The S&P/ASX 200 Index closed exactly flat today at 4008.6 points. The market has dropped 0.5% in the after hours futures market, whilst Euro and US markets are also set to open down, probably on end of month and end of quarter portfolio re-adjustments.

Asian markets were mixed, Japan’s Nikkei 225 closing flat at 8700 points, whilst the Hang Seng was sold off losing 2% to 17641 points and Shanghai Composite down 0.35% to 2356 points.

In other risk assets, the AUD lost half a cent to 97.30 cents USD, whilst WTI crude climbed slightly to $82.71 USD a barrel.

Gold climbed from a pre-$1600 low and was bid up during the Asian session, currently at $1625 USD an ounce or $1673 AUD an ounce.

Movers and Shakers

A mixed day across the board on the ASX, with the biggest gains in energy and utilities, whilst healthcare and IT stocks suffered.

The banks were mainly down, although Commonwealth (CBA) was steady, ANZ lost 0.3%, NAB 0.6% and WBC down the most at 1.02% – no direction in all four cases in the short term. Macquarie (MQG) was up 1.6%

Cochlear (COH) lost another 3.76% falling to almost May 2008 lows whilst CSL slipped 0.64% providing most of the losses for the healthcare sector.

BHP Billiton (BHP) and Rio Tinto (RIO) had a mixed day, with the former steady and the latter losing 1%

Newcrest Mining (NCM) slipped slightly, whilst Fortescue (FMG) also had a mild loss, down 0.67%

Sundance (SDL) was the biggest winner on the ASX200 today, up 4.8% whilst the biggest loser was Gunns (GNS) down almost 17%.

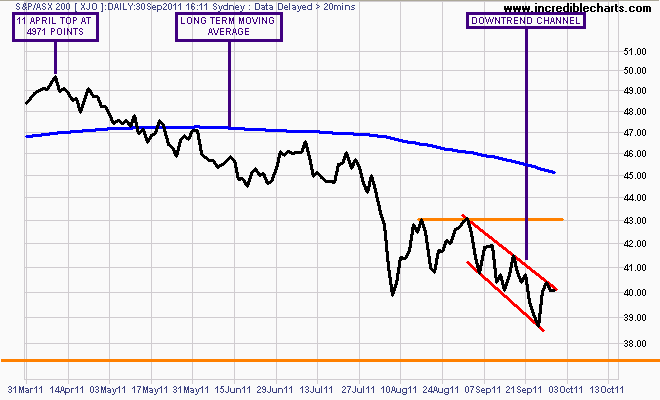

The Charts

The daily chart below shows that although price action has snuck ASX200 back into its sideways channel and above resistance at 4000 points, the whole of September has seen a downtrend channel form from the 4300 point resistance level. Again, short term momentum has not broken through its resistance level, reflecting internal resistance.

There is significant resistance at the 4300 point level, the intersection of the medium term downtrend since April (not shown for clarity) and the last 2 high’s since the broad selloff in early August.