Recently when the ABS released the latest housing finance data, it came with a headline unwelcome to anyone concerned about housing affordability:

‘Investment loans reach record high’

Now, if we were to wind the clock back 40 years to the mid-1980’s, the assessment of this headline would be entirely different.

At that time, ABS housing finance reports showed that over 60% of new mortgages flowing to investors were for the construction of new homes.

More loans to property investors meant more homes, and despite the high level of relative activity of property investors building new homes, the proportion of occupied housing stock they held as a cohort remained relatively stable.

The current situation is completely different.

According to the latest ABS data, covering the September quarter of 2025, 83% of new loans to investors were to purchase existing properties.

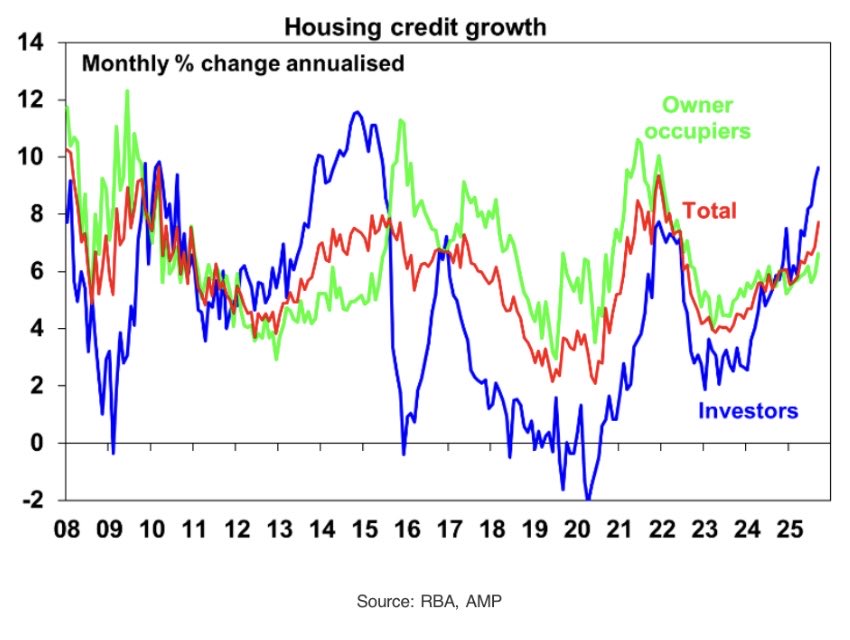

According to an analysis from AMP, the latest RBA Credit Aggregates data revealed that the level of growth in outstanding property investment loans by dollar value hit its highest level in a decade on an annualised basis.

All in all, the current conditions are close to ideal for property investors.

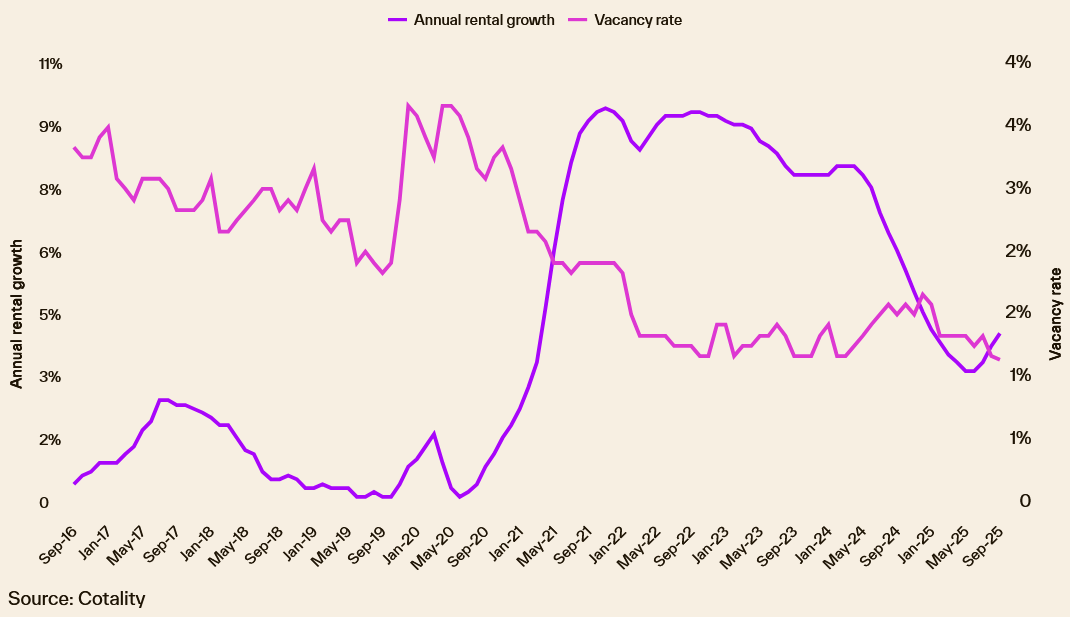

The rental vacancy rate is tracking near record lows, according to Cotality.

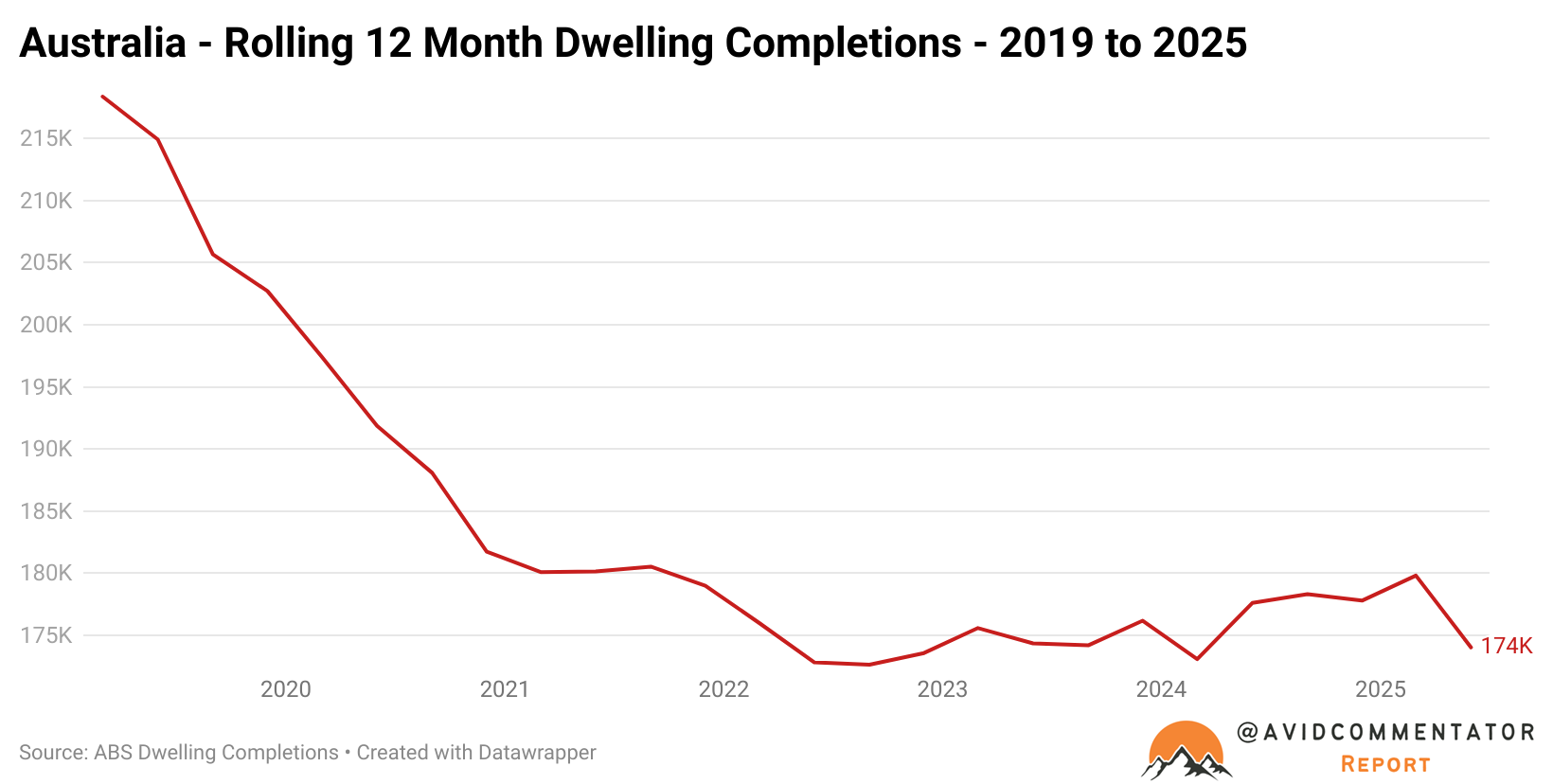

On the supply side, dwelling completions have struggled to break out of the same tight range they have been in for over 3 years, with completions hovering around the 175,000 per year mark, well below what is needed to begin to address the nation’s housing shortage and dramatically below the 240,000 homes per year required under the Albanese government’s 1.2 million new home target.

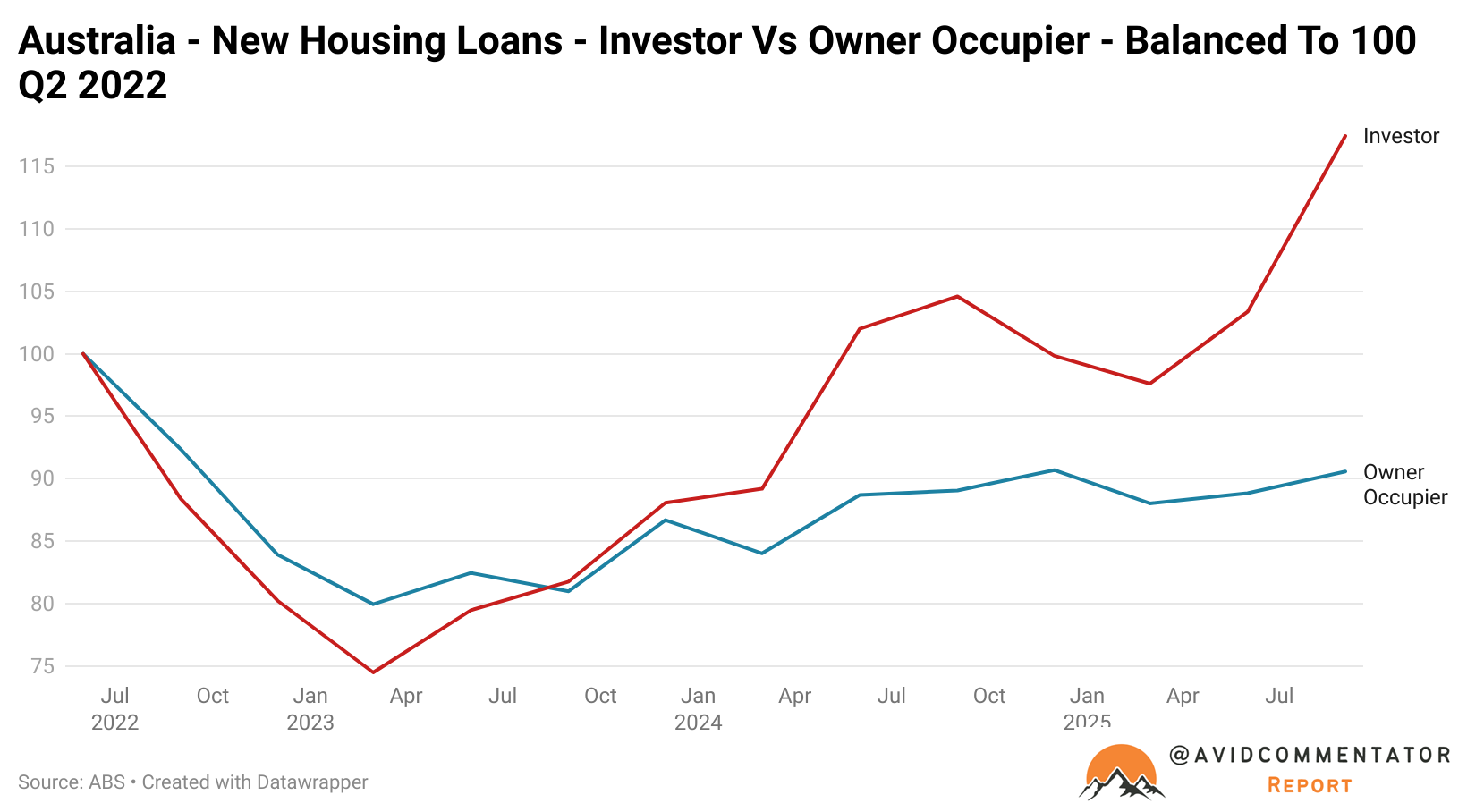

Since the election of the Albanese government in May 2022, new owner-occupier mortgage activity has remained depressed below that first snapshot under the Albanese government’s tenure.

New mortgage activity for property investors, on the other hand, has surged above that base, hitting its highest level on record in both the number of mortgages flowing to investors and the dollar value.

While the government places a great deal of emphasis on the issue of housing, the simple reality is they have delivered conditions consistent with investors continuing to grow their share of the pie at the expense of prospective owner-occupiers.

The Prime Minister attempts to cut a figure as a champion of the people, but in reality what he has delivered is weak real wage growth, stagnating living standards, and increasingly favourable conditions for property investors.

While he may not like the moniker, there is a strong data-driven argument to be made that in 2025, the Prime Minister is a property investor’s best friend.