Once in a while a real estate article gets published in the mainstream media that is so bad that it just has to be dissected. Mark Armstrong, an independent [sic] property analyst, adviser and director of Armstrong Property Planning, published one such article yesterday in Fairfax, entitled Bold investors buy in a softer market.

Here are some key extracts, together with my own counter-arguments.

On top of this many property markets around the globe have suffered major corrections in value and many investors are asking themselves: ”is the Australian market going to suffer the same fate?”

…I don’t think the Australian market is going to crash…

To understand why we seem to defy global trends we need to look at the differences between markets.

The Australian and US markets differ greatly from a tax and financing point of view but when we dig a bit further we find there are also significant demographic differences.

While culturally the two countries have many similarities, their societies live quite differently. In Australia, more than 70 per cent of the population live in the 10 biggest cities. This ensures a very centralised market where the bulk of the population competes for scarce land close to major infrastructure.

This competition for a finite commodity puts pressure on the value of land and results in a more robust property market.

Because most of the population wants to live in these defined areas it creates a housing shortage…

Advertisement

Okay, let’s stop right there. According to Mr Armstrong’s own figures, some 16 million people live in the 10 largest Australian cities. And the concentration of our population in these locations has resulted in greater competition for housing, thereby pushing up its cost.

Back to the article.

By contrast, in the US only 13 per cent of Americans live in the 10 largest cites… The US has a more decentralised population and, as a result, the pressure on the value of land is less.

Again, using Mr Armstrong’s own figures derives a population of some 40 million (13% multiplied by 309 million) living in the 10 largest US cities. That’s 2 1/2 times the number of people living in Australia’s 10 largest cities.

Advertisement

Given these facts, and following Mr Armstrong’s own line of argument, you would expect house prices in the largest metro areas of the US to be significantly more expensive than Australia’s, since a much larger number of people are competing for housing. Let’s have a look.

First, consider the Median Multiples (median house prices divided by median household income) of Australia’s capital cities as calculated by Demographia:

Advertisement

Now consider the Median Multiples of the five largest US metropolitan areas. Note that the populations of each of these regions is larger than any of the metropolitan areas of Australia’s capital cities.

There are two important observations from the US chart.

Advertisement

First, that the Median Multiples are typically lower in these US cities, despite their significantly larger populations. This flies in the face of Mr Armstrong’s suggestion that Australia’s concentrated population justifies its lofty housing valuations.

Second, the massive housing crash experienced in Los Angeles (population of 12.8 million) contradicts Mr Armstrong’s claim thatthe “competition for a finite commodity puts pressure on the value of land and results in a more robust property market“. If this was the case, then why did Los Angeles house prices fall so violently? [Hint: read here for the answer].

Anyway, back to the article.

America has traditionally had very well established small town communities with schools, transport and entertainment. These small towns often do not have a shortage of land and while this does create more affordable housing it also increases the risk of price volatility.

Unfortunately Mr Armstrong has it backwards – abundant land supply, free of physical and regulatory constraints, reduces price volatility as supply is free to adjust to changes in demand.

Q0 and P0 represent the initial equilibrium situation in the housing market. Initial demand is provided by D0, whereas supply is shown as either SR (restricted) or SU (unrestricted), depending on whether land supply constraints exist.

Following an increase in demand, such as a significant relaxation of lending standards, the demand curve shifts outwards from D0 to D1. When land supply is restricted, house prices rise sharply from P0 to PR. By contrast, when supply is unrestricted, prices rise more gradually from P0 to PU.

The situation works the same way in reverse. For example, if there was a sharp fall in demand following a contraction in credit availability or a sharp rise in unemployment, causing demand to fall from D1 to D0, then prices fall much further when land supply is constrained.

The key point is that increases (declines) in demand can bring sharply rising (falling) house prices when supply is constrained. However, when land supply is not regulated, it adjusts to demand and house price volatility is reduced.

And this textbook explanation is supported empirically by the below charts.

Advertisement

First, consider the Median Multiples in US cities defined by Demographia as having prescriptive land-use regulations (i.e. restricted land supply):

As you can see, prices have been highly volatile in these markets.

Advertisement

Now consider the Median Multiples in US cities deemed by Demographia as having more liberal land-use regulations (i.e. more abundant land supply):

Prices have been far less volatile in these markets as changes in demand have led predominantly to changes in the rate of new home construction rather than prices.

The bottom line is that Mr Armstrong’s claim that house prices are more volatile when supply is abundant are false. The opposite is in fact the case.

Advertisement

Again, back to the article.

History shows that the Melbourne property market doubles in value every seven to 10 years and an investor who uses a more aggressive strategy now maybe in a position to sell their investment in the future and use the sale proceeds to wipe out the debt on their home many years earlier than the conservative investor.

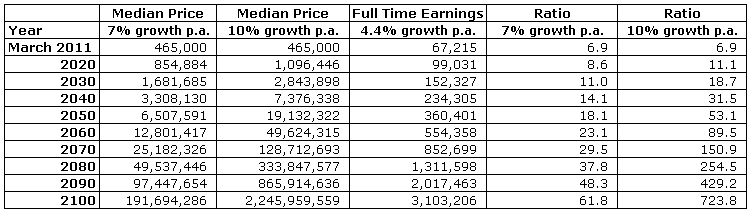

Ah yes, the tired old property doubles every seven to 10 years myth. To illustrate the absurdity of Mr Armstrong’s claim, I took Melbourne’s median dwelling price ($465,000) against Australia’s average full-time earnings ($67,215) as at March 2011. I then used the Rule of 72 to extrapolated the house prices forward by 7.2% and 10.28% per annum respectively (i.e. the growth rates required to double every seven or 10 years), and extrapolated average full-time earnings forward by 4.4% per annum, which is the average rate of growth since 1990. The results are presented in the below table.

As you can see, a growth rate of 7.2% per annum delivers a median dwelling price of around $226 million in the year 2100 against an average income of around $3.1 million, producing a dwelling price-to-income ratio of nearly 73 times!

A growth rate of 10.3% per annum delivers a median dwelling price of around $2.8 billion in the year 2100 against an average income of around $3.1 million, producing a dwelling price-to-income ratio of nearly 912 times!

Clearly Mr Armstrong does not understand the laws of compounding. In fact, the only way that his ‘doubles every seven to 10 years’ claim could ever be met is if the Reserve Bank and Government abandoned inflation targeting and allowed both wages and house prices to grow in concert via inflation (like in the 1970s). In such an event, the dwelling price-to-income ratio would be largely unchanged, but house prices could continue growing strongly in nominal terms whilst remaining steady in real terms.

To be fair to Mr Armstrong, I agree with his claim that Australian is unlikely to experience a US-style housing crash. As stated previously, this scenario would likely require a hard landing in China and a prolonged commodities price crash – possible but not the most likely outcome.

It’s just a shame that Mr Armstrong has resorted to such flimsy arguments to make the case that the Australian housing market is exceptional and will continue rising strongly into perpetuity, albeit subject to some minor adjustments along the way.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

{kind=link}