Readers of MacroBusiness have turned my attention to a recent “AskNoel” question on Domain from 2 (early) baby boomer investors.

Q. I’m 48 and my husband is 55. As a result of renovations blowing out to $300,000, our mortgage is $690,000.

Our home is worth $1.1 million. We have two positively geared investment properties, owing $280,000 and $525,000, with about $100,000 equity in each.

Our incomes are $95,000 and $76,000 and we have $200,000 each in super. Should we sell one rental property and pay some off our mortgage or buy another investment property to minimise tax?

With my previous experience in the financial planning industry I’m not surprised at this situation and the low financial education of the couple involved.

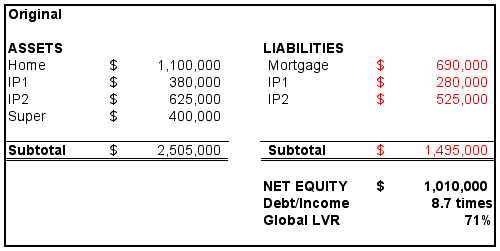

Noel Whittakers slightly contradictory response rightly pointed out that this couple, with net assets of just over a million dollars (see table below), have relatively low tax rates, with the husband near to retirement/preservation age.

And yet they are considering buying another investment property to minimise tax?

Assumed current portfolio

Transition Strategies

This transition of wealth accumulation to wealth preservation in retirement is a tricky situation for this nation’s baby boomers. As The Unconventional Economist has pointed out, it is this demographic that is most likely to own 1 or 2 investment properties – with relatively modest LVR’s but usually negatively geared (I question if this couple really are positively geared: the interest on their IP mortgages alone is $63,000 or so: on an average 4% gross rental yield, the rent would only be $40,000…..) and a high concentration of their paper wealth in their home with minimal superannuation.

So as a group, they are moving from a high taxable income with a leveraged concentrated portfolio to zero/low tax lower income with assets that only work if tax-advantaged. Negative gearing makes no sense (nonsense?) if your marginal tax rate is zero.

Risk is Risk

It appears that this couples financial plan rests almost solely on having $2 million worth of property for retirement – with a paltry $400K in super.

So what should this couple do? Keep the IP’s and stay the course? Sell one and pay off some of the mortgage? Buy another property? Salary sacrifice into superannuation? Or something different entirely?

Financial planning is not about getting the best mathematical result – its about weighing up the risks and considering opportunities whilst providing a robust forecast of what could happen. Simply saying “Strategy A will give you the best tax outcome so I advise this” is foolish advice at best.

Let’s look at the options from a risk/robust/opportunity point of view:

Keep the IP and Stay the Course

Residential property is likely the most riskiest asset class in this country. Some say it will double every 10 years, as it has in the last 25 years, or “average” 7% a year along a nice bell curve. Suffice to say this blog has analysed and considered the continuation of this paradigm and consider it over. This time is not different.

By choosing this route, this couple – and the 1.7 million other property investors out there – are exposing themselves to probable reductions in their paper equity and cool words from their bank manager due to their increasing LVR. A 20% decline in valuations would increase this couple’s global LVR from 71% to 88%. That’s LMI/FHB territory.

Rents aren’t going to experience any massive jumps in the years ahead. There is no shortage of properties to rent, and rents move along at a similar pace to CPI (approx. 3-4% pa).

Moving from property to super, this couple has nowhere near enough to fund their retirement. Assuming they both aren’t salary sacrificing much into super (and how can they whilst servicing a $690,000 mortgage on a $170,000 pre-tax income – approx. $60K a year in payments doesn’t leave a lot for expenses) their likely super balance will be in the range of $700K at retirement, providing a tax free pension of about $30K a year (equivalent to $40K in pre-tax earnings).

Not exactly a comfortable retirement – remember by then, their mortgage is likely to be reduced to approx. $480-600K (depending on when they retire) – yet the repayments won’t have changed, still some $60,000 a year – assuming interest rates don’t rise or one of them doesn’t lose their job.

Forget about it. This strategy is a losing one – unfortunately it will be the majority who cling to it in the years ahead.

Buy another IP

Take on more debt just to reduce tax on income that is just about to become tax-advantaged, whilst leaving a whopping great big mortgage on the family home? Read above again, slowly.

Pay off the Mortgage

Now we are talking some sense. Consumers forget that the headline interest rate on your mortgage is post-tax. That means it takes on average, an extra 30-40c of every dollar of your wage to pay off your mortgage (and most of this is interest, so its actually a multiple of that again to pay off principal)- so the effective interest rate is really closer to 11 or 12%.

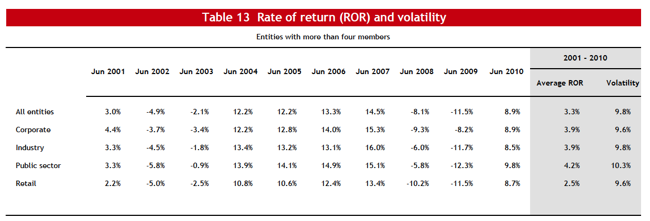

An 11% pre-tax return is fairly good in an inflationary environment or where your real earnings are increasing. Consider that the average super fund annual return for the last 10 years barely exceeds 4% (post-tax, so roughly 4.5% pre-tax).

Jan 2011 APRA Super findings - best average is 4.2% with 10% annual volatility

So you have to ask yourself – is it better putting your post- or pre-tax dollars into super and earn 4 to 4.5% or pay off your mortgage and earn almost double and leave yourself with a better income position that is robust to any unforeseeable change?

The caveat to this strategy are those with a DIY fund who can access a 7% term deposit (or who invest in an absolute return fund manager) and can salary sacrifice meaningful amounts into super (in this case 85 cents of each dollar of income is invested, whereas its only 65-70 cents of every dollar paying down your mortgage).

This strategy is appropriate with someone on a high wage (at least 37% marginal tax rate) and with a modest mortgage (i.e repayments are equivalent to paying rent, so its not a lost opportunity cost).

Salary sacrifice/contribute to Super

Debates about fund manager fees aside, there are two very large risks with superannuation. The regulatory/legislative risk exposes those saving for retirement to constant changing of rules and the possibility of increased tax and/or allocation or even access restrictions. The lack of risk-adjusted returns for most funds, that exceed the nominal cash rate or inflation completes this pair of nasty truths (see chart above again)

For this couple contributing to super the entire CGT-adjusted equity realised in selling one or even two or their IP’s still leaves them with a very large mortgage. It may also run them foul of “over-contributing” – yes, you can get penalised for trying to save for your retirement with some very punitive tax rates.

To help increase returns in super, the best way to get out of the industry and retail fund poor performance (and in some ways to be more flexible around ridiculous constant tinkering with super regulation) is to start a Self Managed Super Fund. Contrary to popular belief, you don’t need $200K and it doesn’t cost the earth to set up and maintain. There are some risks and administration problems but this is what comes with being responsible for your own money and future.

One of the best strategies is to go to the bank and plonk most of your super into a high returning (7% plus) medium term deposit. Immediately you are now exceeding the average return of almost all super funds (except those run by The Prince – shameless spruik). Although a “Great Inflation” may be on the way, or even here already, the consensus is towards higher interest rates to tackle inflation. We are clearly at a macroeconomic inflection point where higher rates that pay more on your cash earning you a greater return, will devalue, deflate and possibly depress asset prices of shares and property.

A better way

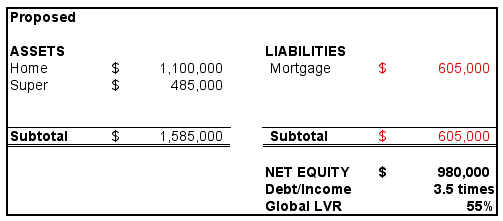

For this couple, it is obvious they don’t need any further tax advantages at the expense of increased exposure to risky and overvalued assets – they need income and they need to pay down their debt. The holding costs of the IP’s versus their “return” are far too risky: better to sell BOTH properties while they still can and use half of their after-CGT equity to pay down their mortgage and half to contribute into super. (Using an average 33% tax rate and the 50% CGT discount the $200,000 in paper equity would realise $167,000 after tax, more if the super is contributed concessionally). Although they give up future rental income – a proper opportunity cost to be sure – this is offset by the reduced risk and the ability to earn better returns in other assets.

Next, the husband should start a Transition to Retirement Pension (TTRP), thus increasing his super returns by 15% at a stroke (there’s no tax on earnings in the pension phase). This strategy has you salary sacrificing most of your income down to the same tax rate payable in super (15%) whilst drawing a tax-free pension to make up the post-tax income shortfall. It also means no additional funds placed into super (net), so they can concentrate on paying down their mortgage before retirement.

Lastly, they both need to tactically re-allocate their super balances out of what is probably the default “balanced” option into the cash option – for their age, at least 70%. The remaining should be a mix of equities, preferably international, with some exposure (if possible) to physical gold and other forms of insurance (life/TPD/income protection).

Proposed rebalanced portfolio

This is a more robust portfolio for this young Baby Boomer couple and gives them the flexibility to weather any storms, or take advantage of opportunities ahead.

Summary

Baby Boomers close to or considering retirement had better get their act together. The risks of relying upon continued asset values in property to remain high will leave many exposed if the situation worsens and Australia ends up turning Irish, American or Spanish.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no interest in any business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.