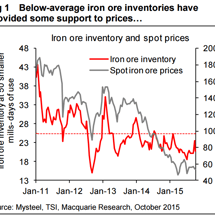

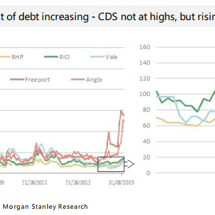

Hedgie: BHP to get smashed

From the AFR: Ben Silluzio, the chief investment officer and CEO of start-up investment firm, Qato Capital, thinks shares in BHP Billiton could fall 30 per cent by the time the mining giant reports its half-year results in February.