The S&P/ASX 200 was slated to make further gains today, but has moved down almost 24 points or just over half of one percent just after midday, now at 4584 points. This is possibly due to the weak Chinese PMI figures (forecast at an expanding 52, came in at 50.2) and the equally important Japanese large manufacturer confidence number has plunged to -9. This has resulted in a mild sell off of the AUD/JPY – a closely watched correlation for the ASX200.

Other Asian markets are still up on these results, with the Nikkei 225 up 0.5% at 9862 points, and the Hang Seng up 1.54% to 22,398 points.

Other risk assets are down or steady, the AUD just above 1.07, whilst gold is back down to support at $1501 USD an ounce. WTI crude is steady at $94.71 USD per barrel.

Movers and Shakers

It’s mainly red across the board with only a few stocks advancing. The four major banks are giving back most of their gains in the previous day(s), with ANZ down 0.58%, CBA down 0.9%, NAB down 1.05% and WBC down 1.12%.

BHP is steady at $43.80, whilst RIO is down slightly to $82.77

In other ASX200 stocks, Paperlinx (PPX) is up 9% followed by Transpacific (TPI) up nearly 4%. CSL is down over 1.5% to $32.54

The losers include Lynas (LYC) down 9%, Sundance (SDL) down 4.4% and JB Hi-Fi (JBH – the markets most shorted stock) down 3.2%

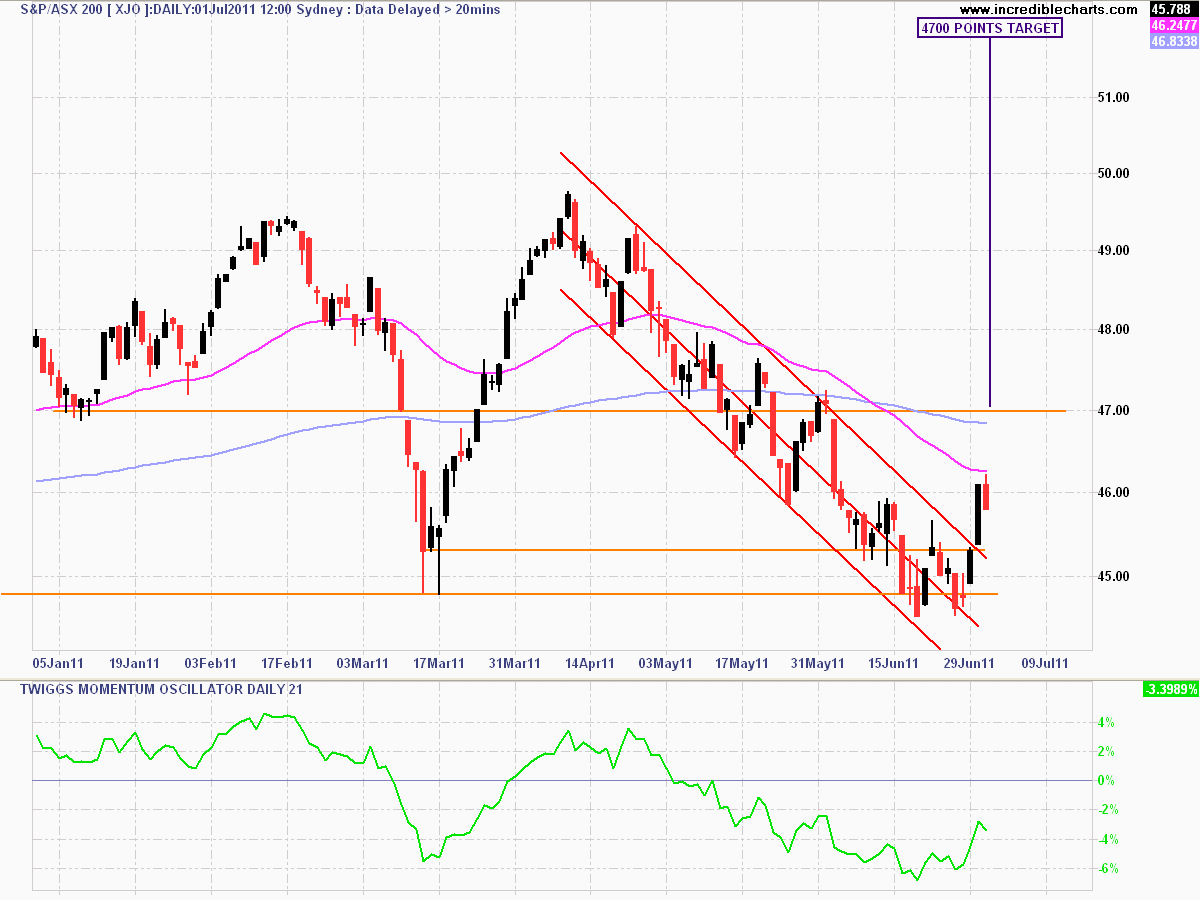

Daily Chart

The daily chart shows current prices have broken out from the downtrend channel but there is still significant downward pressure on the index as the next critical level is 4700 points. As I’ve been saying the 4500 points level has switched to support on the back of (another) Greek bailout. Technical indicators only suggest a small rally at this stage, with no confirmation of momentum or directional range.

Daily chart of ASX200 - click to enlarge