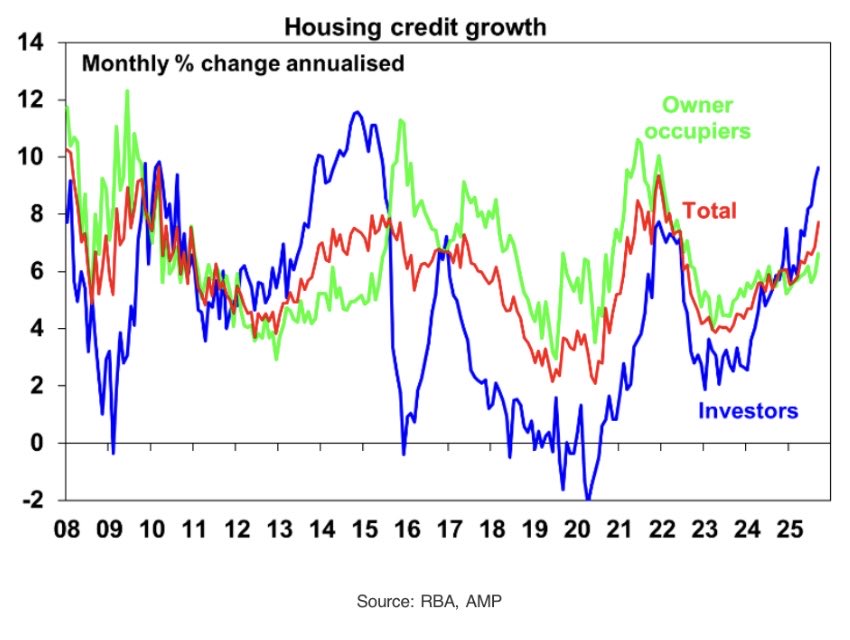

In October, the nation’s housing market saw the strongest growth since June 2023.

It also marked the strongest growth in credit to property investors in a decade on an annualised basis.

October was also notable due to the introduction of the Albanese government’s significantly expanded 5% deposit scheme for first home buyers.

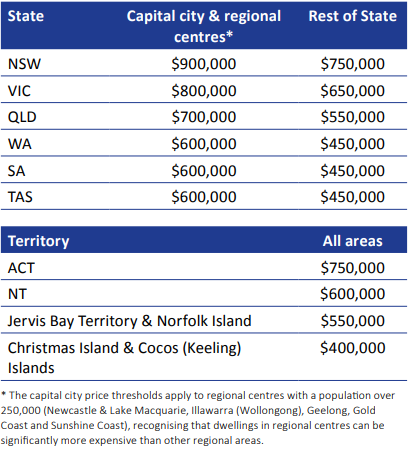

Under the previous iteration of the scheme, individuals with an income of $125,000 per year and joint applicants with a combined income of up to $200,000 per year were eligible to apply.

Price caps varied based on state and whether or not a property was in a regional centre, capital city, or somewhere else in the state.

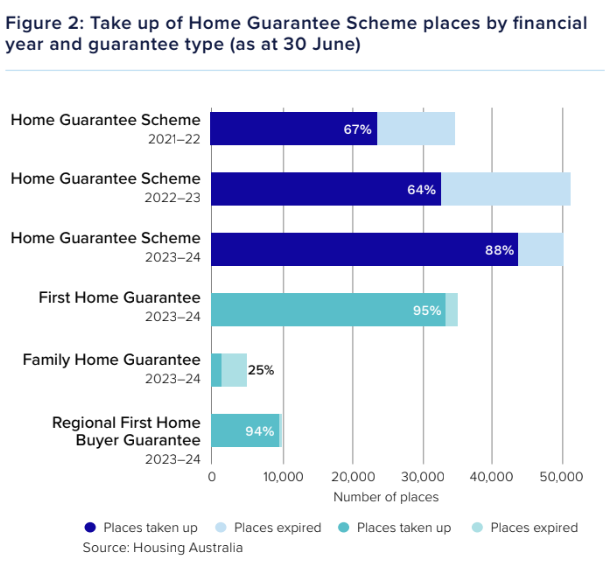

As the chart below from Housing Australia illustrates, the various home guarantee schemes became a larger and larger element of property transactions.

At the previous peak in activity for the scheme relative to overall housing turnover, 40% of first home buyers were relying on the scheme in order to purchase a property.

It’s worth noting that the previous iteration of the scheme was introduced under the Coalition and the legislation to expand it to its 2024 configuration was passed shortly before the Morrison government exited government.

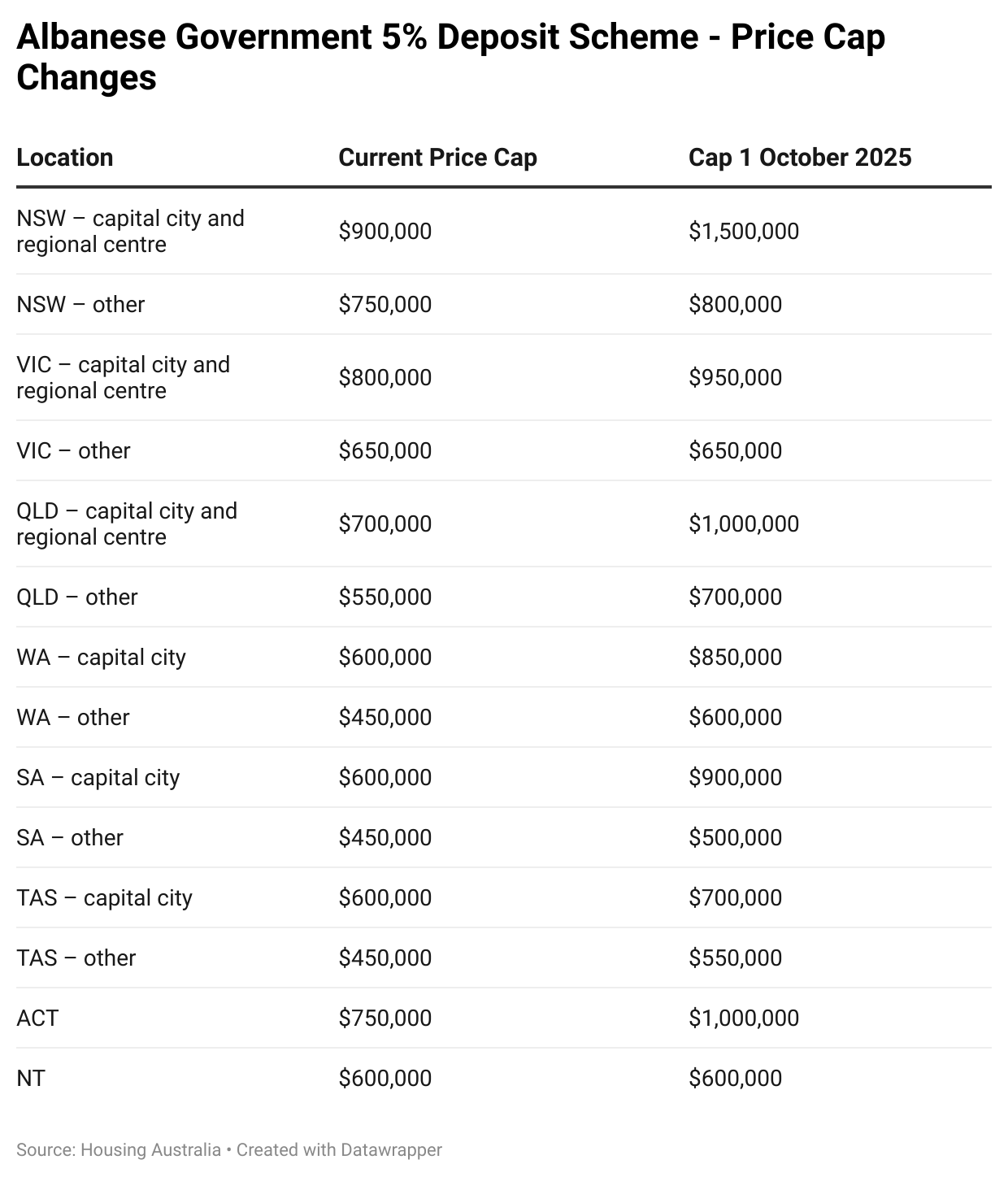

Upon the introduction of the new iteration of the scheme by the Albanese government, income caps were abolished and price caps were raised dramatically.

For example, on September 30th, the cap for a prospective first home buyer purchasing a home in Sydney was $900,000; it is now $1.5 million.

The increase in price caps continues more or less along these lines, as illustrated by the chart below from the federal government agency, Housing Australia.

The Result

It didn’t take long for demand to surge as a result of the Albanese government’s expanded scheme.

According to figures from the Albanese government, 1 in 10 homes purchased in October were conducted using the Albanese government’s 5% deposit scheme.

The number of home purchases enabled with the Home Guarantee scheme in October was up by 48.1% compared with the performance of its previous version in October last year.

The government also noted that roughly half of the transactions made possible by the 5% deposit scheme in October would not have been possible under the previous version of the scheme.

These two statements are rather obvious illustrations that the scheme is having a significant impact on the housing market.

That roughly half of those transactions required the new scheme raises questions about the remaining pool of first home buyers, and whether they could have bought homes if the Albanese government had not dramatically expanded eligibility.

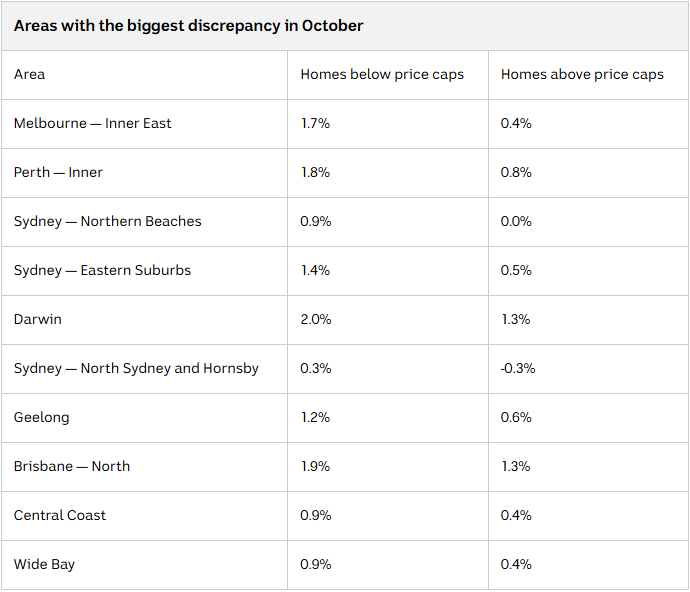

The early evidence from Cotality suggests that the scheme may be having an outsized impact on certain elements of the market.

In a recent data release, Cotality measured the performance of home prices in different price brackets of the market—those where buyers are able to take advantage of the 5% scheme and those where prices exceed the current caps.

The largest gaps in market performance often appeared in segments where prices were below caps and above price caps, particularly in some of the most affluent areas where meeting the previous price caps would have been challenging.

However, the new higher price caps now make a significantly larger portion of the market eligible for government backing.

This is also arguably emblematic of the fact that income caps have been removed, allowing higher earners with small deposits the ability to buy with a small deposit and government support.

Chart: ABC News

Ultimately, property experts, academics, and political figures will continue to debate the impact of the first year of the expanded 5% deposit scheme long after it has become a distant memory for most Australians.

However, it is evident that the scheme has significantly increased demand in a market where property investors were thriving.