The S&P/ASX 200 has steadied after midday, now at 4498 points, down 0.04%, after opening slightly higher.

Asian markets are mainly up, with the Nikkei up 0.28 percent to 9624 points, and the Hang Seng up strongly, 1.22% to 22,025 points.

Other risk assets are mixed, although the AUD is just below 1.055 against the USD, gold slightly up from its overnight plummet at $1522 USD whilst WTI crude is down again at $91.89 USD per barrel.

Movers and Shakers

It’s mixed across the board with resources stocks mainly up. ANZ is the only bank loser, down 0.14% whilst NAB is the best up 0.9%. WBC and CBA are up 0.5% and 0.8% respectively.

BHP is up another 0.5% to $42.25, whilst RIO is up 0.3% after rising to $80.48 per share, now back at $80.26.

In other ASX200 stocks, Cochlear (COH) has rebounded 1.5%, whilst its “brother” CSL has fallen 2.75% on the continued bad news from the US FDA. Telstra (TLS) is also swallowing the NBN news and is down a significant 2.4%

Gunns (GNS) continues to be volatile, up over 15%, whilst Macmahon Holdings (MAH) is up over 2%. APA Group (APA) is down nearly 10% after its $300 million capital raising whilst Duet Group (DUE) is off 6% and Nexus (NXS) reversing yesterdays gains, down over 6%

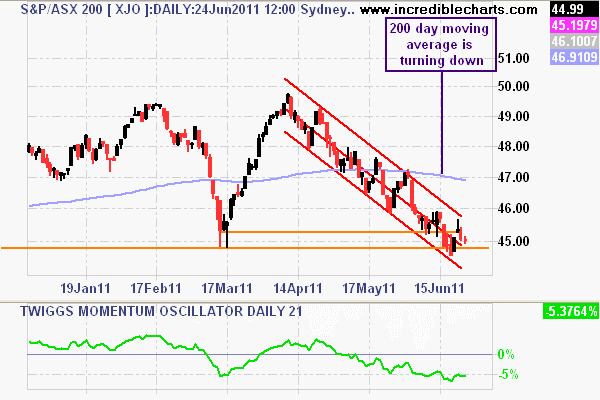

Daily Chart

The daily chart shows how the current price activity still hovering around the low point of the Japanese/MENA lows of March. It seems 4500 points is now resistance (i.e the price above the market is not willing to pay) switching from support.

Note how prices are failing to bust the upper channel line at approx. 4560 points. A close above this resistance line and heading above 4600 points would suggest a rebound/impulse rally has some steam behind it but until then, the next target is 4200 points for the index.

Six month daily chart with 200 day moving average (grey line)