Following on from today’s post, Avoid Melbourne housing, SQM Research has just released its latest weekly newsletter again showing Melbourne as the epicentre of the nation’s housing supply glut. According to SQM, Melbourne’s stock on market has increased a whopping 47% since June 2010 (see below table).

The only ‘good’ news coming out of the newsletter is that the number of homes for sale nationally has fallen by 2% since May 2011, mostly reflecting seasonal factors (winter is traditionally a slow period for property listings).

Below are the key extracts from SQM Research’s release:

Advertisement

Stock on Market June 2011

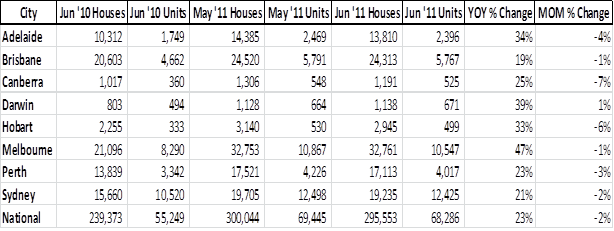

Figures released last week by SQM Research revealed that residential listings for the month of June 2011 fell by 5,650 to 363,839 nationally. This is a 2% decrease from May 2011, yet still a 23% increase when compared to the same month last year (June 2010).

Each capital city experienced a month-on-month decline excepting Darwin whose stock rose by 1% from May 2011.

The capital city to record the largest month-on-month decline was Hobart, falling by 6% since May 2011 to a total of 1,809.

The capital city to record the largest year-on-year increase was Melbourne, rising by 47% since June 2010 to 43,308.

No capital cities have recorded any declines in stock year-on-year, though Brisbane recorded the most modest growth, rising by 19% to 30,080 since June 2010.

This is the second consecutive monthly decline in listings and although to a certain extent this result can be attributed to seasonal factors as we enter into the quietest time of the year for new listings, it is possible that stock levels have now peaked for the cycle.

Managing Director of SQM Research, Louis Christopher says “Real estate listings remain at levels high enough to record overall house price falls, however we note that the level of listings may have also finally peaked.

“It’s too early yet to call a bottom in the current housing downturn and even when it eventually does come, a recovery is very likely to be slow. But clearly we are much closer to a bottom in the market than where we were 12 months ago.

“Much is dependent upon the direction of interest rates and any type of meaningful government intervention in the market place.”

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.