, hitting its second highest level on record at $3.1bln. The surge in the trade balance came as a result of an 8% surge in exports with the exports of metals, ores and minerals rising to an all time high while exports of coal and fuel both rose over the month. Imports were quite evenly spread with services, intermediate and consumption goods all rising over the month with the only sub-component to register a fall being capital goods. Exports from the QLD region through the Gladstone port are back running at their long run average through the 3rd quarter

Building Approvals

Building approvals surged in August with total approvals jumping 11.4% over the month while the previous months gain of 1% was revised up to a gain of 1.8%. Public approvals fell following the sharp jump the previous month with private non housing driving the gains over the month after they increased 35% while Private housing approvals continue to slide, hitting a new post GFC low. Most states experienced a rise in approvals over the month with NSW approvals jumping by a solid 45% over the month

Building approvals surged in August with total approvals jumping 11.4% over the month while the previous months gain of 1% was revised up to a gain of 1.8%. Public approvals fell following the sharp jump the previous month with private non housing driving the gains over the month after they increased 35% while Private housing approvals continue to slide, hitting a new post GFC low. Most states experienced a rise in approvals over the month with NSW approvals jumping by a solid 45% over the month

Retail Sales

After a volatile first half of the year, retail sales have posted two solid increases back to back in July and August which is encouraging. Total sales rose by 0.6% with sales ex-food climbing 0.7% over the month however the gains are hardly uniform across sectors. Spending on food continues to outstrip the rest of retail sales which could be a sign of inflation, as anecdotally at least, many food staples appear to be getting more expensive. Sales ex-food are unchanged from a year earlier suggesting that sales ex-inflation are likely to be lower than 12 months ago. A distinct positive was that the latest rise was spread across all states fairly evenly

After a volatile first half of the year, retail sales have posted two solid increases back to back in July and August which is encouraging. Total sales rose by 0.6% with sales ex-food climbing 0.7% over the month however the gains are hardly uniform across sectors. Spending on food continues to outstrip the rest of retail sales which could be a sign of inflation, as anecdotally at least, many food staples appear to be getting more expensive. Sales ex-food are unchanged from a year earlier suggesting that sales ex-inflation are likely to be lower than 12 months ago. A distinct positive was that the latest rise was spread across all states fairly evenly

Offshore Data

US ISM

It was a mixed outcome for the ISM indices in September with the manufacturing index unexpectedly rising from 50.6 to 51.6 after it was expected to fall to 50.5 while the non-manufacturing ISM fell from 53.3 to 53.0 after it was expected to ease even further to 52.8. The employment component of the manufacturing index rose from 51.8 to 53.8 however the employment component of the non-manufacturing sector which is far more significant fell from 51.6 to 48.7, its first read below 50 since August 2010 at which time total employment was falling.

It was a mixed outcome for the ISM indices in September with the manufacturing index unexpectedly rising from 50.6 to 51.6 after it was expected to fall to 50.5 while the non-manufacturing ISM fell from 53.3 to 53.0 after it was expected to ease even further to 52.8. The employment component of the manufacturing index rose from 51.8 to 53.8 however the employment component of the non-manufacturing sector which is far more significant fell from 51.6 to 48.7, its first read below 50 since August 2010 at which time total employment was falling.

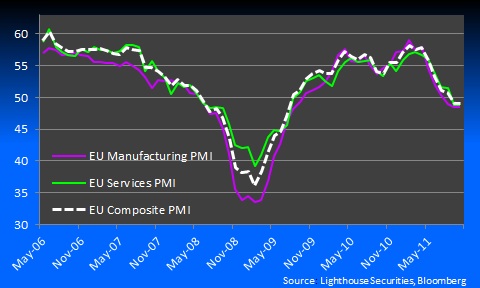

EU PMI

The final read of the EU manufacturing PMI was revised up slightly from 48.4 to 48.5 however still indicated that activity contracted during September. France and Germany’s manufacturing PMI’s were both revised up however the French index was still below 50 while the German index was revised up from 50 to 50.3. It was the polar opposite for the services PMI’s with the EU index revised down from 49.1 to 48.8 with the French index down to 51.5 from 52.5 while the German index was revised down to 49.7, indicating a contraction in activity from the previously reported 50.3.

The final read of the EU manufacturing PMI was revised up slightly from 48.4 to 48.5 however still indicated that activity contracted during September. France and Germany’s manufacturing PMI’s were both revised up however the French index was still below 50 while the German index was revised up from 50 to 50.3. It was the polar opposite for the services PMI’s with the EU index revised down from 49.1 to 48.8 with the French index down to 51.5 from 52.5 while the German index was revised down to 49.7, indicating a contraction in activity from the previously reported 50.3.

German Industrial Production

After a solid bounce in July which saw industrial production surge 3.9%, activity fell for the 3rd time in the past 4 months in August, dropping 1% which was actually better than the 2% fall that was expected. After rising 2.3% last month, consumer goods fell 4.9% in August, driven by a 10% fall in the production of durable goods while production of non durable goods was also lower, dropping 3.8%. The only sub component to rise over the month was the production of capital good which edged up 0.2%.

After a solid bounce in July which saw industrial production surge 3.9%, activity fell for the 3rd time in the past 4 months in August, dropping 1% which was actually better than the 2% fall that was expected. After rising 2.3% last month, consumer goods fell 4.9% in August, driven by a 10% fall in the production of durable goods while production of non durable goods was also lower, dropping 3.8%. The only sub component to rise over the month was the production of capital good which edged up 0.2%.

US non-farm payrolls

Jobs growth resumed in the US according to the September nonfarm payrolls report with the establishment survey showing there were an additional 103k jobs added over the month while the August stall in employment growth was revised up to show a gain of 57k and the 85k from July was revised up to 127k. The jobless rate also remained unchanged at 9.1% according to the household survey after it showed the economy adding in excess of 300k jobs for the second month. However it wasn’t all good news with the U6 underemployment rate continuing to trend higher, rising 0.3% to 16.5%. Additionally both the unemployment and underemployment rate would be higher were it not for the almost 2 million additional people classified as “not in labour force” over the past 12 months

Jobs growth resumed in the US according to the September nonfarm payrolls report with the establishment survey showing there were an additional 103k jobs added over the month while the August stall in employment growth was revised up to show a gain of 57k and the 85k from July was revised up to 127k. The jobless rate also remained unchanged at 9.1% according to the household survey after it showed the economy adding in excess of 300k jobs for the second month. However it wasn’t all good news with the U6 underemployment rate continuing to trend higher, rising 0.3% to 16.5%. Additionally both the unemployment and underemployment rate would be higher were it not for the almost 2 million additional people classified as “not in labour force” over the past 12 months

US Consumer Credit

Total consumer credit fell for the first time in almost 12 months in August, dropping 0.4% or $9.5bln on a seasonally adjusted basis. Revolving credit remained weak, falling for the second straight month, dropping $2.3bln and it has only risen 4 times in the past 3 year while non-revolving credit also fell, down $7.2bln, which was its first decline since May 2010. Non-seasonally adjusted consumer credit gre by almost $13bln with the US Government now accounting for 16% of total outstandings, the highest percentage on record.

Total consumer credit fell for the first time in almost 12 months in August, dropping 0.4% or $9.5bln on a seasonally adjusted basis. Revolving credit remained weak, falling for the second straight month, dropping $2.3bln and it has only risen 4 times in the past 3 year while non-revolving credit also fell, down $7.2bln, which was its first decline since May 2010. Non-seasonally adjusted consumer credit gre by almost $13bln with the US Government now accounting for 16% of total outstandings, the highest percentage on record.

Yours in data – The Lighthouse Team.