It is going to be so hard for the RBA to hike rates next week given the nature and structure of economic growth that is being revealed by the economic data over the past month, since the SoMP was released. It will be interesting to see how they handle this because we are not seeing a run of the mill distinction between some areas doing well and other not so. Rather the economy now and in prospect projects a yawning gulf between the haves (mining leases) and the have nots (the rest of the economy.

Now, there is no polite way to say this but for the first real time in its modern day history the RBA risks turning the population against it. I can already see MSM headlines about “unelected” officials foisting rate rises on hapless households. Let me explain.

There is a compact between politicians and citizens in a democracy like Australia. Essentially the former serves the needs of the latter or they get thrown out. There is no such compact between central bankers and the citizenry of the jurisdiction that they govern although all sides assume that the central bankers will be doing their best to steer a steady course through economic icebergs as they come into view.

It sounds like I’m an apparatchik when I say this but as a market guy who has sat through all the crises in this economy and the globe since the late 1980’s I truly believe that probably no central bank in the modern age has done a better job of managing its economy. The last 20 years have, for a small open economy, often thrown enormous challenges.

Crisis after crisis they, along with the government and the floating exchange rate, the RBA has been able to get our economy through unscathed. There has always been winners and loser but in aggregate Australians respected and understood what the RBA was trying to achieve.

But the bifurcation of the Australian economy such that you need $240 million in the bank just to get into the BRW rich list and where mining is making multi-billionaires out of people while in the cities and towns families are under pressure to make ends meet, means that it is much more difficult now for the RBA to keep faith with the Australian population and its very important role in our economy and still hike next week.

That is certainly the case after weak data again yesterday. While net exports was the banner number with a negative 2.4% print, almost guaranteeing a near -1% result for the first quarter GDP, the key for us was, as ever, the credit data. Private sector credit was flat at 0.0% on the month and continues to speak volumes for household retrenchment. Why is this so important? Because we believe in a developed economy it is the demand for credit that sets the speed limit for economic growth. So while business credit is in a nascent pick-up, something the RBA has noted, the growth rate in housing debt is falling and other personal debt is dropping away. Indeed demand for housing credit is at its lowest in 30 years, probably more, as we noted yesterday. The RBA has articulated a mining boom centric policy approach but the data suggests things are worse on Main Street than they recognise or are at least permitting themselves to acknowledge publicly.

This lack of either understanding or disclosure is complicating life for commentators, but crucially NOT the market. I don’t want to turn this into a bash the economists piece but I must note one thing that is vitally important to know when you hear them speak – they play the man not the ball. That is, they try to forecast what the RBA is doing as opposed to what the economy is doing and therefore what the RBA should do.

One of Australia’s most senior economists has been tying himself in knots trying to explain why the RBA is going to hike, even as we’ve seen him discuss the pressure households are under in vehement clashes in semi-public. Others, such as our friend Mr Carr, think that they have understood the message that the RBA was sending on in the May SoMP and so ignore any evidence to the contrary which suggests the economy might not be on such solid ground. Whatever the RBA do next Tuesday or the following month or months I’ll guarantee you they aren’t rigid. They understand that the pieces of the puzzle change their shape and that of the pieces around them once you put them in place. Some commentators do not.

So it is that many of the commentators who felt like teenage boys and got over excited on the release of the SoMP and called for a rate hike in June have, with much less fanfare than the previous call, walked slowly away from a June hike hoping that no one would notice. We saw more of that yesterday with one of the majors pushing their call out to July while others had already gone from June back to August and Septmeber and some are pretending that comments on radio don’t count because they never put them in print.

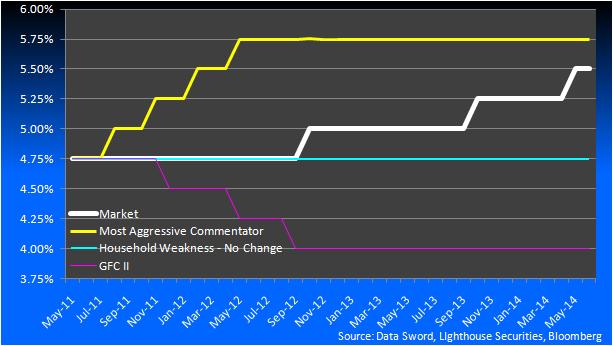

But as David Uren argued the other day in the Australian the market just never believed it and believes it even less now. Here is the chart –

- The white line is what the market now expects as movements in the cash rates – note it is now over a year until we get a full 25bps hike.

- The yellow line is the most aggresive call in the market and I would say the path to full blown recession

- The Blue line is what I think the RBA should do – no hikes and

- The Pink line is what happens if they mess Greece or Ireland up and we get GFCII

The RBA is on record saying that they don’t like to shock the market, it impacts their credibility, but the maarket is telling them they are wrong. I know short end traders who have been doing this for over a quarter of a century who swear that the next move will be down because the RBA has already done too much to households. I hold a similar view on households.

But the RBA has a medium term mandate, they grant themselves flexibility to manage this medium term mandate when it is necessary. We know they have a central tendency that says that the Chindia boom is multi decade and generational in nature. We’ll grant them that.

But if the RBA wants remain faithful to its tenet of “do least harm” then it needs to grant itself the flexibility to wait a few more months and see how this economy is really going. Not to do so is to risk losing its precious credibility with the Australian population.