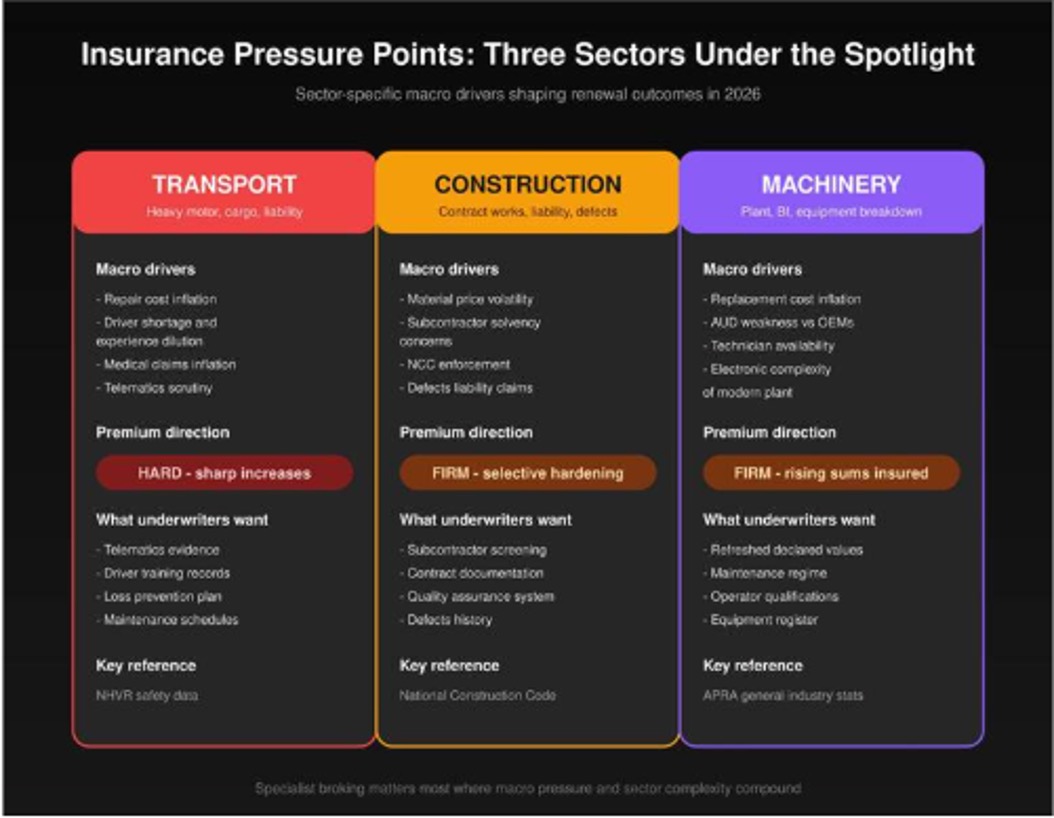

Transport, construction and machinery sectors are bearing the sharpest edge of Australia’s insurance cycle

(Feature Image: Bearing the sharp edge of the insurance cycle. Credit: Drazen Zigic/Getty Images)

The aggregate commentary on Australian commercial insurance markets through 2026 reads as cautiously optimistic, with several lines softening and capacity gradually returning. The aggregate, however, is hiding a sharp divergence at the sector level. Businesses operating in transport, construction, and machinery-intensive industries are still navigating one of the toughest premium and capacity environments in twenty years, and the underlying drivers are firmly macro rather than firm-specific.

For business owners and finance teams in these three sectors, understanding the macro forces that are shaping their renewals is the difference between accepting outsized cost increases and structuring their operations and risk presentations to recover meaningful ground at the next placement. The signal coming through the cycle is consistent. Sectors with high asset values, complex exposures, and visible loss experience are being repriced more aggressively than the broader market, and the gap is widening rather than narrowing.

Transport Has Become the Test Case

The Australian transport sector aggregates some of the most challenging risks in the commercial market. Heavy motor fleet exposures sit alongside cargo, public liability, business interruption, and increasingly cyber risk as fleet telematics and dispatch systems become attractive attack surfaces. The Bureau of Infrastructure and Transport Research Economics tracks the heavy vehicle activity that underpins this exposure, and the long-run growth in tonne-kilometres travelled has translated directly into more claims frequency for the underwriters covering the sector.

Heavy motor premiums have moved hard. Rate increases on prime mover fleets through 2024 and 2025 exceeded broader commercial inflation by a significant margin, and the structural drivers, repair costs for newer prime movers, technician shortages, and the rising cost of medical and rehabilitation claims, are still in play. The National Heavy Vehicle Regulator publishes safety performance data that has become an active input into how underwriters segment the transport market.

The Driver Shortage Has a Premium Cost

Australia’s heavy vehicle driver shortage, documented across industry bodies and government reports, is showing up in claims data. Operators forced to dilute their experience pool with newer drivers see correlated increases in claims frequency, and underwriters are using detailed driver experience information to differentiate premium outcomes. Carriers with disciplined driver training, telematics evidence, and visible safety culture are still securing competitive renewals. Those who cannot demonstrate that picture are paying for the average of the sector.

Construction Is Wrestling With Material and Labour Pressures

Construction insurance has been buffeted by the same cost dynamics that have been reshaping the building industry itself. The Australian Bureau of Statistics publishes the producer price indices for construction inputs, which have been a leading indicator of the rebuild costs underwriters are now using to price contract works and construction liability exposures.

Major projects insurance has hardened in line with project complexity and the visibility of delay and disruption claims. Subcontractor solvency exposures have become a board-level concern for principal contractors, and underwriters now ask much more pointed questions about supply chain resilience, retention practice, and the contracting structure of sub-trade engagements.

Defects Liability Is the Quiet Issue

Beyond the more visible major project lines, the long-tail issue creating the most analytical work for construction underwriters is residential and commercial defects liability. The combination of more complex building systems, energy performance compliance, and stricter regulatory enforcement under frameworks such as the National Construction Code has lifted the cost of putting defects right. Insurers covering builders and design consultants in these segments are responding with sharper risk selection and tighter wordings.

Machinery and Plant Are Caught in the Middle

Businesses that own or operate significant plant and machinery sit at the intersection of property, business interruption, and equipment breakdown exposures, and each of those lines has its own dynamic in the current cycle. The replacement cost of heavy machinery has risen materially since 2020, driven by both global supply chain costs and the depreciation of the Australian dollar against the currencies of major OEMs. Underwriters have updated their sums insured assumptions accordingly, and businesses that have not refreshed their declared values are at acute risk of underinsurance penalties at the next claim.

Equipment breakdown loss frequency has also crept up, partly because the increasing electronic complexity of modern machinery means more components can fail, and partly because technician availability for repair has tightened. The combination of higher repair cost per incident and longer disruption duration has produced a sharper-than-average premium response from the specialist underwriters covering this segment.

The Common Macro Thread

The unifying feature across transport, construction, and machinery is that each sector combines high asset values, significant third-party liability exposure, and operations that are deeply embedded in the productive capacity of the broader economy. When the macro environment delivers higher repair costs, longer service times, more frequent severe weather, and tighter regulatory enforcement, these are the sectors that absorb the impact first.

The Australian Prudential Regulation Authority publishes general insurance industry statistics that show how this divergence flows through to the capital that insurers allocate to each line. The lines most exposed to these macro pressures attract higher capital charges, which translates into higher premiums for the underlying clients.

Why Specialist Broking Matters More in These Sectors

The technical complexity of risk in these three industries has moved well beyond what a generalist commercial broker can credibly advise on. Heavy motor wordings, contract works extensions, marine cargo coverages for specialised plant in transit, equipment breakdown extensions, and the interaction between general liability and product liability for machinery dealers all require deep specialist knowledge. Working with specialist insurance brokers who advise primarily on transport, construction, and machinery risks has therefore become the difference between competent placement and genuinely strategic risk management.

Risk Presentation Drives Outcomes

Underwriters in these sectors are seeing more submissions than they can quote, and the quality of presentation has become a primary filter for which risks they engage with. A submission that demonstrates a credible operational story, supported by safety data, telematics evidence, contractual structure, and a clear risk improvement plan, will get attention. A submission that arrives as a generic data dump will increasingly not.

Practical Operating Implications

For finance and operations leaders in transport, construction, and machinery businesses, three operating habits move the needle on insurance outcomes. The first is keeping declared values and sums insured aligned with current replacement costs, refreshed annually rather than every three to five years. The second is investing visibly in risk management evidence, particularly telematics, training records, safety case files, and incident response data. The third is engaging a specialist broker who advises across the industry and can therefore benchmark the business against its peers when challenging premium outcomes.

Outlook for the Rest of 2026

The macro forces driving the hard market in these three sectors are not going to reverse in the next six to twelve months. Repair costs will remain elevated. Driver and technician shortages will continue to influence loss patterns. Climate-related event frequency will keep reinsurers cautious. The clients who navigate this environment best will be those who treat their insurance programmes as a strategic input to operations rather than a transactional renewal exercise. The macro tide will eventually turn, but the operators who reach the turn in the strongest position will be those who used the current cycle to professionalise how they present risk to the market.