First COVID. Then the Ukraine war. Then tariffs. Now the Iranian war. Plus massive government deficits in many countries.

At some point, the concern is that inflationary expectations will be permanently embedded in consumers’ and workers’ psyches. At that point, central banks might need to inflict some real economic damage to reset expectations.

How should we look at inflation reversion?

There are two ways to consider reversion:

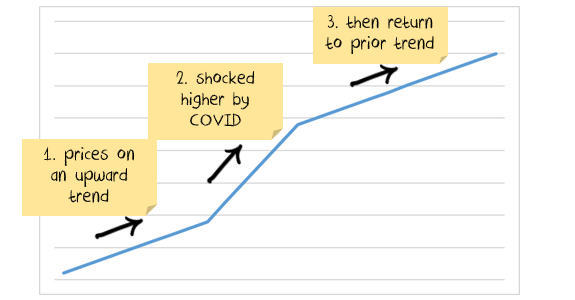

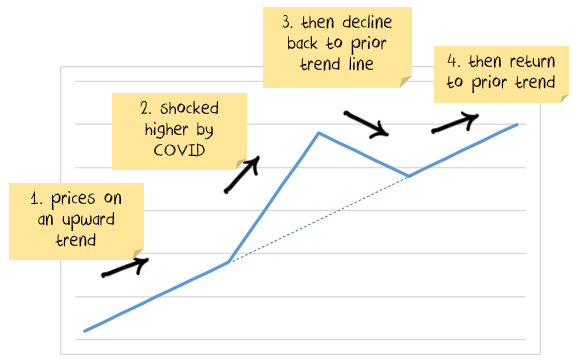

1. While central banks will force inflation back to 2%, prices will remain structurally higher.

2. Prices have been temporarily shocked, but will return to the prior trend

Goods are more likely to fall into the second category, while services are more likely to fall into the first.

The shape of future inflation or deflation depends on how many things you think will fit into each profile.

What is really happening?

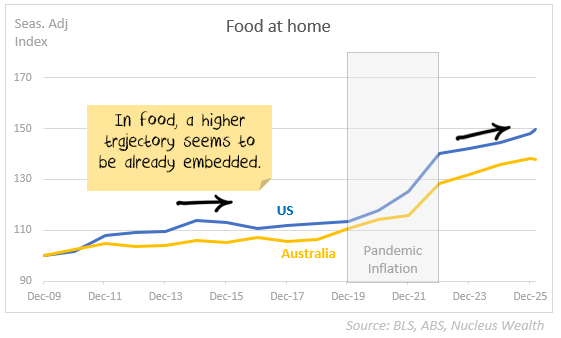

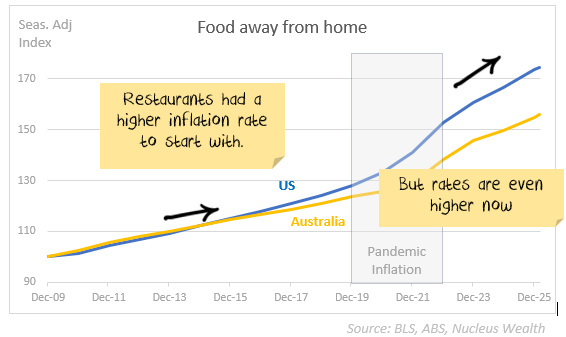

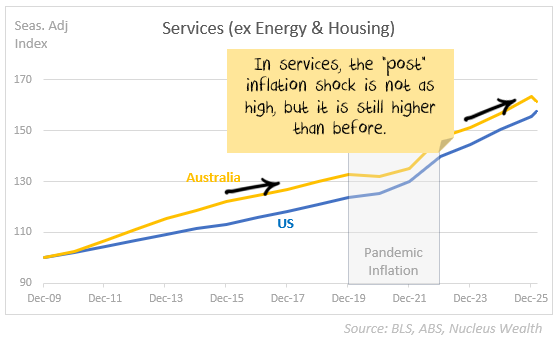

In most service categories, and in food, it appears that higher inflation is already embedded:

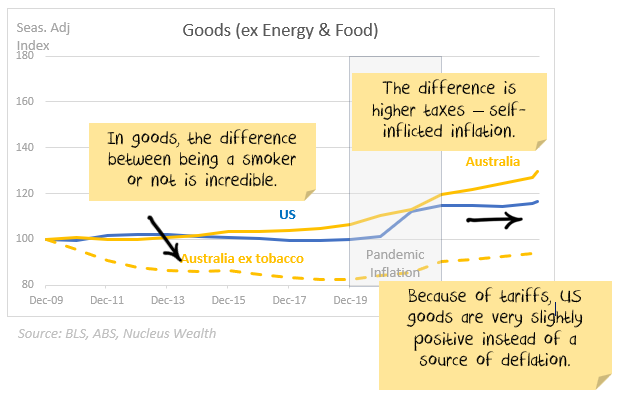

Goods are almost different, but policy decisions are causing higher inflation in both Australia and the US:

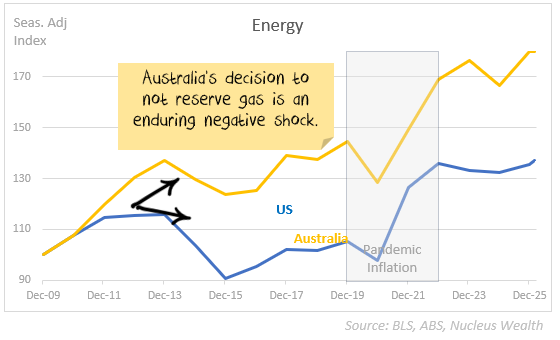

Energy is much more volatile and about to become more so. The biggest issue for Australia is that despite having an incredible amount of energy, a political decision has been made to open Australia up to world prices. Embedding higher inflation.

Can the RBA use higher interest rates to bring down world energy prices? No, it can’t. Which means it will need to damage the rest of the economy to tame inflation.

What should you do within your portfolio?

Long term: more equities, more inflation-linked bonds. But in the short term, there are other considerations. More on that another day.

Damien Klassen is Chief Investment Officer at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on X(Twitter) or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an Authorised Representative of Nucleus Advice Pty Limited, Australian Financial Services Licensee 515796. And Nucleus Wealth is a Corporate Authorised Representative of Nucleus Advice Pty Ltd.