Cochlear (COH, previously covered at MB here) announced a voluntary recall of its Nucleus 5 implant products yesterday. The share price was promptly massacred, closing down 20% to $57.50. The main jist of the recall was as follows:

COH is undertaking a voluntary recall of the unimplanted Nucleus CI500 cochlear implant range and is currently notifying healthcare professionals and regulatory authorities.

While less than 1% of CI512 implants have failed since launch in 2009, Cochlear has identified a recent increase in the number of nucleus CI512 implant failures. In an abundance of caution Cochlear has issued a voluntary recall of the Nucleus CI500 range of cochlear impants wile it further investigates the cause of this issue

And continuing:

All existing recipients with a Nucleus CI500 series implant can continue to use their system as normal.

The two main points to note are:

- The recall is only for un-implanted implants made since 2009 – in other words, there is no need to remove those products already implanted. A good thing for current recipients.

- The expected failure rate of the implants being recalled is less than 1%

So it’s not a horror recall where every unit needs to be taken out of peoples skulls and replaced. In addition, the failure rate appears to be low at less than 1% (but obviously not good enough by medical standards). The information released thus far doesn’t indicate a catastrophic problem, so the large share price drop may provide brave investors with a rare contrarian opportunity to by a wonderful company at a great price.

Let’s look closer:

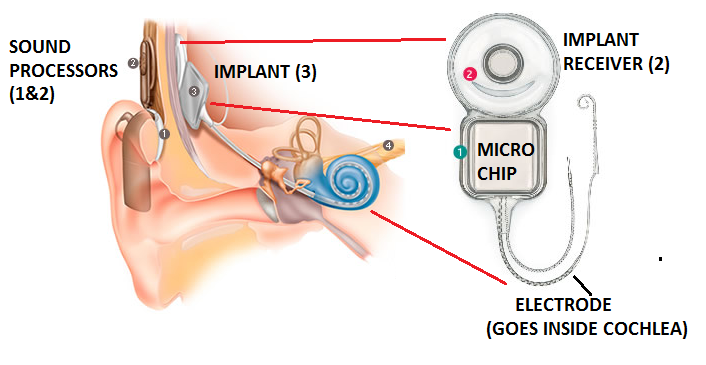

What’s in an implant?

The Nucleus device is made up of two main sections – an external sound processor and coil and an internal implant.

The sound processor captures sound and converts it into digital code whilst the sound processor transmits the digitally-coded sound through the coil to the implant. The implant converts the digitally-coded sound to electrical impulses and sends them along the electrode array, which is positioned in the cochlea.

It is the implant which has been recalled no further details have been given on whether the problem is hardware or software.

How big a deal is it?

Unfortunately, the nucleus device is COH’s number one product – it made up $648m of the $809m in revenue for FY11. Of that $648m in implant sales, 70% came from the implant type affected by the recall.

I did some back-hand calcs and estimated the number of un-implanted units to be recalled is in the order of 1300, based on the finished goods numbers in the FY11 results. By comparison, COH implanted about 17,250 of the affected units in FY11. Assuming the failure rate of the units is 1% (higher than stated in the press release), then about 170 units from last year’s implants will need replacement. If we multiply this by 3 years (2009 through to 2011) then we get a (very conservative) estimate of 500 units that will need replacement.

In dollar terms, I don’t think it’ll make a big dent in the $180m or so COH makes in net profit each year. However, this could change should the problems be larger/more widespread than stated in yesterday’s release. It also doesn’t take into account the intangible losses associated with the bad press COH is getting.

Is the current share price justified?

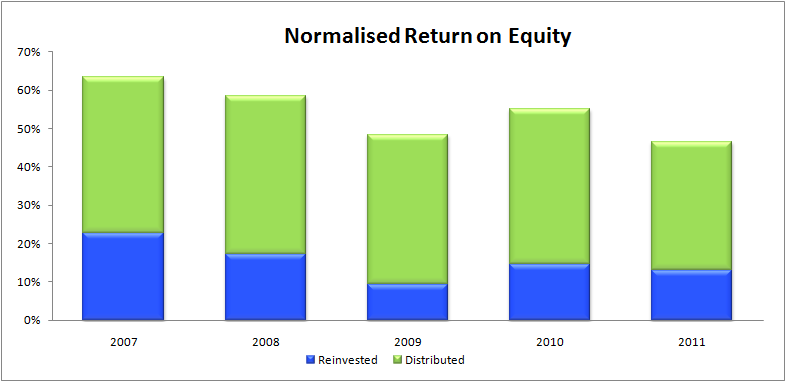

In my opinion, the market has oversold COH based on the information publically available. The recall is bad news – no doubt – but the scale of the problem doesn’t seem to warrant a 20% price drop. When I run our valuation calculations, the current price of about $57.50 is only justified if normalised ROE was to run at 30 – 35% for the next 5 years. By comparison, COH had an averaged normalised ROE over the last 5 years of about 64%.

So, NPAT would have to drop 40-50% to justify the current prices. I just don’t see that happening with the current recall information at hand. NPAT may be hit this year and next, but in the long term COH should remain the dominant supplier of implants to the planet. They currently have 70% of the market, their books look great, they spend a bucket-load on R&D and their name has become synonymous with ear implants (sort of like the Coca Cola for hearing assistance). In addition, their main competitor has also had recall/product quality issues in the past.

Of course I could be wrong and things could get much worse, in which case NPAT may drop drastically and COH would stop being the wonderful company we think it is. But no investment is without risk, even for the value investing puritans.

But if you ask me, buying a wonderful company with a dominant market position after a sudden 20% price drop goes some way to mitigating investment risk.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has an interest in the businesses mentioned in this article. The author also has a personal interest in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.