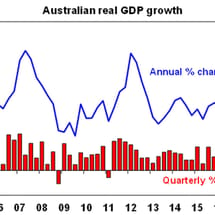

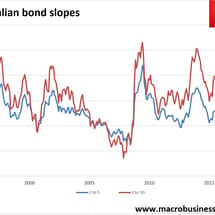

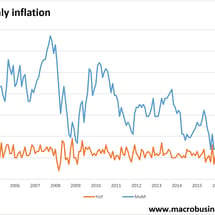

Kouk: RBA to slash rates, Australian dollar to crash

Via the Kouk today, given he and MB are the only ones to have gotten this right: In the wake of the September quarter national accounts, and with accumulating information on house prices, dwelling investment, the global economy and spare capacity in the labour market, I have revised my outlook for official interest rates.