The S&P/ASX 200 opened higher, shrugging off bad job data, and at midday is up 10 points or 0.2% to 4546 points. The correction has now wiped off just over 9% of price in the ASX200, just below the conventional 10% level of a complete correction.

Asian markets are mixed, with the Nikkei down over 0.29%, the Hang Seng dropping 0.31% but Singapore up slightly.

Other risk assets are mixed, with the AUD dropping sharply below 1.06 on the ABS Jobs figures, now 1.058 against the USD, gold slipping to $1537 USD an ounce. WTI crude has jumped above $100, at $101.25 USD per barrel.

Movers and Shakers

Its mainly green across the board, with both bankers (houses) and miners (holes) up. CBA is up 0.43% and NAB 0.21%, with ANZ up strongly 0.8% and WBC 0.56%. The major resource stocks BHP and RIO are up 0.26% and 0.33% respectively.

In other ASX200 stocks, healthcare leader CSL is down 1.84%, whilst Sigma Pharmaeutical (SIP)builds on yesterday’s gains, up 8.3% with Linc Energy up 6.3%. The uranium miners continue to fall with Paladin down 4%, ERA down 2%

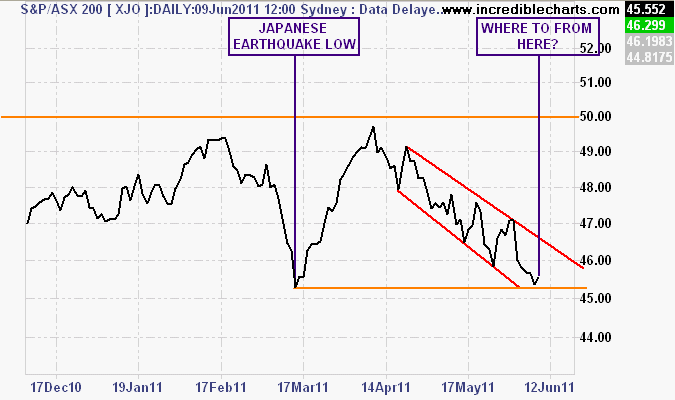

ASX200 remains below critical support level

The market remains in a downward, albeit decelerating trend pattern and remains at the Japanese earthquake lows just above 4500 points.

The daily chart shows the market on the Japan earthquake low, but not lower. A break below this level would extend the correction, with the next target at 4200 points – the lows in the May flash crash of 2010.

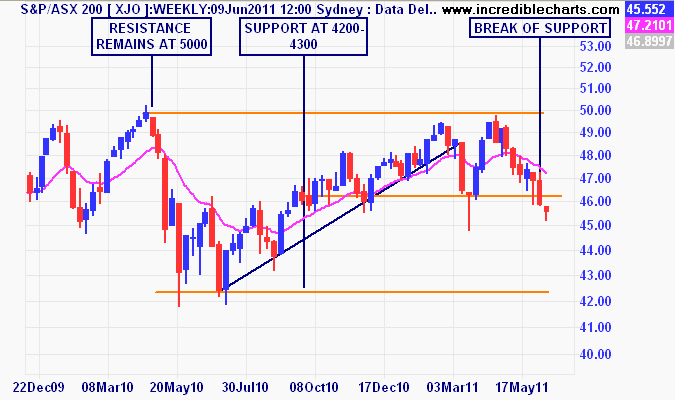

The weekly chart still shows the key difference between the Japan earthquake/MENA riots low of March and now: the market closed the week above the 4600 support level (overshoot of this on a daily level is normal, its the weekly close that matters) in the former, whilst it is on track to close 2 successive weeks below currently.

Daily chart of ASX200

Weekly chart of ASX200 - note difference in candle from Japan lows