The S&P/ASX 200 Index lost 1% or 39 points to 3863, hitting a 2 year low, after a strange and volatile day with a 50 point rally in the morning that collapsed during the day, even though the banks all put on solid gains. The answer was all that does not shine – gold.

In after hours future trading, the market is steady, whilst Euro and US futures point to similar losses. Almost all risk markets continue to be correlated with each other in timing, magnitude and direction.

Asian markets experienced slightly larger moves, Japan’s Nikkei 225 losing 1.7% to 8414 points, whilst the Hang Seng was down 1.8% at 17352 points and Shanghai Composite losing 1.6% to 2393 points.

In other risk assets, the AUD was sold off heavily again – some safe haven – and stands at 96.7 cents against the USD, whilst WTI crude slipped below the $80 USD a barrel level or 0.6% during the Asian session.

Gold has now lost 5.4% since the Asian session opened this morning, and just under 15% in 30 days, currently at $1562 USD per ounce. Silver is even worse off – down 13.5% today – and off 35% in 30 days. Crazy times.

Movers and Shakers

A very mixed day across the board on the ASX, with a lot of sectors making broad gains – healthcare and consumer sectors particularly, but it was the energy and materials hit hard, both losing 4%.

The banks were mainly fine, with Commonwealth (CBA) up over 1%, ANZ steady, NAB up 0.7% and WBC up a stonking 2.5%. Macquarie (MQG) fell again, closing just above $20 a share (yes, $20!) losing 3.3%, whilst volatile Cochlear (COH) gained 1.7% alongside its CSL brother, up 2% exactly after breaking out on the back of a weaker Swiss Franc and Aussie Dollar.

BHP Billiton (BHP) and Rio Tinto (RIO) continue to be the culprit, with the former losing 1.7% closing at just below $34 after being as high as $35.10, whilst the latter losing almost 4%, again reaching a good intraday high of $63.76 but closing just above $60. Newcrest Mining (NCM) lost a stunning 9% for the day, reflecting the gold spot price falls. Day traders love this stuff of course.

Gunns (GNS) was the biggest winner on the ASX200 today, up 13% whilst James Hardie (JHX) books 5.5% for the day.

The losers? Small caps. This is ominous. Murchison Metals (MMX) lost 19.5%, Lynas Corp (LYC) over 17% amongst a bevy of befuddled beauties. Other’s within the ASX Small Ordinaries Index include Bannerman Resources (BRM) down 21% and a host of gold, silver and oil stocks.

The Charts

We are now in new, dangerous territory. The market has closed at a 2 year low – whenever risk markets do this, thus wiping out 2 years of capital gains, they have a nasty habit of continuing to fall, as everyone capitulates, both dumb and smart money.

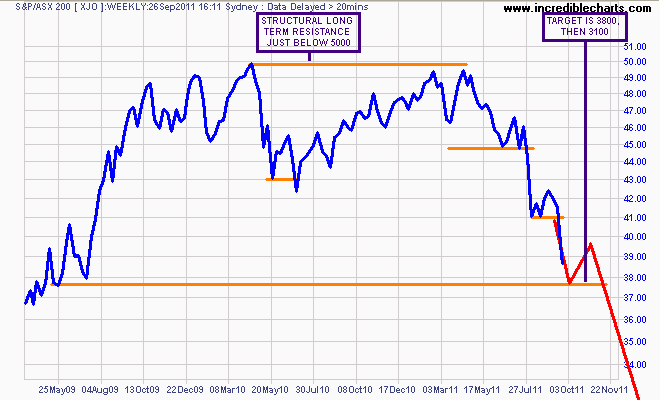

Weekly chart of ASX200

The weekly chart above shows my original plotting of a possible decline in the ASX200 and so far, the script is being followed. The lower orange line is the support level from the rebound rally of March to July 2009, just below 3800 points.

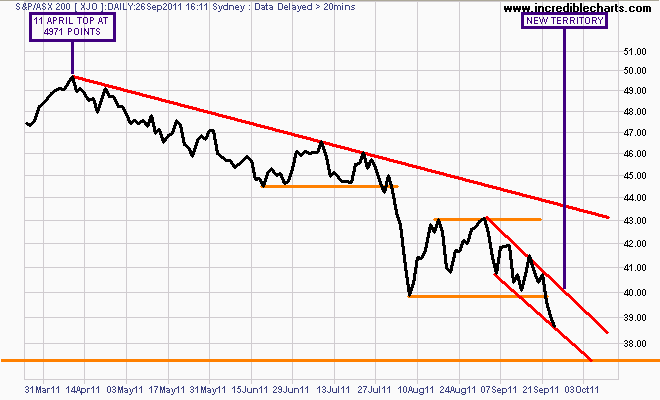

The daily chart below shows a small price channel forming, pointing towards those support levels in the short term.

Daily chart of ASX200

Overhead resistance has now shifted to 4000 points, the terminal support level throughout the sideways price movement in late August and early September that the market has now tossed aside like an economists forecast.

A rally beyond this level could go as far 4200-4300 points, on the back of any sort of good news, likely emanating from Europe. I have warned readers before that bear markets include significant rallies – sometimes over 20% as ebullient bulls come back out of the woodwork exclaiming all is well.

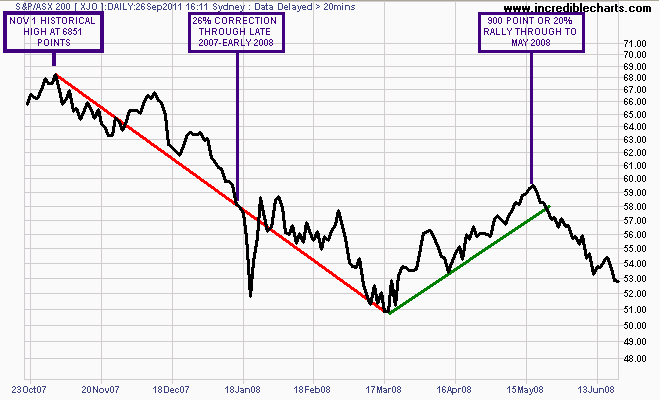

I might just add that one such rally occurred during the GFC, after correcting some 26% from the November 2007 highs, including some epic daily volatility the market rallied 900 points or 20% through to May 2008.

Daily chart from late 2007 to May 2008 - similar volatility to now, at least on the downside

We all know what happened after that, and even though Greece may well be “profligate and dishonest” (although I note that the same could be said for German and French bankers), it has more debt and interconnectedness with world markets than Lehman Brothers.