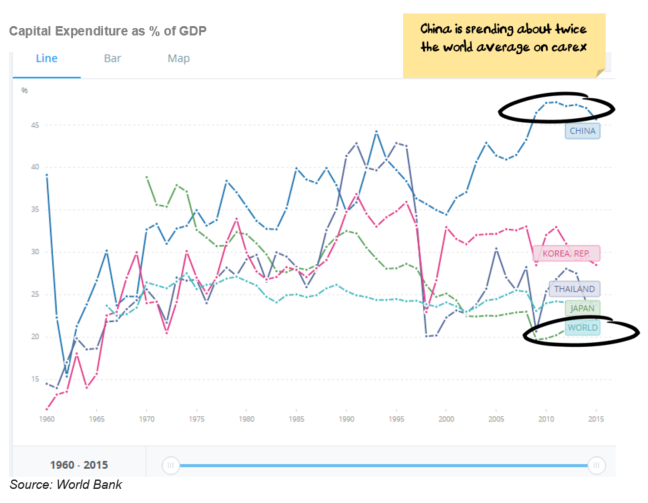

China is spending just under half of its GDP on capital expenditure, new roads, bridges, factories, airports and buildings. This level is much higher than any similar country has ever spent on capex since we started keeping records – the only country that came close was Thailand shortly before the Asian Crisis (for anyone not sure how that ended for Thailand, the word “crisis” is instructive).

Click below to watch our webinar or read below for a short summary of our view:

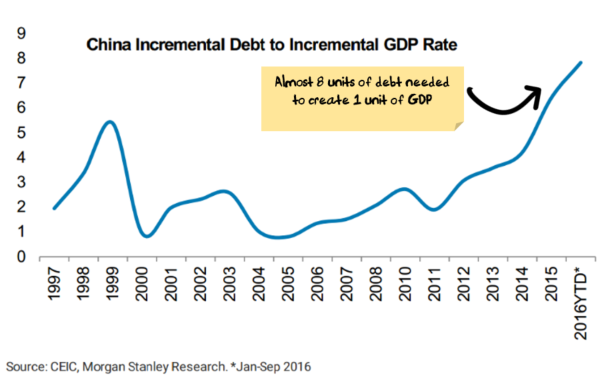

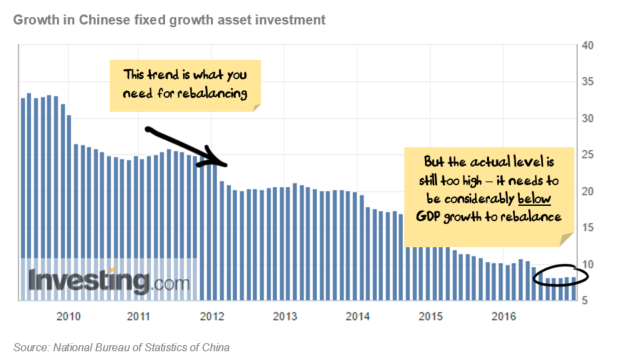

The spending, is increasingly debt funded, and each dollar of debt is having a smaller and smaller impact:

Sometimes it’s hard to grasp that not all investment is good. Specifically, an investment that does not earn a high enough return is not a good investment. Judging returns is hard enough to measure for commercial operations but when you are building things like bridges or roads then measuring the return as a “public good” is even harder again.

The parable here is that when you first start spending on capex you choose the most efficient investments first (give or take) and as time goes on you invest in projects that earn a lower and lower marginal return. For example, the first bridge across a river is very productive as it may save hours of transit time, the second less productive as now its saving transit time from congestion on the first bridge, and by the time the third and fourth bridges are being built the benefits are more and more marginal (and harder to measure).

At some stage, if the level of investment is high enough, this return will fall below the cost of capital – the key question is when? In my view, China is likely to have surpassed this level a few years ago – as the above chart indicates.

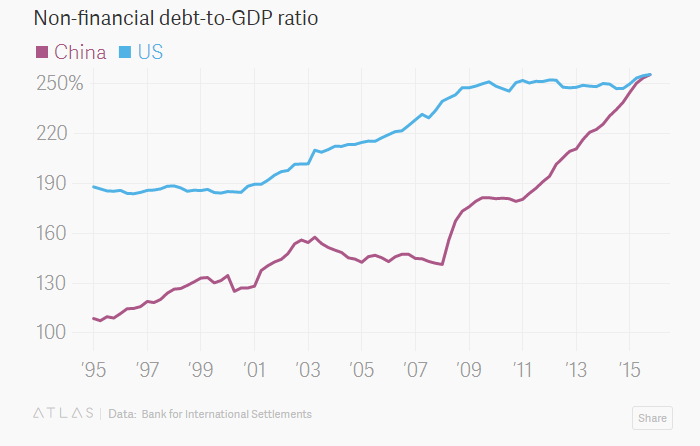

When does this end? i.e. how much debt capacity does China have left?

Chinese debt is high at around 250% of GDP. Its government deficit is running at close to 10% of GDP if you include debts being accrued by local governments.

So, not much debt capacity left. Having said that, China could probably scrape another few years out without too many issues. But, the current path is clearly unsustainable.

What other structural issues are there?

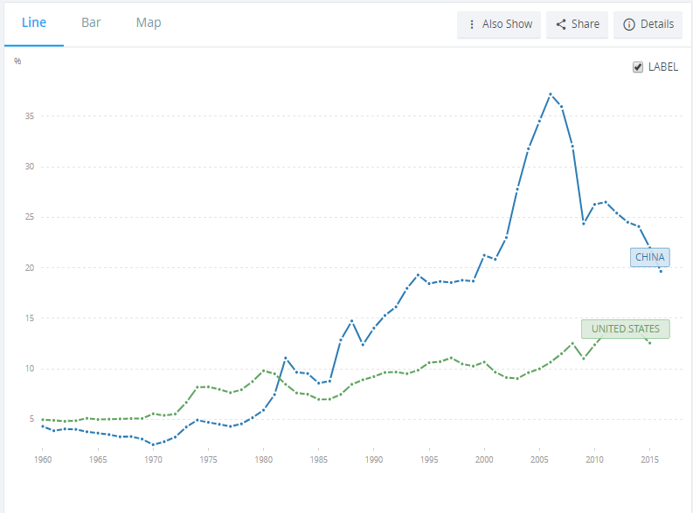

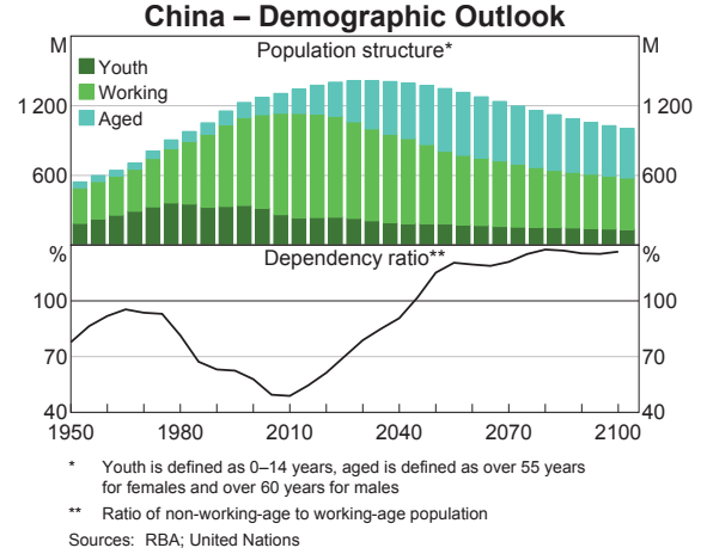

A lot of the growth in the Chinese economy has been driven by exports and favourable demographics. We don’t expect either of these to be helpful in the coming years and demographics in particular will likely detract from growth:

Source: World Bank

If we assume at some stage the Chinese economy will rebalance, then the key questions become how and when?

For the “how” question, we are unsure – in the vast majority of similar cases, investment spending continues to increase as long as it can before ending in a crash (e.g. Russia, Japan, the Asian crisis). Basically, the level of investment spending gets so high the entire economy becomes dependent on creating investment, and it is hard politically to diversify away from this as it involves short term pain for a longer term gain.

There is some hope that this time China will be able to rebalance more gradually – they have recognised the problem at least in their five-year plan, the question is whether politically it is possible to make the change given:

- it is likely to generate higher short-term unemployment

- local governments have become dependent on profits from land sales

- vested interests will likely lobby to maintain the construction spend

Forgetting the political issues for a moment, let’s make the assumption that China wanted to rebalance smoothly over the next ten years back to 50% consumption, 30% investment (which would still put them at the top of the world for investment as a % of GDP).

If consumption started growing at 12% real (say 15-16% nominal growth which is a relatively heroic assumption) and gradually edged down to 8% (11-12% nominal) per annum over the next ten years, then investment would have to grow at 0% to rebalance the Chinese economy. And investment growth is currently well above 0%.

So, on the “when” question the answer is the sooner the better. The longer it takes for the rebalancing to start, the more likely that it ends in a crash rather than an orderly transition.

The real question is how much ideological conviction to Chinese politicians have in rebalancing?

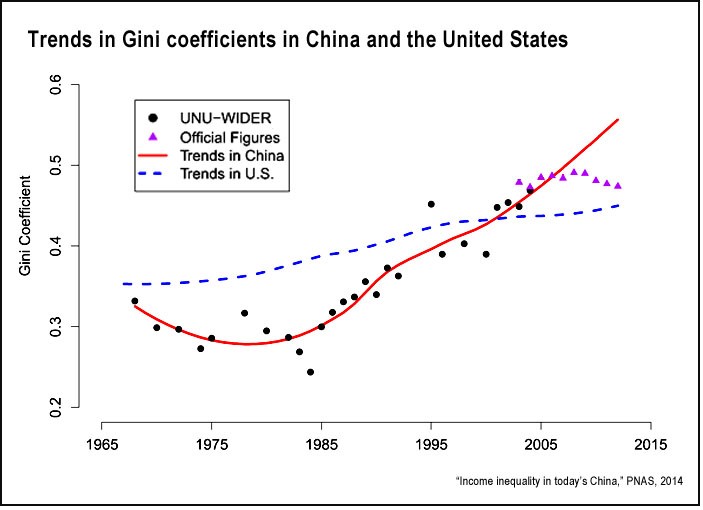

While Chinese GDP growth has been impressive, the growth has not been evenly dispersed among Chinese citizens. Estimates of the Gini coefficient, which measures inequality, have grown dramatically in China and suggest that China (ironically for a communist nation) has one of the world’s most unequal wealth distributions.

The inequality creates a number of issues. I am going to ignore the potential for large-scale political upheaval, not because it is unlikely but because human beings have proven to be very poor at predicting regime change and I am unlikely to be any better. It’s a risk that needs to be kept in mind, but there is little an investor can do right now as regimes can last decades beyond expectations or fall within weeks of experts decrying any possibility.

What the imbalances do create is something MB readers are used to reading about and something I am much more comfortable forecasting – political self-interest.

The growth in wealth for a (relatively) small number of people within China has been spectacular and has been based on the existing arrangements where investment growth is high.

Additionally, local governments are highly reliant on land sales to developers. Reports about Chinese party officials owning tens or even hundreds of properties, plus that China does not rate well on most measures of corruption (on the Transparency International 2012 study China was ranked 80th, citing graft, bribery, embezzlement, backdoor deals, nepotism, patronage, and statistical falsification) suggests that the relationship between party officials and developers is unlikely to be entirely above board.

So, rebalancing means less development which then means less chance for lower level communist party officials to “supplement” their income. As rebalancing occurs, it will create (probably quite intense) political pressure for the Chinese leadership.

Does the Chinese leadership have the fortitude to stand up to vested interests?

No one knows – probably not even the Chinese leadership.

What this means for investors is that it is wise to position portfolios for a rebalancing, but to be mindful that as the rebalancing occurs that there will be a risk that leadership will cave to vested interests and begin another round of stimulus.

For Australian investors, we also need to be mindful of the reduction in demand for commodities.

What is the end game?

My bet is that China will follow the Japanese path – spend as long as they can, then bundle all of the bad debts up into banks and zombie companies, followed by decades of economic stagnation where the economy goes nowhere but unemployment never gets too high, household incomes keep growing, and the Communist Party stays in power. Add in a rapidly ageing Chinese population and the parallels might be a lot closer than many imagine.

The danger is that they get it wrong and either an economic crisis or a political upheaval occurs.

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.