The S&P/ASX 200 Index closed down 1% or 41 points to 4040, after recovering some mild losses in the morning, slipped after lunch on news of Italy’s rating downgrade and RBA minutes indigestion. In after hours future trading, the market has slipped another 5 points whilst the Euro and US futures point to similar losses.

Asian markets experienced similar moves, Japan’s Nikkei 225 closed down 1.6% to 8721 points, whilst the Hang Seng was down 0.3% at 18863 points.

In other risk assets, the AUD slipped and fell below 1.02, and is at 1.0197 whilst WTI crude slipped too, only falling 0.15% to $85.60 USD per barrel.

Gold suffered a 5 minute drubbing last night, falling almost $50 an ounce in the NY trading session to $1770 an ounce and came back to $1780 through the Asian session, before falling again to $1770 prior to London trading.

Movers and Shakers

Another red day across the board on the ASX, with materials and financial sectors the biggest losers, with healthcare and consumer sectors rising slightly, mainly due to a strong day by CSL, up nearly 3%.

The banks were all sold off between 0.5% and 2.3%, with NAB the biggest loser, ANZ the smallest. Macquarie (MQG) slumped 2.3% whilst volatile Cochlear (COH) lost almost 4% after rebounding yesterday. Platinum Australia (PLA) was the biggest loser in the ASX200, down almost 8% for the day.

BHP Billiton (BHP) lost over 2% alongside Rio Tinto (RIO) just under 2% whilst gold miner Newcrest (NCM) gained half a percent.

The Charts

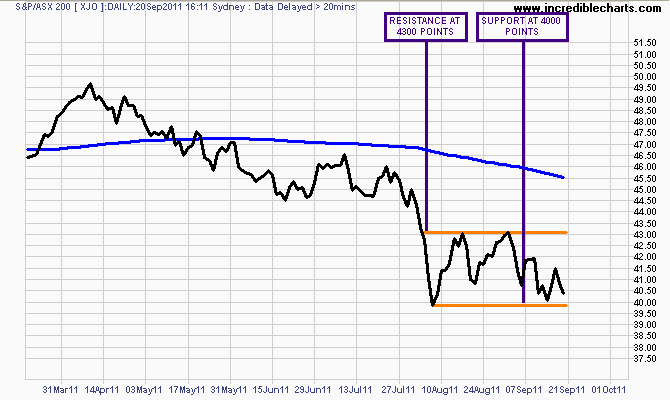

The short term daily pattern is very close to the bottom of a sideways price channel with support at 4000 and resistance at 4300 points.

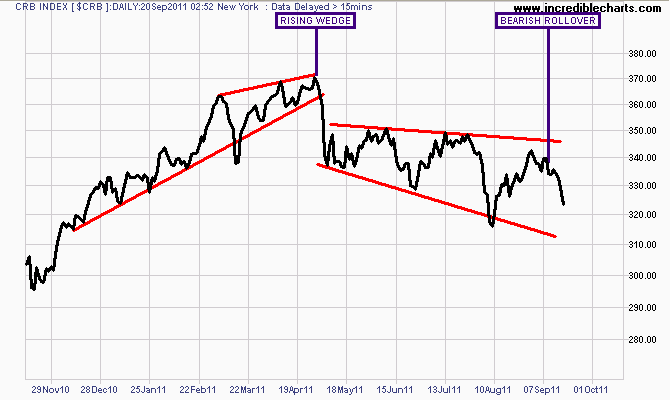

The medium and long term patterns are still bearish and more importantly, Euro and US markets are forming bear reversal patterns on the back of their ongoing debt crisis – bad for the “houses” part of the ASX200. The CRB Commodity Index has rolled over, which is bad news for the “holes” part of the ASX200.