The S&P/ASX 200 finished flat today, up 4 points or 0.1% to 4188 points after a volatile session where it breached 4200 points before a disappointing jobs data release. In after hours trading, the market is just holding on to these gains awaiting the Euro and US sessions, which will likely react to both Ben Bernanke and Barack Obama’s speeches.

Asian markets experienced mixed results, with the Nikkei 225 up 0.3% to 8793 points whilst the Hang Seng closed down 0.65% to 19917 points.

In other risk assets, the AUD slumped immediately on the poor jobs data, with traders factoring in no further rate rises for sometime, and finished down 0.64% at 1.0593, whilst WTI crude steadied on its overnight reversal to $89.51 USD per barrel.

Gold has regained after a volatile week, up 1.5% to $1844 USD an ounce with strong intra-day bids across the Asian session.

Movers and Shakers

A mixed board on the ASX, with half sectors down and half up, consumer stocks the biggest losers whilst IT and energy stocks outperformed.

The banks were mixed, with ANZ and CBA slipping 0.5% each whilst NAB climbed 1.2% and WBC steady. Macquarie gave back yesterdays gains and closed down 1.4% to just over $23

BHP Billiton (BHP) slipped 0.16%, mirroring the index, whilst RIO gained almost 1 percent.

The Charts

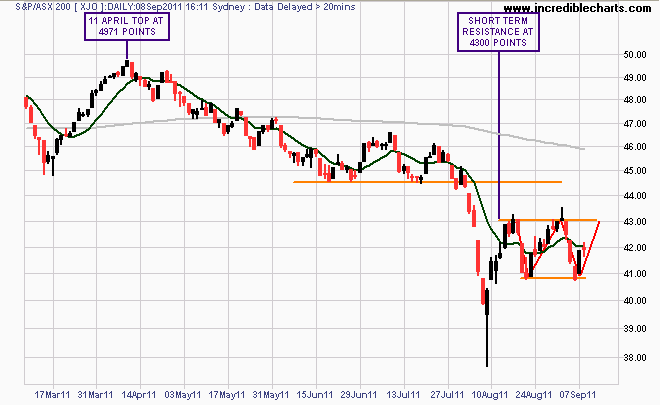

Bullish medium term investors and traders still need to look for a sideway channel pattern between 4100 and 4300 points to eventuate before considering positions, similar to the pre-QE2 action of last year.

Today’s action has stalled the momentum of any rebound rally and reflects the doubts in the minds of those who bought at these “cheap” levels. Volume remains weak and the medium term downtrend is still well in place.