Following on from The Prince’s article on Australian debt, this week’s equities spotlight focuses on FSA Group Ltd – one of Empire’s favourite debt companies and a current constituent of our portfolio.

The Business

The Services division aims to assist debt-laden clients through facilitating payment arrangements with their creditors. This can be done through informal agreements, debt agreements, insolvency agreements and bankruptcy assistance (as well as other methods). As of December 2010 FSA held 51% of the Australian debt agreement market, which has decreased slightly slipped from the 56% share held a few years ago.

The Products division has three subsections – Home Loan Broking, Home Loan Lending and Business Factoring Finance. The broking section assists clients that already own property to consolidate their debt using the equity within their homes. The lending section (which began operations in 2007) provides both prime and non-conforming home loans, whilst the factoring finance section provides credit solutions for businesses. As of December 2010, the FSA home loan pool stood at $200M, with an average loan to value ratio (LVR) of 68%.

Recent discussions with FSA management have highlighted an interesting aspect of their business model – debt arrangement revenues increase when either the economy is surging or when the economy is in trouble. The reason for higher revenue during boom times is that consumers will over-spend and get themselves into too much debt even whilst times are good. On the flip side, during economic downturns unemployment will push people into debt problems as they cannot service their pre-bust borrowings. FSA claim the current economic environment – mid-level interest rates, low credit growth and relatively low unemployment – is actually dampening their revenue potential as people slowly pay down their debts and refrain from taking out new home loans.

Financials

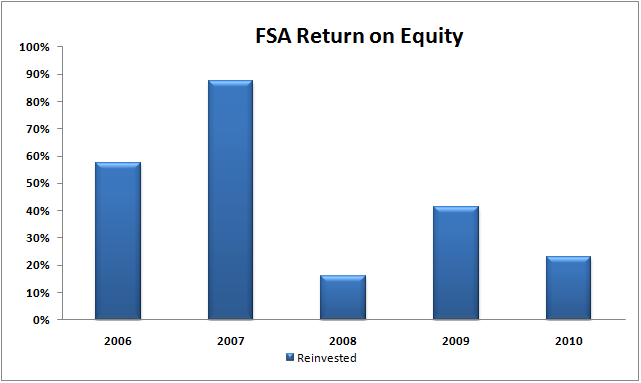

FSA’s return on equity (ROE) has averaged an impressive 45% over the last 5 years; however the annual results have been volatile. In 2008 ROE dropped to 15%, and then increased to 40% in FY09 before dropping again to 21% in FY10. Some of the volatility has been caused by starting up the home lending division (FY09), legislative changes to the fee structures of debt agreements and substantial interest rate volatility during the GFC. In addition, changes to funding arrangements after the GFC have tied up a fair chunk of FSA’s capitals, which is used as collateral against new debt warehousing facilities.

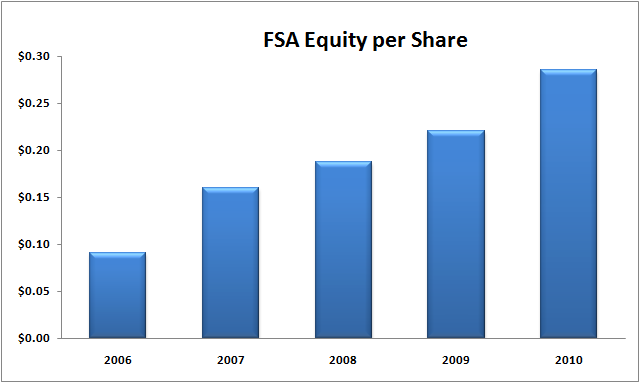

Borrowings have increased from a low base of $0.01 per share in 2007 to $0.10 per share in FY10. Net debt sits at $10M, which is small compared to the forecast NPAT of $8.5M for FY11. Equity per share has increased consistently over the last 5 years, from $0.09 in FY06 to $0.28 in FY10. Intangible assets are negligible at $0.02 per share whilst forecast FY11 earnings are $0.06 per share.

{kind=link}

In the last few years FSA’s asset sheet has grown substantially due to the expansion of their home loan services. FSA has identified a gap in the market after the exit of many non-conforming lenders during the GFC. FSA claim their home loan books are very healthy, with 99% of loans granted to owners-occupiers and 98% of debtors full-doc and employed (as opposed to self-employed). The average loan is $200,000 and has an LVR of 68%, meaning the average property value is around $300,000.

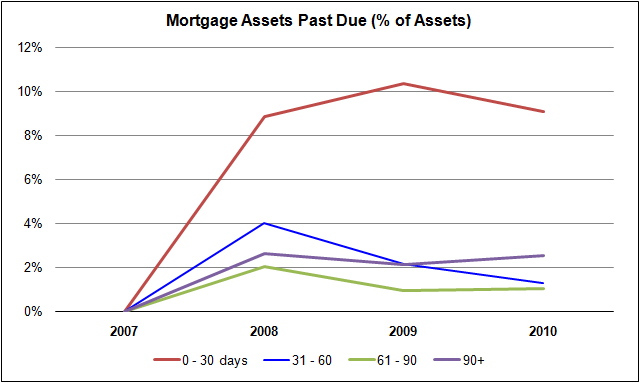

The 90+ day arrears on their home loans currently sit at 1%, which is very low for debtors in the non-confirming and low-doc market. According to the Fitch Dinkum Index Report (Q4FY10), the average 90+ arrears in this market segment is 4%. Home loan arrears for 0-30 days currently sit at 9%, which appears to be quite high and may translate into higher arrears for 30-60+ days if lenders fall further behind in their payments.

Factoring finance makes up only a small portion (~5%) of FSAs current revenue, however management claim there is large un-met demand in this market and has high growth potential in the future.

Management

FSA has a high level of internal ownership, with 40% of all shares owned by the two executive directors Tim Maher and Deborah Souton. This ensures managements interests are aligned with those of the shareholders. The high director ownership level is even more remarkable given FSA has not delivered a dividend since its inception. Typically this indicates management is confident of compounding the equity base of the business by retaining earnings for future growth – another good sign for investors. Some of the directors take upwards of 30% of their salary in short-term bonuses, however this is not typical. Bonus details are not listed in the annual reports, so the levels of bonuses will need to be watched in the future.

The management team appears to have a mix of financial, accounting and public service experience. The two executive directors have been in their roles since 2002, indicating a long-term commitment to the company.

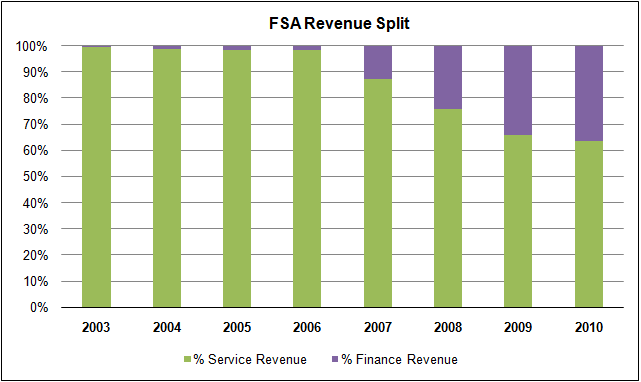

Management have been consistent (and relatively successful) with their two-pronged strategy to increase debt agreement clients and increase their home lending divisions – the increasing contribution of the lending services can be seen in the graph below. Return on equity has been volatile and the last few years profit targets have been missed, however explanations of revenue decreases have always been transparent in market updates. We believe capital allocation has been very good – resisting the urge to please the market (by distributing dividends) and choosing to reinvest profits in the company.

Key Opportunities

- FSA is a dominant player in the debt agreement market at a time when consumer debt levels are at record highs

- The increase in home lending and business finance will diversify their revenue streams

- The home loan book appears to be very healthy given their target market of non-conforming debtors

- The GFC saw the exit of many non-confirming lenders, providing FSA with an opportunity to cater for un-met demand in both individual and business lending

- Recent changes to the fee structure for debt agreements will increase the capital base required for start-up debt companies, effectively raising the barrier to entry for competitors

Key Risks

- FSA’s exposure to home lending is increasing at a time of decreasing home values (although LVRs and loan sizes are modest)

- In the past FSA has proven to be sensitive to interest rates, with low interest rate environments decreasing profit

- The 0-30 days arrears numbers for the home loans sit at a high 9% (FY10), although this may be as a result of their target market (non-conforming finance)

Summary

FSA has a very dominant position in what is potentially a high-growth market (debt arrangement services) as Australians struggle with mortgage debt and the likelihood of higher interest rates in the future. In addition, FSA has been expanding its revenue base into lending services that will further diversify revenue streams. Whilst decreasing house values may impact upon lending revenue, the current home loan book seems conservatively geared and is focussed on the lower end of the housing market. In addition, any deterioration in the economy will increase debt service revenues as consumers experience higher levels of debt stress.

The core management members have been with the company since 2002 and appear intent on growing FSA’s equity base through sensible capital management. With the debt service and loan provision segments of FSA, management are attempting to develop a robust business model that prospers in both healthy and depressed economic environments.

Due to a lack of distinct competitive advantage, we consider FSA Group Ltd a “Very Good” company.

Valuation

Empirebelieves the market is seriously mispricing FSA at the moment, with shares trading between $0.24 and $0.28 in the last few months. This is well below current equity per share of $0.32 and even less than Net Tangible Assets of $0.29 per share – a true Buffet/Graham-style value play. We believe FSA’s (eminently sensible) policy of not distributing dividends may be part of the reason for the low share price, as Australian investors have a tendency to chase dividend yield instead of capital growth.

Using a forecast ROE of 20%, equity per share of $0.32 and assuming a dividend starts being paid in 3 years time, Empire’s valuation of FSA is $0.44 per share.

Using a 20% Margin of Safety, our maximum buy price is $0.37.

Update: FSA history and Controversy

In order to ensure level coverage of FSA, I’d like to include a couple of links to some controversial aspects of FSA’s past:

http://www.accc.gov.au/content/index.phtml/itemId/740605/fromItemId/720536

http://www.heraldsun.com.au/money/dirty-debt-tricks/story-e6frfh5f-1111117793478

Obviously FSA had a run-in with the ACCC in 2006 over its conduct with debt-arrangement clients. The outcome was that Fox agreed to modify what it said and the information it gave to prospective clients. In addition the Herald article shows complaints do arise about FSA, with the article being one of several I came across during my research.

I understand that debt-related matters are controversial at the best of times, let alone when trying to run a profitable business based on peoples debt distress. With regards to the ACCC settlement, we feel that 5 years is a long enough time to demonstrate FSA has operated within the limits agreed between themselves and the ACCC. They may have overstepped the mark (according to the ACCC) in the early days, but I am yet to come across any other ACCC rulings since.

FSA’s clients are in stressful situations and most probably have limited financial skills in the first place (at the risk of generalising). So we’d expect a fair amount of complaints given their very large market share and the obvious hardships their clients face. However, if FSA truly were “sharks” that profited from unethical behaviour, I think they’d be on ACA or Today Tonight every other month given their dominant position.

The ethics of the profitting from debt are open for debate, but from a business perspective we believe FSA to be a very good company with good earnings potential (given Australia’s high level of private debt).

What do you think?

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has an interest in the business analysed in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.