The S&P/ASX 200 Index lost 1.5% or 57 points to 3907, after a volatile day from absorbing last night’s crash across Euro and US markets and a “statement” from the G-20. In after hours future trading, the market is slipping below 3900, whilst Euro and US futures point to some minor gains.

Asian markets experienced similar moves, Japan’s Nikkei 225 shut for a public holiday, but futures pointing to a 90-100 point loss, whilst the Hang Seng was down 1.8% at 17564 points.

In other risk assets, the AUD was sold off again and stands at 97.7 cents against the USD, whilst WTI crude slipped half a percent to just above $80 USD a barrel after getting pummeled overnight.

Gold has slipped again and is now at $1726 USD per ounce.

Movers and Shakers

Surprisingly, a mixed day across the board on the ASX, with healthcare and consumer sectors actually gaining, whilst energies and materials were heavily sold off.

The banks were mixed, with Commonwealth (CBA) up over 1% whilst the rest lost between 0.8% and 2%. Macquarie (MQG) fell 1.5% whilst volatile Cochlear (COH) saw a large trading range going as low as $48.30 before closing just below $50 a share.

Nexus (NXS) was the biggest winner on the ASX200 today, up 29% on a rebound from board gyrations and Bluescope Steel (BSL) rallied over 6%, probably on the weakening AUD (higher dollar does more damage than a carbon tax remember).

BHP Billiton (BHP) was down almost 3%, reflecting the selloff in metals and energy commodities last night, whilst Rio Tinto (RIO) dropped 3.5%.

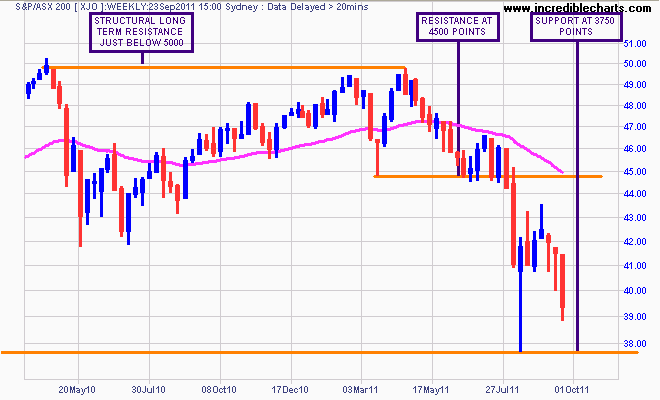

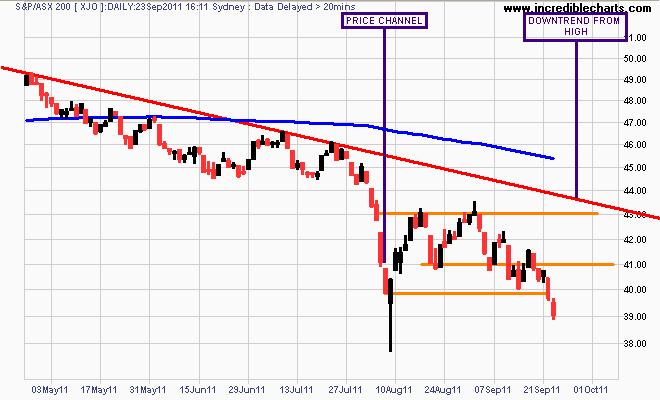

The Charts – updated with closing chart (h/t outsidetrader)

The daily chart below shows how today and yesterday’s price action sits below the closing low of August 8th selloff, but not the intra-day low on the following “epic” day. Note too that today’s action has a small tail, which indicates some intraday buying support from a low, but this is not a clear sign of a bullish bias and just a reaction to the G-20 communiqué.

The weekly chart shows the depth of the decline, which in previous weeks did include serious buying to try to support prices (the long lower tails), but the bulls capitulated. The next target level is 3750 points, which may be reached after a short-covering rally or any good news that comes out of Brussels or Washington tonight.

The weekly chart shows the depth of the decline, which in previous weeks did include serious buying to try to support prices (the long lower tails), but the bulls capitulated. The next target level is 3750 points, which may be reached after a short-covering rally or any good news that comes out of Brussels or Washington tonight. Overhead resistance remains at 4100 points, the former support level throughout most of the sideways price movement in late August, early September, although a rally up to 4200 points is conceivable, but it would not bring the dominant downtrend to a conclusion just yet. Readers must remind themselves that bear markets include significant rallies – sometimes over 20% as ebullient bulls come back out of the woodwork exclaiming all is well. And then the trend resumes.