In the lead up to Standard and Poors’ (S&P) downgrade of US Government debt, the largest holder of US Treasuries – China – had stepped-up its warnings and condemnation of the US Government’s fiscal mis-management and its deteriorating debt repayment capability.

In November 2010, China’s Dagong Global Credit Rating Co. reduced its credit rating for the US to A+ from AA, citing a deteriorating intent and ability to repay debt obligations after the Federal Reserve announced more monetary easing (‘Quantitative Easing’). At this point in time, Dagong’s US credit rating was four notches below the global credit ratings agencies: S&P, Moodys and Fitch.

And in the month prior to the S&P downgrade, senior Chinese officials expressed strong disdain at the US’ economic mis-management to Stephen Roach, Morgan Stanley’s Executive Chairman of Asia:

The Chinese have long admired America’s economic dynamism. But they have lost confidence in America’s government and its dysfunctional economic stewardship. That message came through loud and clear in my recent travels to Beijing, Shanghai, Chongqing, and Hong Kong.

Coming so shortly on the heels of the subprime crisis, the debate over the debt ceiling and the budget deficit is the last straw. Senior Chinese officials are appalled at how the United States allows politics to trump financial stability. One high-ranking policymaker noted in mid-July, “This is truly shocking… We understand politics, but your government’s continued recklessness is astonishing.”

Then, in the days prior to the S&P downgrade, Dagong again reduced its US sovereign debt rating to A from A+, placing the US five notches below AAA and on par with Russian sovereign debt.

And following the S&P downgrade, the Chinese Government blasted the US Government’s debt addiction, demanding that the US live within its means and cut its military and social security spending in order to ensure the safety of China’s US dollar assets, as well as advocating the creation of a new reserve currency:

China, the largest foreign holder of U.S. debt, demanded Saturday that the United States tighten its belt and confront its “addiction to debts” in the wake of Standard & Poor’s decision to downgrade the U.S. credit rating.

China currently owns $1.2 trillion of U.S. Treasury debt, the largest stake of any central bank. The commentary carried by the state-run Xinhua News Agency was China’s first official response to the S&P decision.

“The U.S. government has to come to terms with the painful fact that the good old days when it could just borrow its way out of messes of its own making are finally gone,” Xinhua said.

It said the rating cut would be followed by more “devastating credit rating cuts” and global financial turbulence if the U.S. fails to learn to “live within its means.”

“China, the largest creditor of the world’s sole superpower, has every right now to demand the United States to address its structural debt problems and ensure the safety of China’s dollar assets,” it said.

Xinhua said the U.S. must slash its “gigantic military expenditure and bloated social welfare costs” and accept international supervision over U.S. dollar issues.

Last month, China’s top general, Chen Bingde, also linked America’s financial woes to its military budget and asked whether paring back on defense spending wouldn’t be the best thing for U.S. taxpayers.

Such comments reflect China’s desire that the United States reduce its military presence in Asia. The U.S., rattled by China’s military buildup, also routinely chides China for its fast-growing defense spending.

Xinhua also suggested a new global reserve currency might be necessary to replace the dollar, a position China has frequently advocated.

“Mounting debts and ridiculous political wrestling in Washington have damaged America’s image abroad,” Xinhua said. “To cure its addiction to debts, the United States has to re-establish the common sense principle that one should live within its means.”

China’s concern about the US Government’s ability to repay its creditors is understandable, given it holds around $1.2 trillion of US Treasuries, equating to nearly 30% of total outstanding US Treasuries as at end-2009 (see below US Treasury chart):

The acceleration of China’s US Treasury holdings – from 5% in 1994 to around 28% as at end-2009 – coincided with the 50% devaluation of the Yuan against the USD in early 1994 (denoted by the black vertical line).

This devaluation of the yuan represented a deliberate policy action undertaken by the Chinese authorities in the wake of the mid-1990s Asian Financial Crisis in order to both promote export-led growth and insulate China’s financial system from future external shocks by accumulating large foreign-exchange reserves. The Chinese Government achieved this devaluation by ‘sterilising’ its trade surpluses via selling the Chinese yuan and buying USD denominated assets, including Treasury Bonds.

For over a decade China’s policies achieved their goal, with China’s holdings of US Treasuries offsetting declining holdings by US households, thereby enabling higher levels of US consumption – much of which was spent on imports from China (see below US Treasury chart):

But in being so reliant on financing from China to help promote growth and fund its budget deficits, the US has handed China considerable political leverage.

With the US Government now monetising its debts (via ‘Quantitative Easing’), there is the risk that China might decide to offload a large share of its Treasury holdings, which could, other things equal, eventually lead to a sharp depreciation of the USD and force the US to raise interest rates in order to attract capital from other investors.

However, the likelihood of this scenario playing out is slim since a large sell-off by China could:

- decrease the value of China’s remaining dollar-denominated assets, leading to large investment losses;

- diminish US demand for Chinese imports, either through a rise in the value of the yuan against the USD or a reduction in US economic growth via higher interest rates; or

- provoke protectionist measures in the US against China.

At the end of the day, China and the US are caught in a morbid dependency whereby China sells its goods to the US and the US borrows money from the Chinese to pay for these goods. Like it or not, both nations are inextricably linked, despite the often-heard claim that China has de-coupled.

Which brings me to a related dilemma arising from the current market ructions: assuming the US and European economies experience another protracted slowdown, can China maintain its current growth trajectory?

To help answer this question, lets first examine the statistics.

First, China’s exports by destination:

As you can see, the US and EU account for around 35% of China’s exports.

Second, the composition of China’s GDP:

This chart illustrates two important points. First, in 2009, the last time Western nations were in recession, declining exports lopped almost 3% from China’s GDP. There is no “decoupling”.

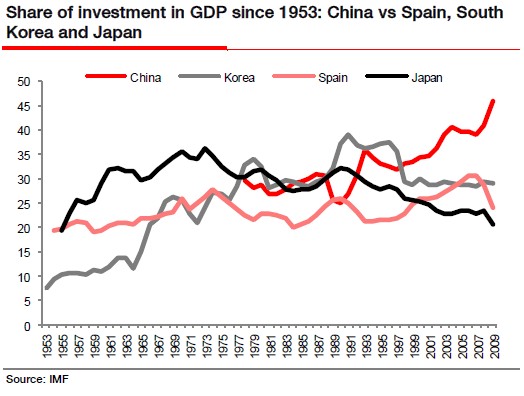

Second, China’s GDP growth has become increasingly dependent upon fixed asset investment, which peaked at a whopping 90% of GDP in 2009, and has surpassed the peak levels reached by both Korea and Japan during their industrialisation.

{kind=link}

This increase in fixed asset investment arose after the Chinese government embarked on a massive fiscal and monetary stimulus program in the latter half of 2008 to counter the aftershocks of the global financial crisis.

The maintenance of artificially low interest rates at China’s state-owned banks – which punishes the country’s savers (households) and encourages over-investment (speculation) in housing, as well as over-investment by state-owned enterprises that are able to borrow at subsidised rates from China’s banks – has also contributed to the fixed asset boom.

As has been well documented on this blog (most recently here), much of this investment appears to have been channelled into unproductive ventures, which raises the prospect of China’s banking system (read depositors) being saddled with a significant amount of non-performing loans.

Another worrying trend for China, as evident in the above chart, is private consumption’s declining share of GDP growth, as well as both labour income and personal disposable income falling as a share of national income and GDP (see below charts):

In the event that the US and European economies do enter a protracted downturn that crimps imports from China, the Chinese authorities will have to engineer one (or a mix) of the following outcomes in order to maintain current rates of GDP growth:

- maintain high levels of fixed asset investment;

- shift GDP growth towards domestic consumption; or

- increase exports to other nations.

Maintaining China’s recent rate of fixed asset investment appears unsustainable. There is only so much infrastructure, buildings and factories that can be built before overcapacity is reached (if it is not already).

Shifting GDP growth away from fixed asset investment and exports towards domestic consumption is the authorities’ end goal. However, as shown by the above charts, the trend is currently moving in the wrong direction with consumption’s share of GDP falling, suggesting that this outcome is not achievable any time soon.

Finally, increasing exports to other nations (e.g. Asia) to offset declining exports to the US and EU would likely be difficult, as protracted slowdowns in the US and EU would likely adversely affect growth in China’s other trading partners, affecting their demand for Chinese goods.

Ultimately, any hard landing in the US and EU is likely to adversely affect China’s growth prospects one way or another, although the extent and timing is uncertain.

With these thoughts in mind, I will leave you with some sage advice from Michael Pettis, who believes that China can avoid a hard landing, but not an ultimate day of reckoning (via Interest.co.nz):

I would argue that we urgently need to see a shift in the economy away from infrastructure, SOEs and real estate towards service industries and SMEs, especially those that are labor intensive. Until we do it is pretty meaningless to talk about a real adjustment in the engines of economic growth.

China has no choice but to adjust, but as long as it is easy to borrow – and I think we have at least four or five more years during which time debt levels can continue rising before we hit crisis levels – the adjustment problem can always be put off a little longer. That is why we are unlikely to get a real sharp slowdown in growth for at least another year or two.

But what to do about rising debt levels? This is the real problem China is facing now, and my biggest concern is that policymakers are buying into the argument that China can “grow out” of the current debt burden, just as it did after the banking crisis of a decade ago. In other words, if we keep investment levels high, we can keep growth high, in which case we can safely ignore the huge pile of debt, just as we were able to ignore the huge pile of NPLs that the banks had accumulated in the 1990s.

Contrary to popular opinion, China did not grow its way out of the previous debt crisis. What happened was very different. By keeping interests rate incredibly low, China was able to do two things.

First, very low interest rates presented a huge subsidy for borrowers, so it allowed them to borrow and invest in every conceivable project, whether of not it made economic sense. Of course all this investment created growth in the present, but because investment was misallocated, it simply meant that in future years growth would be much lower. To that extent, we didn’t have real growth – we simply overstated current growth rates in exchange for being forced to write the growth off in the future. Over the next few years we are going to pay for that misallocated investment in the form of slower growth. That means that much of the growth that allowed us to “grow” out of the debt problem simply involved pushing the real cost of the debt crisis forward.

Second, very low interest rates effectively created substantial debt forgiveness for the borrowers, so again even with the artificially high growth, China did not “grow out” of its debt. It just wrote most of the debt off, at the expense of course of depositors. This is why consumption collapsed during this period as a share of GDP.

For this reason the idea that we can “grow” out of the debt problem once again by keeping investment high is wrong. First, it would only increase capital misallocation and debt levels, and would require even lower growth in the future. We can’t keep pushing the cost off into the future, as attractive an option as that always seems. Second it would put unbearable pressure on household income and consumption, and so ensure that the one thing China needs above all – a rapid rise in household consumption – is all but impossible.