On Monday I posted a technical piece saying the the Australian Dollar had hit resistance and so far it appears that the 1.1014 level has proved to be the ceiling that I thought it was going to be. It was tested on two distinctly seperate occasions on Monday Sydney time and then again in New York for 2 hours that night. So technically it looks fairly solid for now. Here’s the chart:

What the piece didn’t do was look at the fundamentals so it was timely when on Monday afternoon I recieved a fundamentally based piece from John Kyriakopoulos who is the Head of Currency Strategy at NAB.

JK reckons that above 1.10 the Aussie is starting to look stretched.

Advertisement

AUD/USD above 1.10 would start to look clearly expensive on medium-term valuation criteria such as the terms of trade or current account balance.

But he is not by any stretch of the imagination bearish. Like your humble blogger, he reckons the underlying support remains solid.

Our long standing view is that the average AUD/USD rate over a full cycle is shifting up to 0.90 from the 0.70 averaged in the twenty years after the floating of the currency in December 1983. This outlook is based on Australia’s terms of trade averaging 50%-60% above the long-term average over the next decade. Above 1.10, AUD/USD is over 20% higher than our estimate of the new long-term average exchange rate. So the cyclical drivers of the currency, such as the wide yield differential, would need to persist and perhaps even widen by more than currently expected, to keep the AUD above 1.10.

Advertisement

Notice where JK has the average, he thinks that it is going to move from the 0.70 to 0.90. I happen to agree that something in this order of magnitude is more likely the result of the positive convergence of economic and investment fundamentals and crucially this is important information that needs to be given to Australian businesses.

This is especially so for two reasons:

It means that levels up around 1.10 won’t likely be sustained indefinately and

Nonetheless, plan for a higher exchange rate through time in your forecasts

JK makes a good point about the relationship between the Aussie and the current account deficict and how these two relate, you might say correlate. He says:

Advertisement

Alternatively, we might be wrong about how high the new long term or equilibrium AUD/USD rate has shifted. One argument in this regard is the very favourable outlook for Australia’s current account balance.

Our long standing view is that Australia’s shrinking current account deficit argues for a re-rating of the AUD and justifies a significant structural appreciation in the currency such that its average over the next decade could be 30% above that averaged in the 20-years after the floating of the AUD in December 1983.

In recent years Australia’s current account deficit has fallen sharply to an estimated 1.2% of GDP in 2011 (NAB forecast) compared to a long-term average of around 4.5% of GDP and 6% of GDP at cycle peaks (including during the previous climb in commodity prices prior to the Global Financial Crisis).

The sharp rise in Australia’s household savings ratio has meant that that a much higher share of Australia’s investment is being funded domestically. Witness the sharp growth in household

deposits. Indeed, household savings has risen by more than 5% of GDP since 2005 (when households were net borrowers). So while higher commodity prices and shipments have boosted export receipts, growth in imports have been relatively modest.

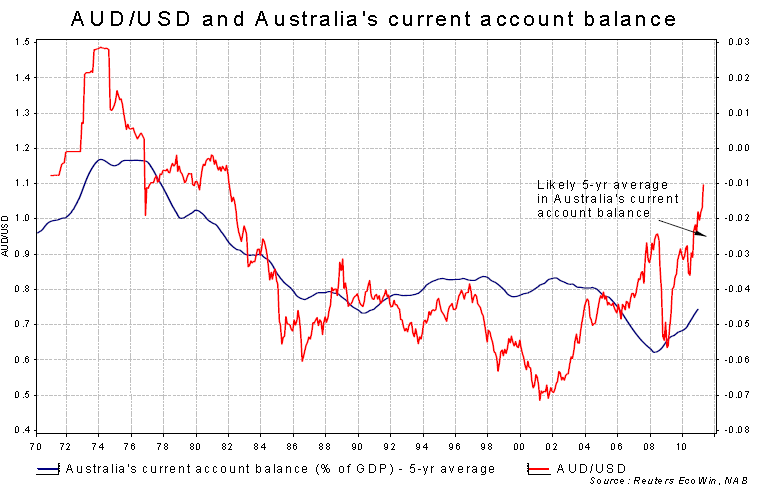

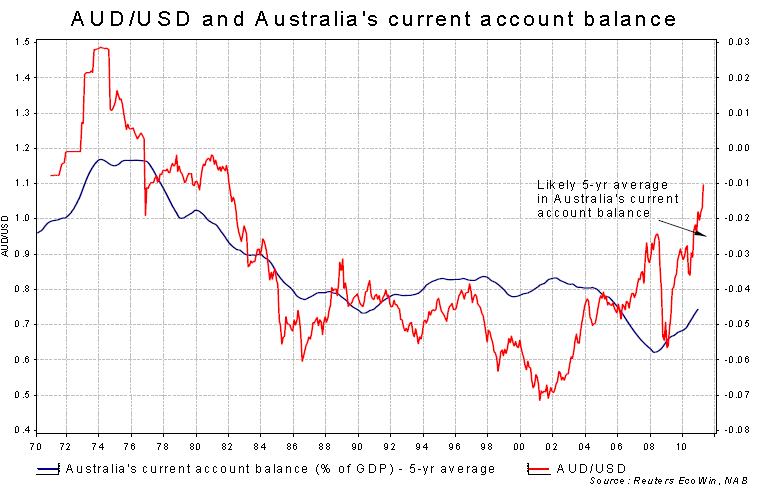

A much lower Australian current account deficit suggests the AUD isn’t overvalued as purchasing power parity would suggest. If the exchange rate was significantly overvalued then Australia would soon be running consistent trade deficits and the current account deficit would widen significantly. If we eyeball a chart of AUD/USD versus the current account balance then to justify +1.10 we’d need to see the current account deficit averaging less than 1% of GDP in coming years. The IMF’s current forecasts are for

Australia’s current account deficit to average closer to 3% over the next five years which is more consistent with 0.90-1.00 as the new equilibrium AUD/USD rate rather than 1.10-1.20.

AUD at +1.10 would overshoot likely fall in current account deficit.

So at its essence JK is saying that the Aussie is at the outer edge of its envelope based on his reading of the fundamental tea leaves. These are medium term considerations obviously and don’t really help those businesses being buffetted by the current Aussie strength, but they are important in ensuring that businesses don’t panic up here and lock in foward cover. Options are your best bet if you are worried. At least then if JK is wrong and it does drive higher you have cover and if he is right then you still participate in the Aussie’s pullback.

For mine the jury is out on where this long term high will be. $1.1014 is it for the moment but I think a lot of the re-rating for the Aussie and Australia still has to be worked through. I wouldn’t rule out an eventual push higher. Or, more likely, if and when the USD forms a solid base that the Aussie’s strength rotates into the crosses such as the EUR and GBP.

Advertisement

But the key here is that JK’s fundamental analysis has converged with my technicals analysis to deliver a very strong signal that the top is in for now.

Disclosure: This post is not advice or a recommendation to buy or sell. Do your own research and consult an adviser before allocating capital.

{kind=link}

{kind=link}