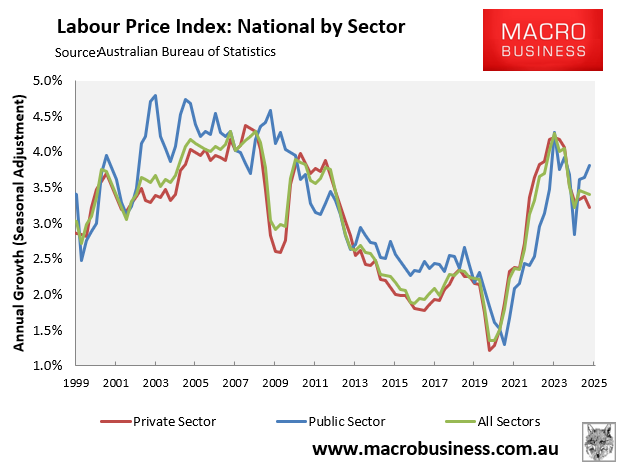

With the release of the latest ABS Wage Price Index for the September quarter, it was revealed that headline wages were growing right on analyst and RBA expectations, with wages up 0.8% quarter on quarter and 3.4% year on year.

But underneath the relatively pedestrian headlines lies a divergence in outcomes and significant falls in inflation-adjusted terms.

For the nation’s private sector workers, wage growth is trending down, with annual growth of 3.2% year on year, the weakest result since the June quarter of 2022.

On the other hand, for those in the public sector, the news is much more favourable, with wages up by 3.8% year on year.

Since the inception of the ABS Wage Price Index in 1997, public sector wages have grown more strongly the overwhelming majority of the time.

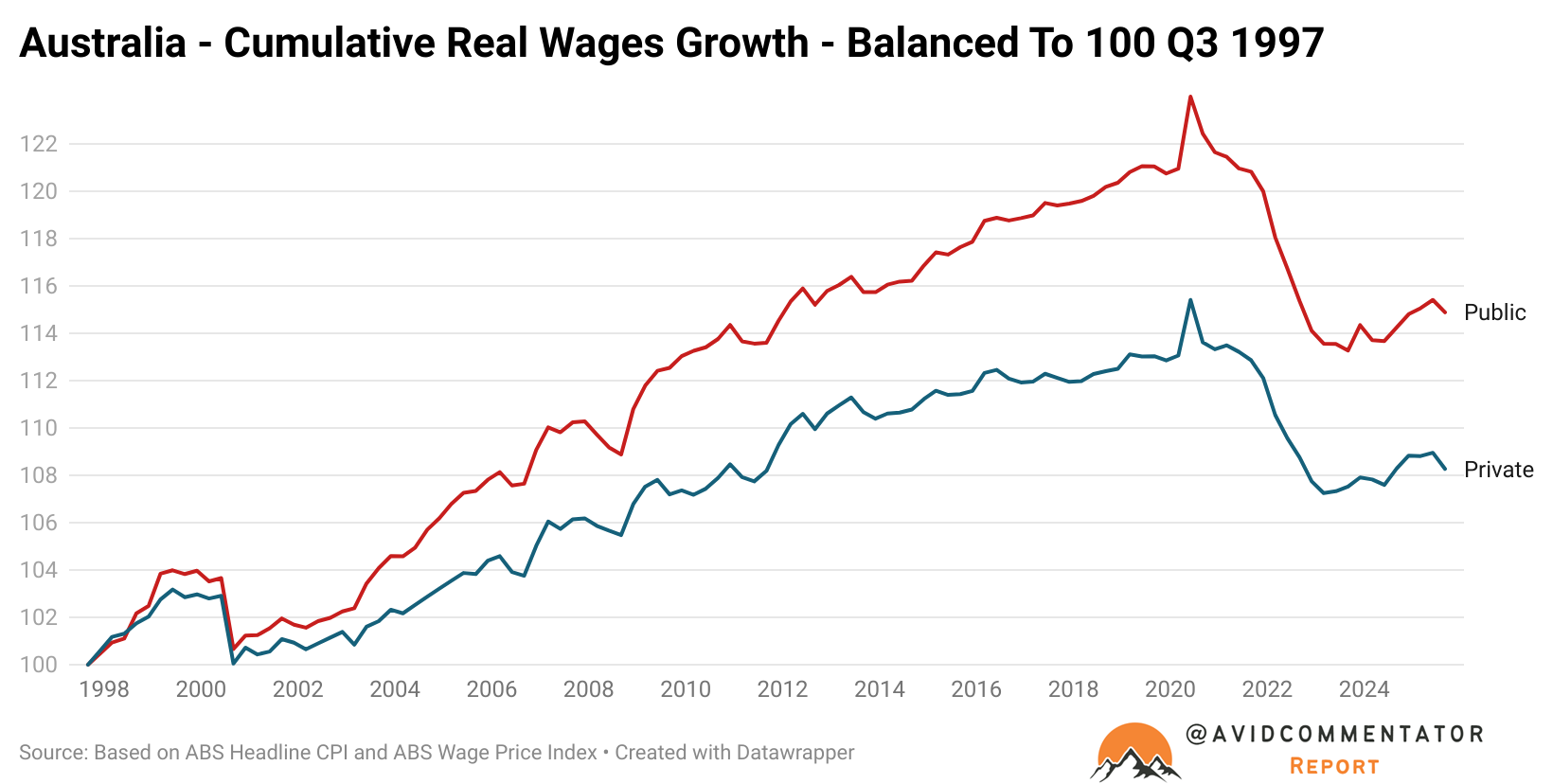

This has had major implications for real wage growth, as public and private sector wages diverged over time.

Since September 1997, real private sector wages have grown by just 8.3%, a compound average annual growth rate of just 0.28%, despite this era including multiple mining booms and rocketing levels of household debt.

Over the same time in the public sector, real wages have risen by 14.9% or by 79.5% more in relative terms than in the private sector.

This translates to a compound average annual growth rate of 0.5%, which, while not particularly noteworthy, is significantly more impressive than the private sector’s performance.

‘Real Wages’

Since real wages stopped contracting in quarter-on-quarter terms, Treasurer Jim Chalmers’s social media team has been eager to get on Twitter to point out the government’s achievement in growing real wages.

With inflation up by 1.3% for the September quarter and wages up by 0.8%, the narrative has shifted to a focus on real wages in annual terms.

Given that this quarter saw real wages dive by 0.5%, this marks the worst quarter for real wages since the era of the Global Financial Crisis outside of the pandemic and its aftermath.

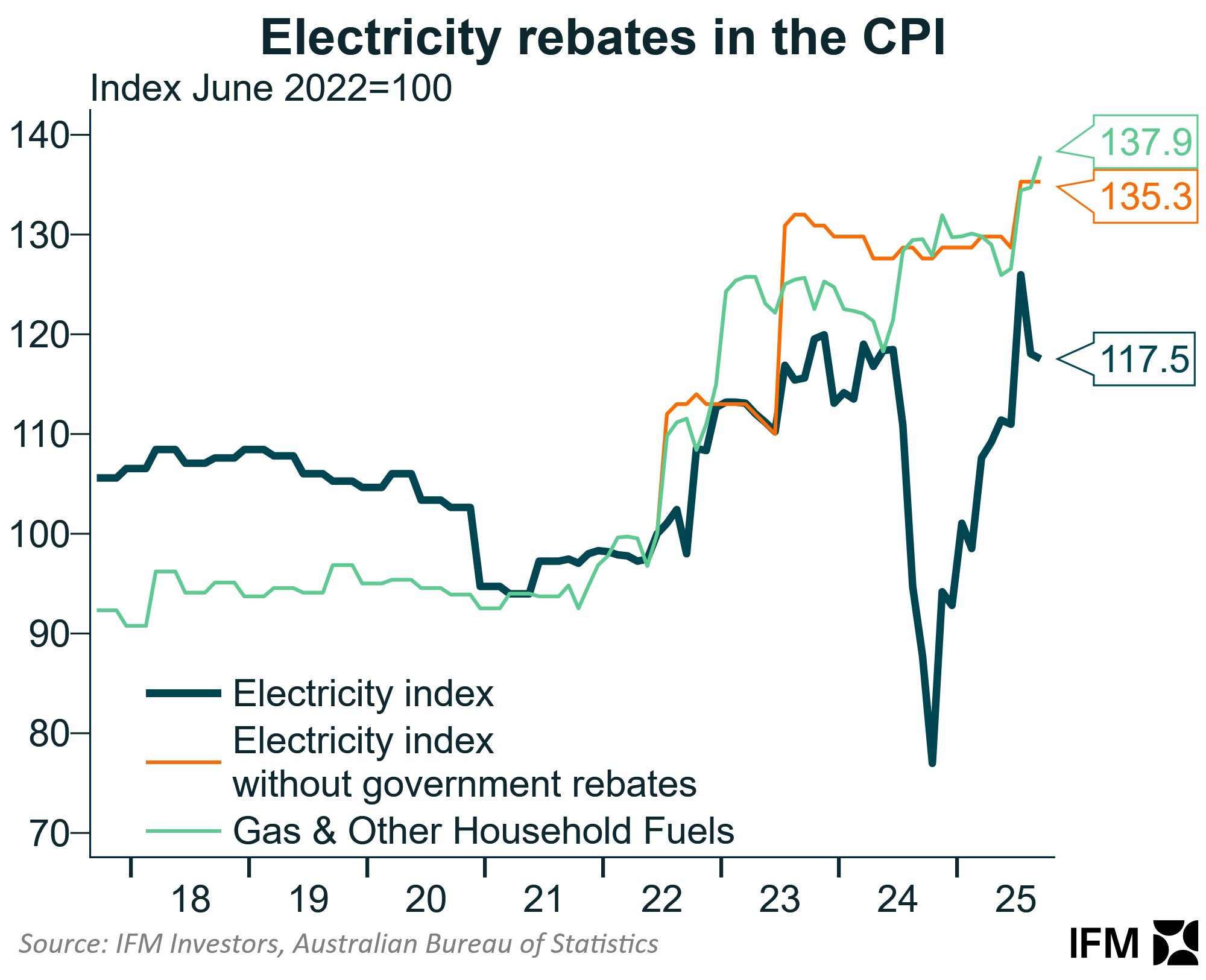

It’s worth noting that the inflationary impulse from the roll-off of electricity subsidies has not yet concluded and there is still quite some way to go until the electricity component normalises with where it should be, as illustrated by the chart below from IFM Investors’ Alex Joiner.

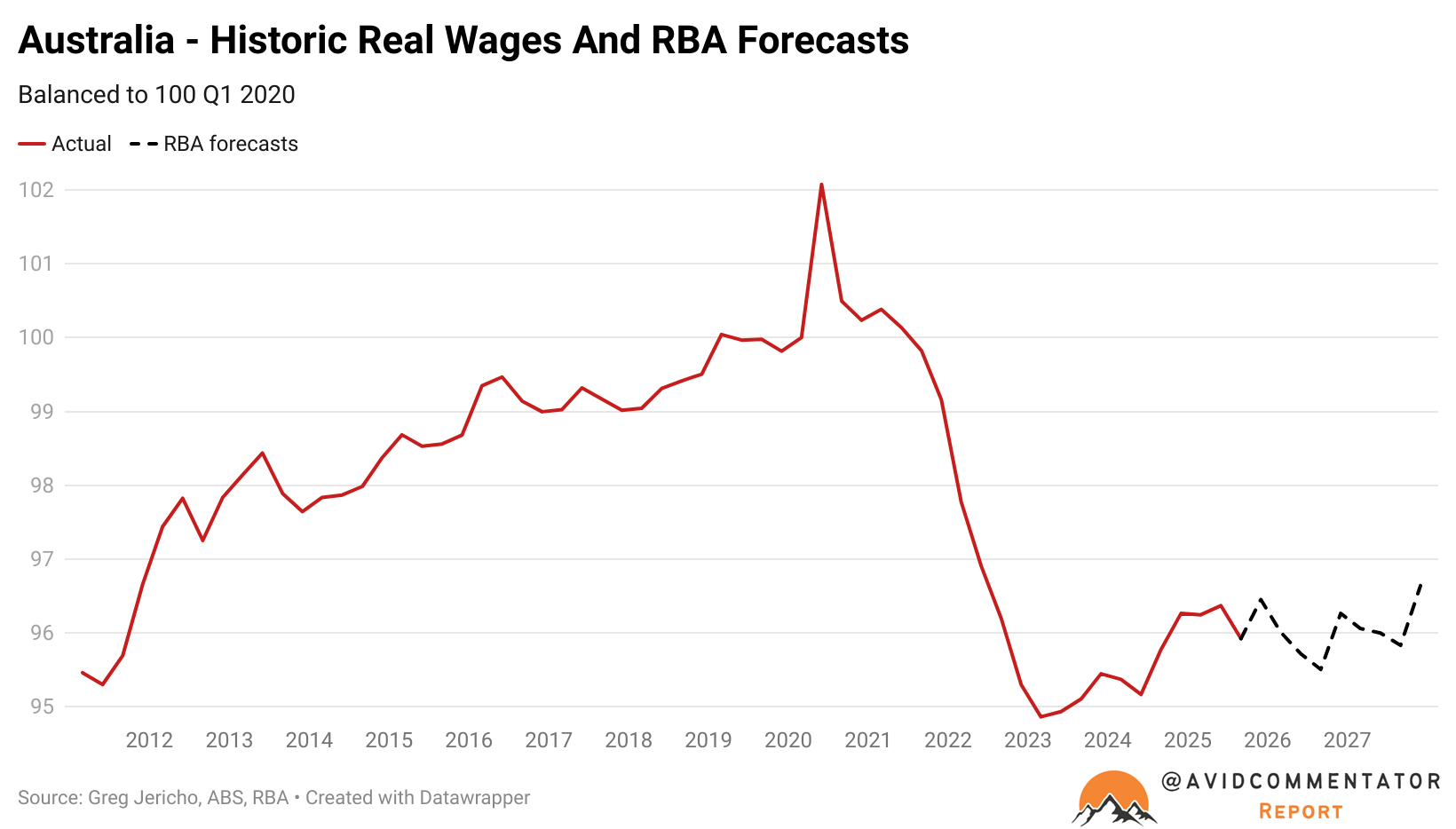

The outlook from the RBA on real wages is also not overly favourable, with part of that stemming from the electricity subsidy roll-off issue.

Based on an analysis of the RBA’s forecasts by Centre for Work Policy Director Greg Jericho, there will be two recessions in real wages, one in 2026 and another shallower one in 2027.

By the conclusion of the RBA’s forward forecast period, wages will sit at roughly where they were in 2012.

Going forward, the divergent outcomes between the public sector and private sector appear set to continue.

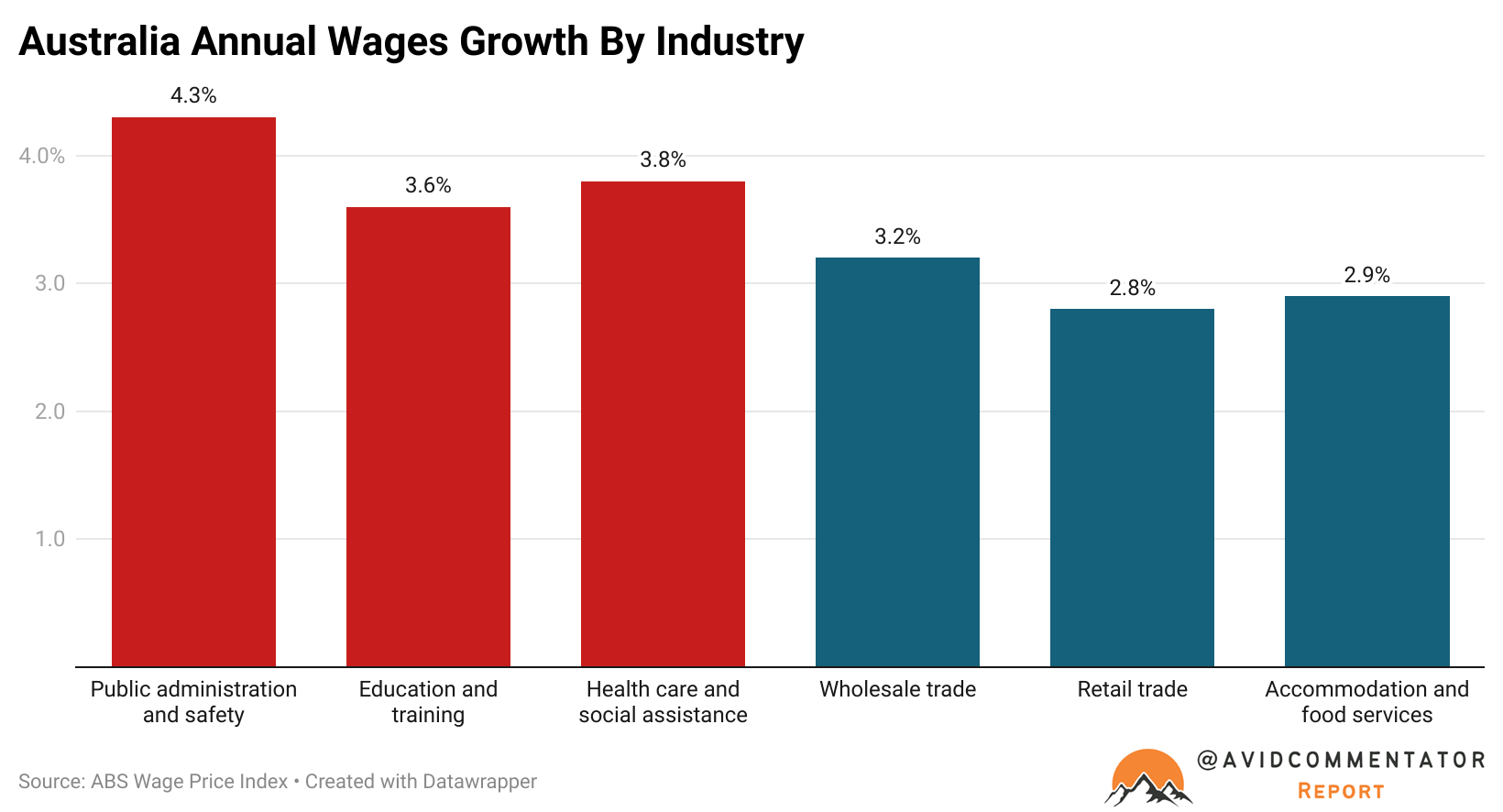

This is illustrated quite nicely by the performance of different industries.

In the non-market sector, which encompasses public administration and safety, education, healthcare, and social assistance, wages are growing more strongly than the national average, in some instances far stronger.

Meanwhile, in terms of wages for the people supplying and serving one’s local shops in the wholesale trade, retail trade, and accommodation and food services sectors, growth is significantly less impressive.

Ultimately, wages are growing most strongly where the demand for labour is strongest, which is generally in those non-market and public sector roles, where hours worked is still growing robustly.

In the market sector of the economy where hours worked are still going backwards compared with Q2 2023, wage growth outcomes are understandably far less impressive.