Canada’s mortgage arrears are far lower than Australia’s

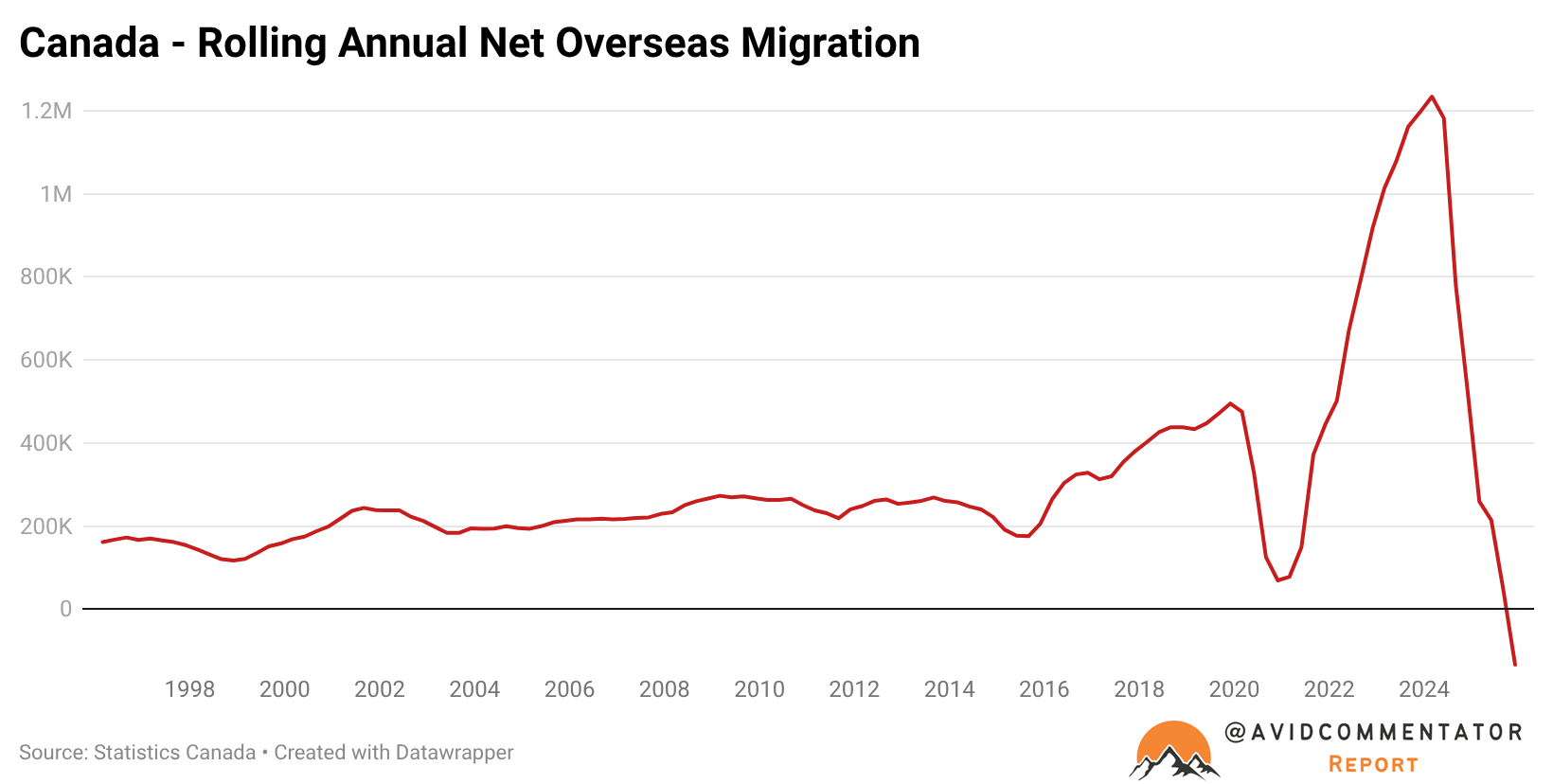

As the debate over the right set of economic, immigration and housing policies in Australia continues, Canada is often raised as an alternative pathway, one where housing prices and rents are falling and net overseas migration is a negative number.

But this different strategy, which ultimately rests upon a reality where the Canadian government lacks the ability to continue to grow the size of government and taxpayer-funded employment at a rate significantly lower than Australia, has seen unemployment rise by 1.8 percentage points to date in Canada, compared to 1.1 percentage points in Australia.

This has led to commentary in some quarters that this would be disastrous for Canada’s mortgage holders and that Australia possesses the superior strategy.

In order to quantify this difference, we will be examining data from the Canadian Banking Association and Fitch Ratings.

Since the Canadian Banking Association uses 90+ days in arrears as its metric for gauging the severity of households struggling to pay their mortgages, that will be the metric for today’s analysis.

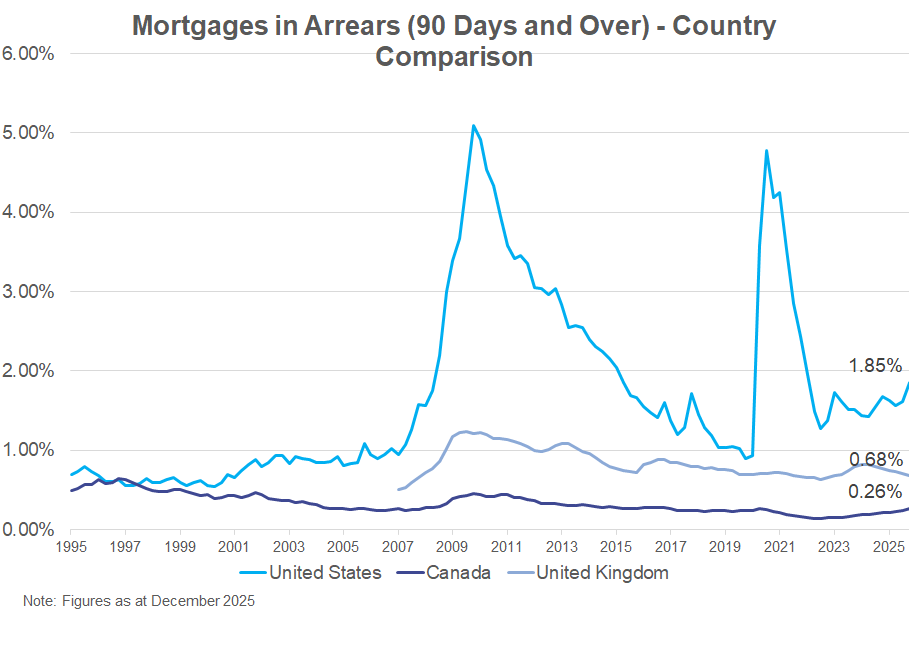

According to figures from Fitch, the proportion of “Prime” Australian mortgages it assesses as 90+ days in arrears is 0.59%, in terms of “non-conforming” mortgages, the 90+ day arrears rate is 1.99%.

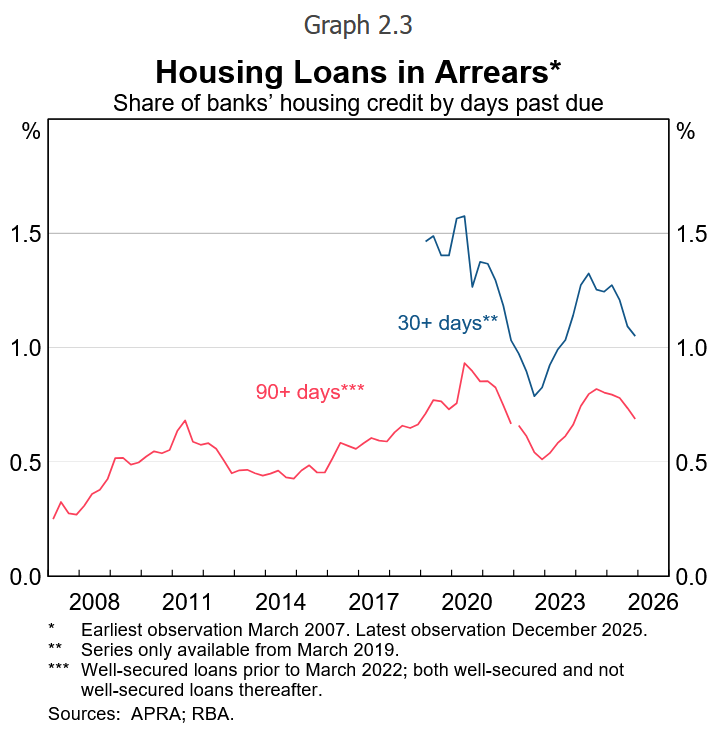

This is reflected in data from the RBA’s March Financial Stability Review, where 0.69% of total mortgages were 90+ days in arrears.

It is, however, worth noting that Australian loans subject to certain formal hardship provisions, such as a repayment pause or dramatically reduced repayments, are not counted as in arrears as long as the limited conditions on the loan are being met and this makes comparing arrears in the present with past eras when this distinction was not made.

Meanwhile, in Canada, arrears are on a different path.

According to the latest data from the Canadian Banking Association, the proportion of loans 90+ days in arrears is 0.26%.

As the chart below reveals, this is a level significantly below Britain and Canada.

Meanwhile, Australia’s current rate of 90+ days mortgage arrears is almost exactly on par with Britain’s.

Source: Canadian Banking Association

While there are arguments to be made for and against Australia’s and Canada’s respective strategies towards housing, the role of government in the economy and immigration, the issue of mortgage arrears is not one that favours the Australian strategy, despite Canada seeing far greater levels of downside in housing prices and at this stage a significantly larger rise in its unemployment.