The S&P/ASX 200 closed higher today, up 45.2 points or 1.07% at 4212 points, recovering most of this week’s losses.

Asian markets experienced similar gains, with the Nikkei 225 closing 1.5% higher at 8772 points, and the Hang Seng up 1.33% at 19724 points.

In other risk assets, the AUD remained steady against the USD at $1.0460, whilst WTI crude picked up only 0.4% at $85.50 USD per barrel. Gold continued to fall throughout the Asian session to an intra-day low of $1728, but it is now back at $1742 USD an ounce.

Movers and Shakers

It’s mainly a green board on the ASX today, with all but the consumer staple sector up, with energy stocks the standout. but Volatility abounds due to earnings reports, here’s just a sample: Woolworths (WOW) is off 5.5% even though profit was up a similar number for the year and Transfield (TSE) down a whopping 22%.

All the banks closed the day up, with ANZ up 1%, CBA up 1.7%, whilst WBC climbed 1.4% and NAB the standout up 2.3%

BHP Billiton (BHP) closed the day up 1%, even after announcing a record corporate profit yesterday, whilst RIO climbed similarly.

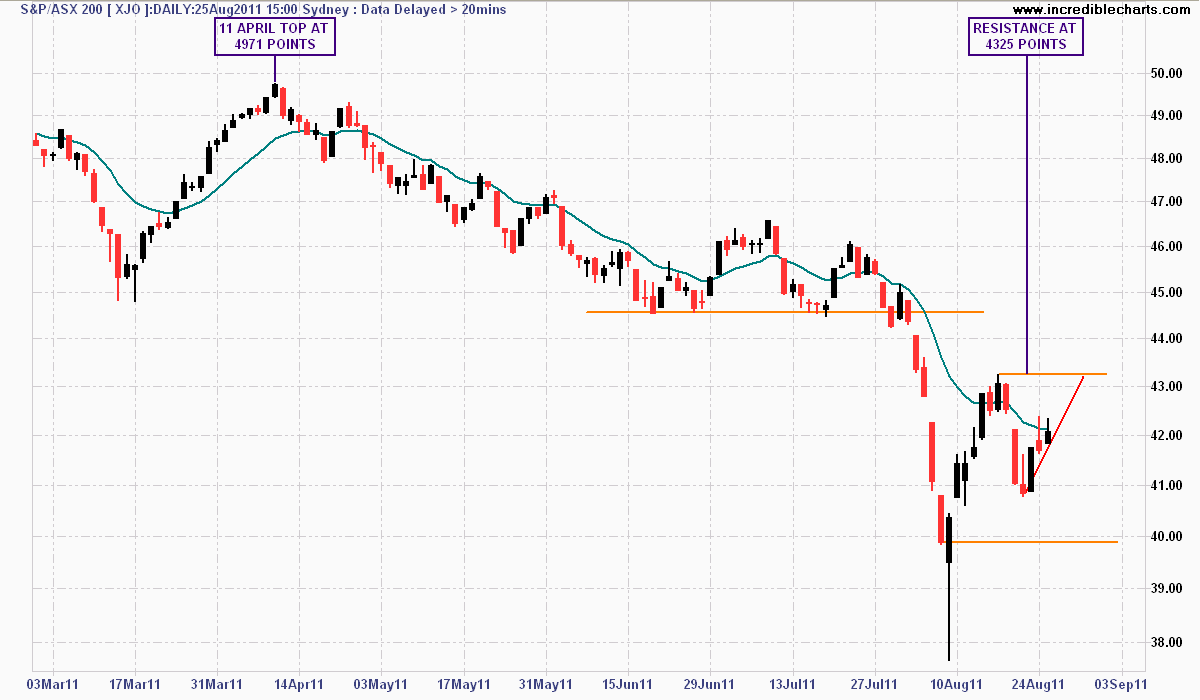

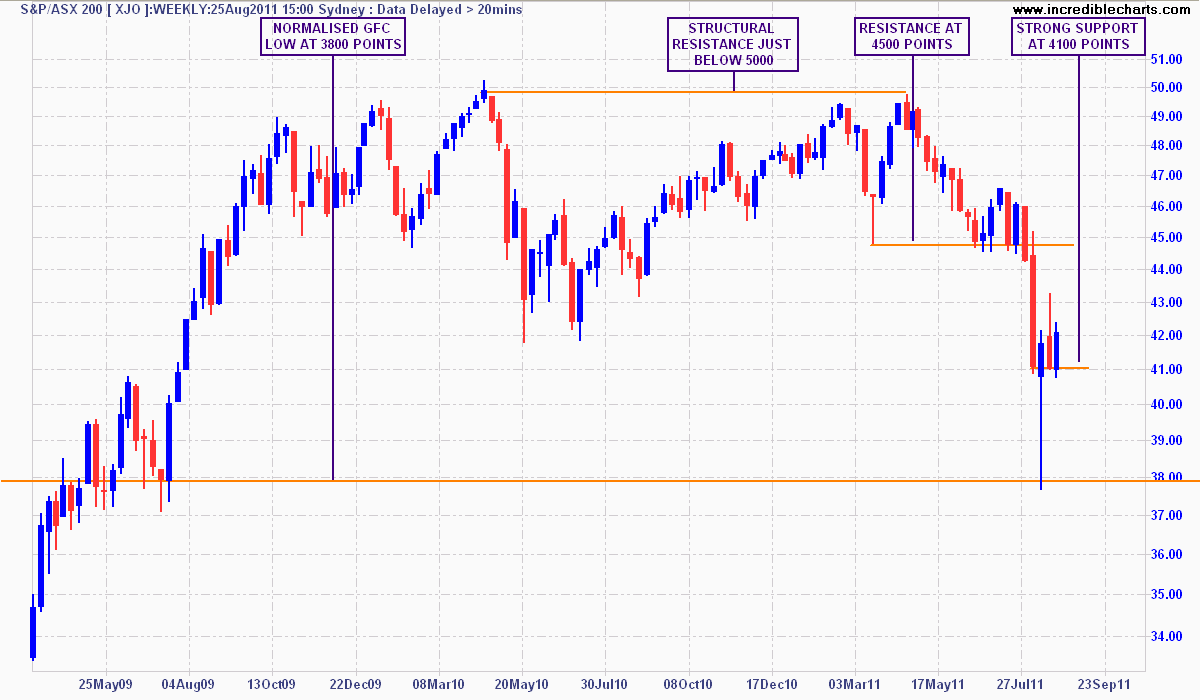

The Charts

In the short term, there is strong resistance at 4325 points – the high reached during the rebound rally from the epic correction of early August. Failure to breach this level will likely send the market back down to 4100 points, or even to the closing low of 4000 points.

Daily chart of ASX200 - click to enlarge

The medium term is more pronounced with support and resistance levels very clear: medium term structural resistance at 4500 points (the target for any sustained rebound rally), with strong support at 4100 points (tested three weeks in a row) and secular, long term resistance at 5000 points (the target to exceed to reverse this secular bear market).

Weekly chart of ASX200 - click to enlarge

We all wait for The Bernank to make his “queasy” speech at Jackson Hole tomorrow night, AEST time.