In yesterday’s article I looked at what a housing correction may do to the Australian share market – both from a macro economic point of view as well as the company level. We discussed which stocks would be exposed and some that may not.

In yesterday’s article I looked at what a housing correction may do to the Australian share market – both from a macro economic point of view as well as the company level. We discussed which stocks would be exposed and some that may not. So now let’s see what opportunities a correction may present the courageous value investor – because there is always a silver lining.

In the Beginning..

Well, the first thing to do is cash out any investments that would be exposed to the correction. Once your portfolio is cash heavy you can either:

1. Sit on the sidelines and watch the ASX 200 fall, or

2. Short a few stocks

During the Tumble..

As house prices and the markets continue to drop, Empire Investing will be watching those companies with reliable foreign revenues whose share prices may get caught up in the market rout – COH, CST & CSL among the prime candidates. Otherwise, we’ll look for other companies whose prices drop substantially below their estimated value. Should nothing come up, then we’ll continue to wait.

After the Landing..

Eventually the correction would come to an end and both the housing and equities market will find stable bottoms. This is the time when real bargains can be found as the market oversells everything in sight. As mentioned above, non-discretionary retailers such as WOW and CCL should be examined, although they are less likely to be oversold because they are considered “defensive” stocks.

In the discretionary sector, low-value seller TRS should bounce back well, although a lower AUD will impact on its margins. As an already lean operator, JB Hi-Fi should also see the crash off and emerge with fewer competitors and in a stronger position. Myer and David Jones should survive after a couple of poor years. If they can obtain their pre-crash return on equities, they should represent good value as investors stay away from higher-value discretionary retailers.

As the economy recovers, the well-known website-based companies (e.g Seek, Carsales.com.au, Wotif and RealEstate.com.au) should also make resurgences. The nature of their low-asset businesses means they can scale sales up quite easily, whilst their well-known branding will ensure returning customers. Empire will be keeping a very keen watch on this clutch of online businesses.

To round out the list of opportunities, one needs to examine the counter-intuitive plays. The property-related industries (development, mortgage broking, renovations, REITs) will be hit hard and many will fall. However, those that survive with stable equity bases and decent cashflows will be heavily discounted as investors flee anything that is remotely involved with property. As such, they’ll be a value-investors dream.

We believe Sunland Group may be among the survivors, whilst Westfield will most likely weather the Australian crash with its off‑shore revenues. In the supplies business, Reece will be the prize with an extremely dominant market position, a hard-earned brand name and an almost pristine balance sheet.

Any of the Big 4 banks may be a good buy if their share prices drop low enough (see The Princes post about the banks for more info). Mortgage Choice may also be a contender if its business model survives the correction. However, when revaluing any of the banks or property stocks one will need to assume a more conservative earnings profile. There will be no return to the pre GFC or pre-Aussie housing crash days. Banks with Return on Equity (ROE) in the very low teens and property trusts in the 5-10% range will probably be the new norm.

Will it happen?

How long is a piece of string? Smarter people than your author have called the housing peak only to see house prices climb ever higher whilst their credibility headed in the other direction. The Australian government has form at messing with the housing market and China is currently pumping money into our pockets. This means the peak will be harder to pick than a broken nose.

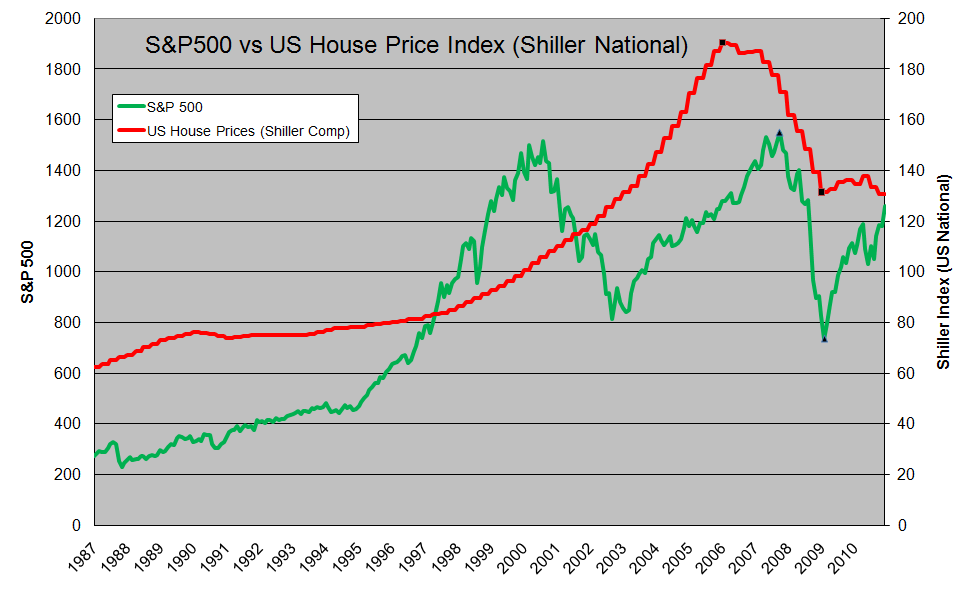

Forecasts among real estate bears range from a US-style crash to slow deflation of house prices over a long period. The following graph showing the S&P 500 vs US house prices shows a lag between the house price and equity market peak of over 18 months. So it is quite possible for these markets to diverge for a long time.

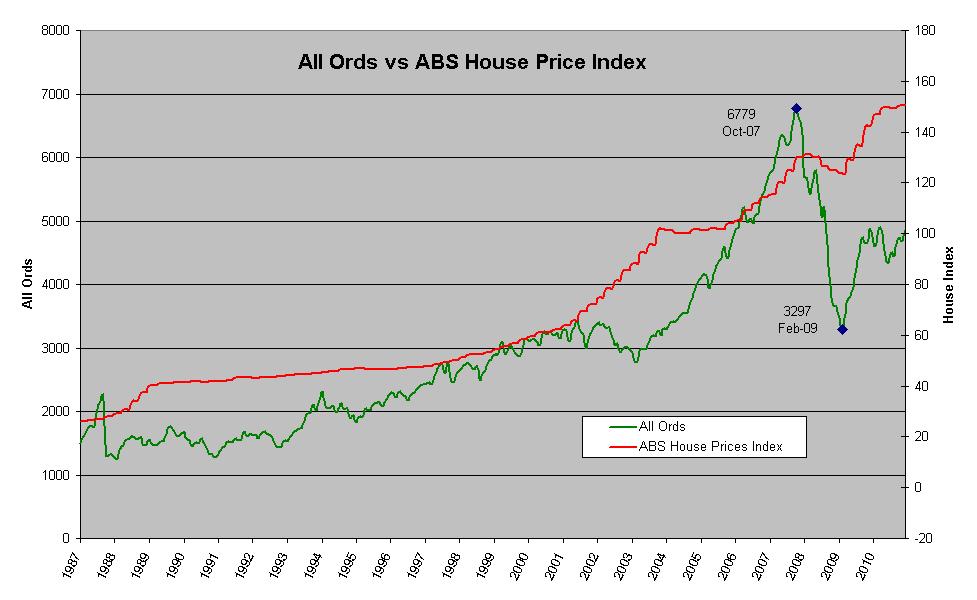

As a comparison, below is a graph showing the established Australian house price index (calculated by the ABS) and the All Ords figures.

At Empire, we’re not assuming a big housing correction. But we are maintaining high levels of cash and unwinding equities positions as they go past fair value. There is very little we’d consider buying at current market prices, so our cash position will continue to strengthen. In a sense, therefore, we are increasingly prepared if housing capitulates. Another option for the brave contrarian is increasing gold positions but it’s not really my cup of tea.

Shorting a market that has been heavily subsidised and historically bailed out/propped up by governments on both sides is a risky venture. Buying out of the money puts on the Big 4 banks wouldn’t be a bad idea for the betting investor (note that the ASX will introduce 100 lot sizes in May, allowing an easier exposure for smaller retail investors). However, they could expire worthless if the housing market stagnates or the government plays its usual tune and uses all sorts of measures for a bailout.

For some tuckshop money, we’ll be writing covered calls on shares we own, with the strike price at or above our required sell price. When the opportunity arises, we’ll write puts for shares we want to own at the strike price. But aside from that it’ll be high interest accounts and thumb-twiddling until a correction occurs.

If the correction does occur – and to quote my business partner The Prince – we’ll hit the market like the fist of an angry god, snapping up wonderful companies like WOW, COH and REH at rock-bottom prices. And finally, when property-investor blood is running through the streets and real estate agents start driving Kia’s, your author may even stop renting…

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has interests in some of the businesses discussed in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before allocating capital in any investment.