Advertisement

The Reserve Bank of Australia (RBA) has released the Financial Aggregates data for August 2011.

Here’s the summary (emphasis added):

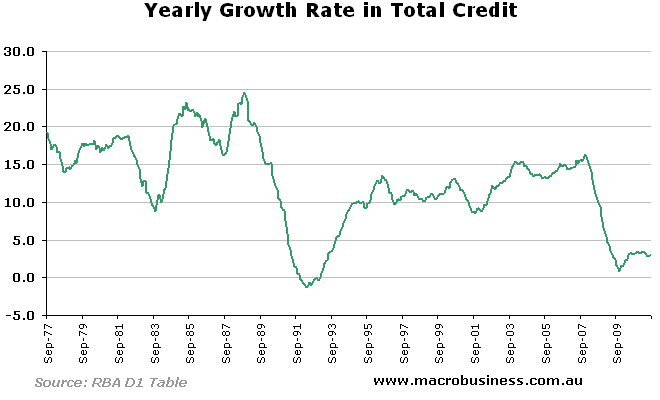

- Total credit provided to the private sector by financial intermediaries rose by 0.2 per cent over August 2011, after rising by 0.3 per cent over July. Over the year to August, total credit rose by 3.0 per cent.

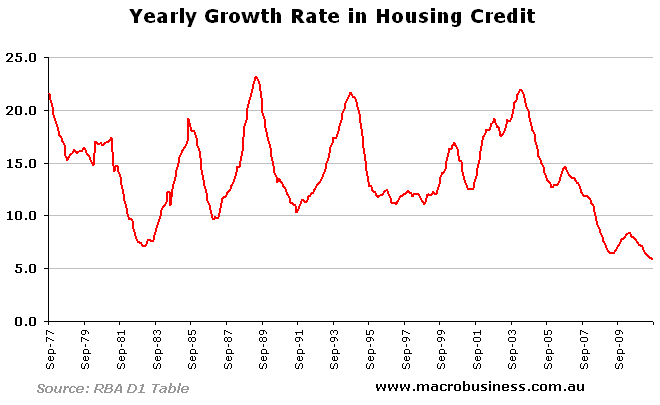

- Housing credit increased by 0.4 per cent over August, following an increase of 0.5 per cent over July. Over the year to August, housing credit rose by 5.8 per cent.

- Other personal credit declined by 0.9 per cent over August, after decreasing by 0.4 per cent over July. Over the year to August, other personal credit decreased by 0.9 per cent.

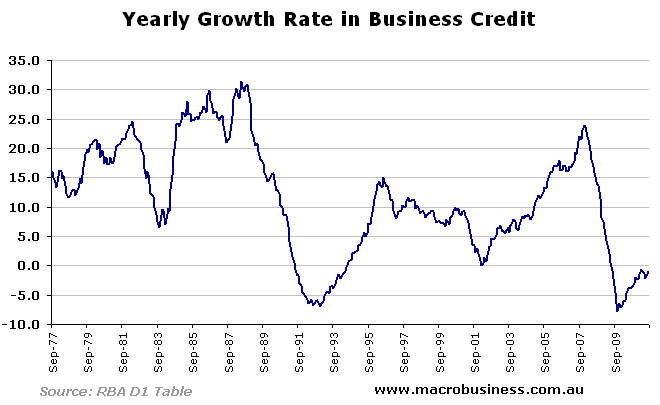

- Business credit was flat over August, following a similar result in July. Over the year to August, business credit declined by 0.9 per cent.

- Over the month of August, M3 grew by 1.3 per cent and broad money grew by 1.3 per cent. Over the year to August, broad money grew by 7.8 per cent.

Looking at the data visually, first by housing credit yearly growth:

Then business:

Advertisement

And total growth:

UPDATE:

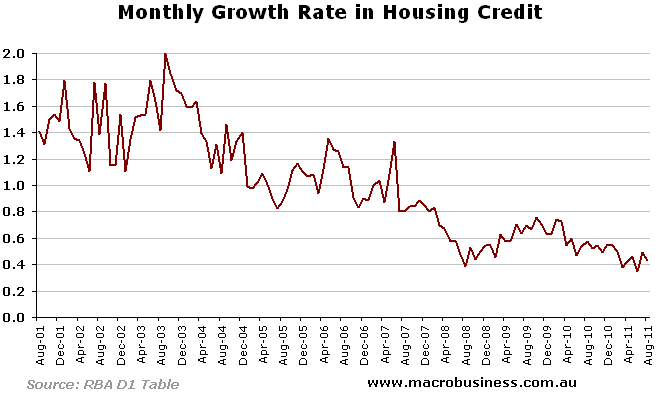

Some readers have asked for a closer look at the change in monthly housing credit growth – here is a chart going back 10 years:

www.twitter.com/ThePrinceMB

Advertisement