As the readers of MacroBusiness would know, we’ve been banging on about Dutch disease in the Australian economy for some time. Namely, the higher Australian dollar (that results from our commodities boom and the weakness of other nations currencies) is hampering our manufacturing and export sectors. This viewpoint was reinforced by a recent round of job losses from Bluescope and Onesteel, with companies like CSR reportedly following suit.

It’s a simple equation really – as the AUD climbs, imports become cheaper and our exports get more expensive. This means Aussie exporters are finding it hard selling their now-expensive goods in the global market. The same applies for tourism and education – Australia is now a more expensive place to holiday and get a bachelors degree. On the flipside, imports into Oz are now cheaper (here I come Amazon and bookdepository!) so local manufacturers are dropping margins in order to stay competitive.

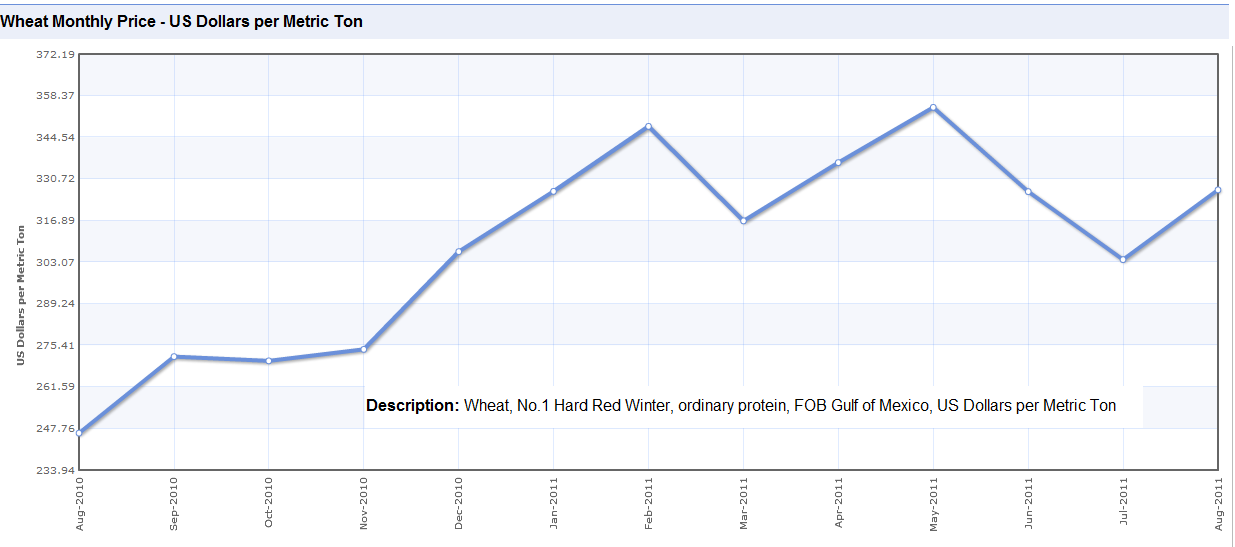

The only exporting exceptions to this situation are the mining and agriculture sectors. Despite the higher AUD, the prices of their products (hard and soft commodities) have been increasing more than the AUD, so profits are up. I’ve covered the mining side before when examining BHP, whilst the chart below shows the monthly wheat price in USD over the last 12 months (courtesy of www.indexmundi.com). A welcome trend for wheat farmers.

Aren’t there any winners from the high AUD?

Surely the high AUD must create some winners in our diverse, first-world economy. In usual times, retailers would love the high AUD. Most of our consumer goods are imported so the decrease in wholesale costs would mean a fat increase in profits for the likes of Harvey Norman, JB Hi Fi, DJs and Myers. However, the Australian consumer has been spooked by global economic turmoil and their own high levels of debt. They’ve also discovered the delight of sticking it to our expensive bricks-and-mortar retailers by purchasing goods online. Even with lower import costs, our retailing dinosaurs are no match for the low overheads and cheap prices of nimble online sellers. So retail is suffering in what should be good times.

The commodities boom that is supporting our AUD should also mean big profits for our engineering services companies. However, the boom itself is creating issues as skilled worker shortages drive up labour costs. Intense competition for big projects can also lead to hasty, low-ball quotes as the Leightons debacle has shown. In addition, many large mining projects are finding it cheaper to pre-fabricate their equipment/structures in Chinese fab shops and ship them into Australia for final erection. This results in local heavy industry missing out on all but the last modular connection works.

But, there is one more major Australian beneficiary to the high AUD environment beyond internet shoppers – travel agents.

Go forth and holiday

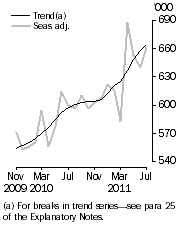

As the ABS data below shows, Australian’s are using their new-found purchasing power and heading overseas for holidays in increasing numbers.

Over the last two years, overseas short-term departures have increased about 20%. This hefty jump should mean an increase in business for our travel and accommodation booking companies that offer overseas packages. In the ASX, the first three companies that come to my mind are Webjet, Flight Centre and Wotif.

Webjet (WEB)

Webjet is “an electronic manager, marketer and credit card merchant of travel and related services utilising the internet and other mediums”. In other words, one can go to their website and look for the cheapest flights from a host of carriers as well as search for accommodation from around the world. They also offer car hire and travel insurance and have websites in Singapore, Hong Kong, USA, NZ and UK.

Webjet has taken advantage of the increase in overseas travel, posting a 5% increase in NPAT for FY11. This has come from an 18% revenue increase and a 17% increase in transactions volumes. Return on equity over the last 5 years has been pretty good, increasing from 20% to 27%. Webjet is debt free, has relatively low intangible assets for an online business and a grossed-up dividend yield of about 7% – not bad in these volatile times.

From a value-investing perspective, Webjet has good-looking numbers and seems to be taking advantage of the shift to online trading in holiday organisation. Keep an eye out for an upcoming Equities Spotlight article on WEB in the next week or so.

Flight Centre (FLT)

Flight Centre is a well-know Australian travel agency and also incorporates Escape Travel, Student Flights, quickbeds.com and several other travel brands. It has been around for some time, starting out as the traditional shop-front based travel agent. It still has over 2000 shops, operates in 11 countries and employs 8000 staff and consultants. However, they have moved with the times and now offer similar services on their website to Webjet.

Revenue increased 4% last year and transactions volumes went up 12%, however NPAT was flat. There was a goodwill write down in their US business. The fact that 49% of their shops are located outside Australia would also act as headwind due to the high AUD. Intangibles of $3.46 vs normalised earnings of $1.42 are relatively higher than Webjets, the result of previous acquisitions. The balance sheet is net-debt free, whilst ROEs have hovered between 15% and 20% for the last 5 years.

Personally I prefer Webjet to FLT because most WEB’s revenues are mostly Australian-sourced and they aren’t saddled with shop fronts which, in my opinion, will become obsolete in the future.

Wotif (WTF)

Most of us know of Wotif – the go-to website for cheap accommodation, often at the last minute (although WTF recently extended booking horizons to 6 months). They are a classic Australian online business success story; the name now synonymous with cheap online booking in Australia. I see they now offer flight bookings through their website – a natural and necessary compliment to their business given WEB and FLT both offer flights and accommodation services.

FY11 revenue increased 2% whilst NPAT fell 3.8%. Management noted:

…an unprecedented appetite for offshore travel by the Group’s core Australian and New Zealand customer base hampered growth until the last quarter of the financial year.

This indicates Wotif is not in the position I had assumed to take advantage of the higher AUD. However, management is confident that cautious consumers will provide a benefit to WTF as they turn to their services in order to save on holiday costs. At least confident enough to predict a profit boost in FY12.

Wotif’s ROE has been decreasing over the last few years, although it has moved from an awesome +100% to a still-very-impressive 56% in FY11. They carry a miniscule amount of debt – easily covered by cash and equivalents – whilst intangible assets are also low. Another good-looking business from a fundamentals perspective, but facing the macro challenges of a high AUD.

The Silver Linings

So WEB and FLT should do well as long as the dollar remains high. However, Wotif’s domestically-focussed revenue sources have seen it miss out on the Aussie exodus. At Empire we believe Webjet to be the best investment due to its low intangibles, high ROE and online business model. We also like Wotif, but from the perspective of the high AUD it would seem Webjet has the greatest capacity for earnings growth.

What does the MB community think – are there any other companies out there (travel related or not) that should also benefit from the high AUD?

We could do with a little earnings optimism, after all.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.