In 2008, the Australian Bureau of Statistics (ABS) released long-term population projections for Australia under three scenarios:

- High growth scenario (Series A), which assumes an increase in the fertility rate, higher net overseas migration than existed in 2008, and an increase in life expectancy;

- Medium growth scenario (Series B), which largely reflected the trends in fertility, life expectancy at birth, and net overseas migration that existed in 2008; and

- Low growth scenario (Series C), which assumes low assumptions for fertility and net overseas migration.

The assumptions underpinning these projections are provided in the table below:

And the projected trajectory of Australia’s population under these assumptions is shown below:

Over the next few weeks, I intend to write a series of posts examining the impact of Australia’s changing demographics on various areas of the Australian economy.

In today’s post, I will focus on the expected impact of population ageing on Australian consumption expenditure, which includes retail spending.

To illustrate the link between an economy’s age structure and consumption expenditure, consider the below chart showing the average weekly expenditure of Australian households by age group, taken from the latest ABS Household Expenditure Survey.

As you can see, household spending peaks between the ages of 45 and 54, before falling sharply. A household in retirement (65+) spends less than half of what a 45 to 54 year-old household does.

This relationship between a household’s age and expenditure has also been recognised internationally by world famous demographer and author, HS Dent, who claims that spending typically increases until age 46 and then begins to decline (see below chart).

")

Now consider charts of Australia’s projected population, split-out by age group, under the three growth scenarios discussed at the beginning of this article.

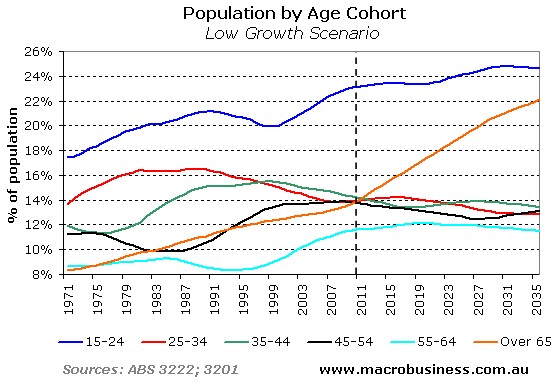

First, the low growth scenario (Series C):

{kind=link}

As you can see, under the low growth scenario, the share of the population at the peak spending age of 45 to 54 (black line) is projected to fall gradually over the coming decades from its current high level as the Baby Boomers enter retirement. The second highest spending cohort – those aged 35 to 44 (green line) – is also projected to fall as a share of the population.

Now contrast these outcomes with the frugal 65+ cohort (orange line). Their share of the population is projected to increase rapidly over the next 25 years as the Baby Boomers retire.

Taken together, the outlook for consumption spending under the ABS’ low growth (Series C) assumptions is particularly bearish, with the higher spending age groups declining in share relative to the lowest spending age group.

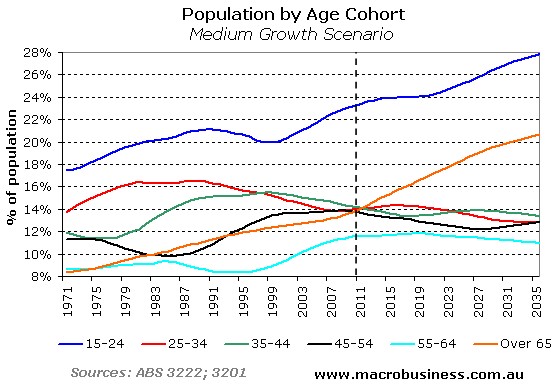

Now consider the medium growth scenario (Series B):

{kind=link}

The outcome is essentially the same as under the ABS’ low growth scenario.

Again, the two highest spending cohorts – those aged 45 to 54 and 35 to 44 – are each projected to fall as percentage of the population. By contrast, the frugal 65+ age group is projected to increase significantly in relative size, albeit by slightly less than under the low growth scenario.

Overall, the outlook for consumption spending under the ABS’ medium growth (Series B) assumptions is also very bearish, with the higher spending age groups declining in share relative to the lowest spending age group.

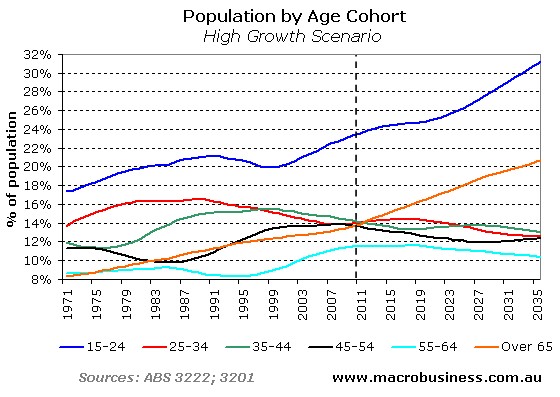

Finally, consider the high growth scenario (Series A):

{kind=link}

Again it’s more of the same, with the two highest spending cohorts – those aged 55 to 64 and 35 to 44 – each projected to fall as a percentage of the population, with the lowest spending age group – those aged 65+ – expected to increase it’s share.

The key difference between the high growth scenario and the low growth scenario is that the 65+ cohort is projected to increase in share by slightly less, whilst the proportion in the 55 to 64 age group is projected to fall by more.

Despite the subtle differences between the scenarios, the negative long-term outlook for consumption is much the same, with the higher spending age groups declining in share relative to the lowest spending age group.

And with the Australian retail sector already under siege from household disleveraging and falling home prices (reported here and here), the impending retirement of the Baby Boomer generation provides yet another unwanted headwind.

In my next post, I will examine how the ageing of Australia’s population might affect asset values.

Cheers Leith