In the world of economics, a recession is often defined as two consecutive quarters of declining economic growth in inflation-adjusted terms.

But in the realm of housing supply, the role of inflation is played by demand growth.

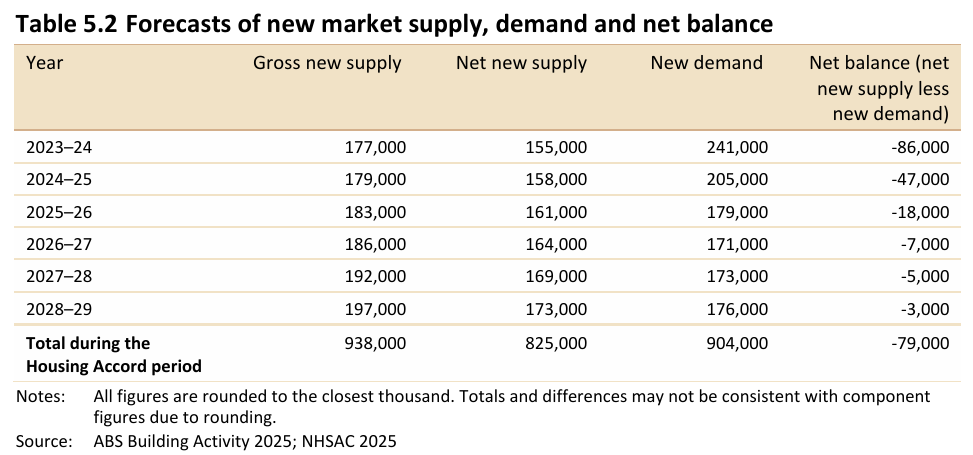

By this metric, Australia’s housing supply growth has been in a recession in net terms for over four years.

According to figures from the federal government’s National Housing Supply and Affordability Council, the shortage of homes since July 1st 2023, comes to over 137,500 homes.

Unfortunately, their dwelling completion estimates were slightly high, so the shortage is actually somewhat larger than that again.

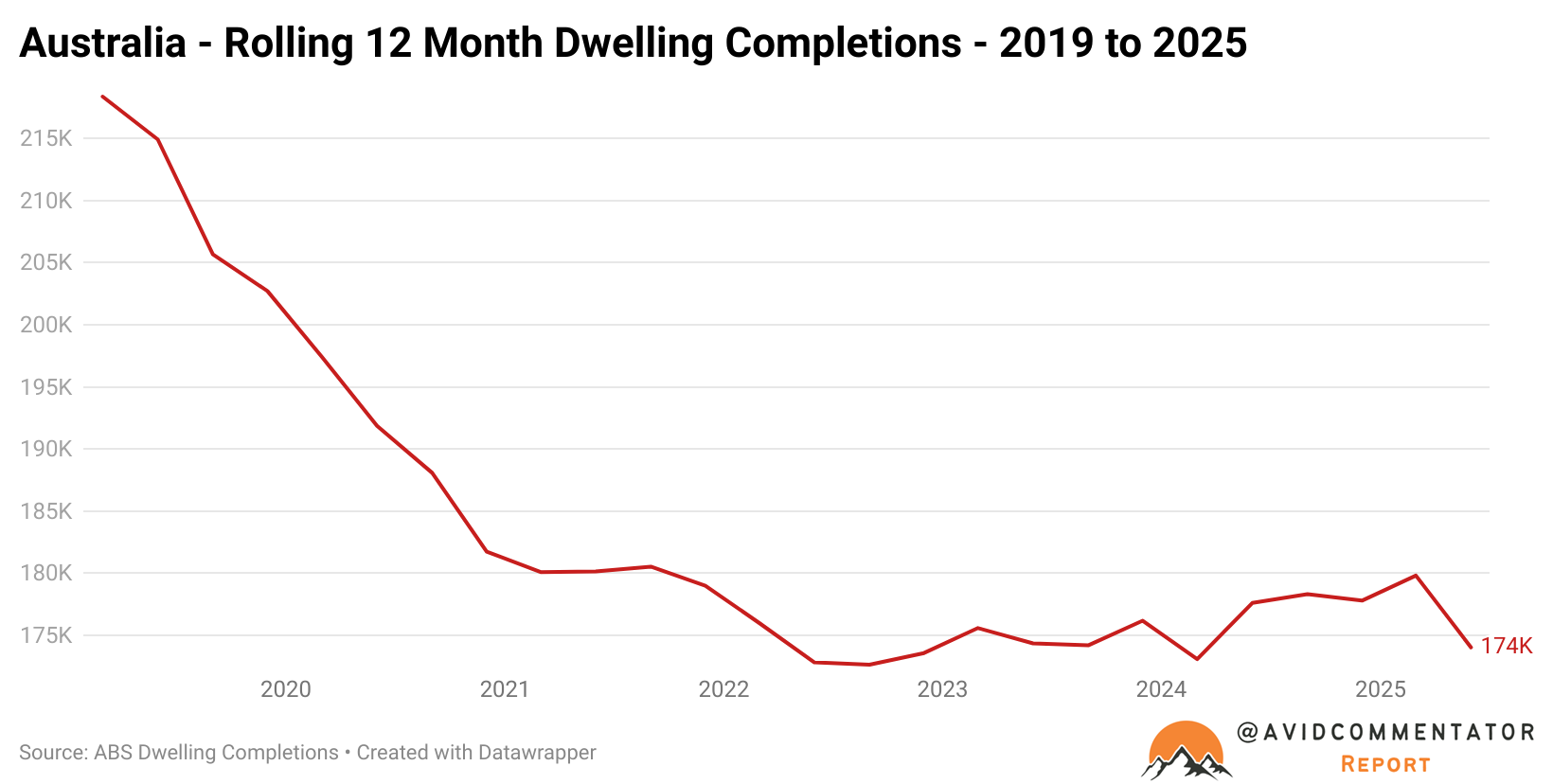

Despite the Albanese government putting housing, in particular public housing, as the major focus of its first term and beyond, what it has delivered is effectively a level of overall dwelling completions that has gone more or less nowhere since its election three and a half years ago.

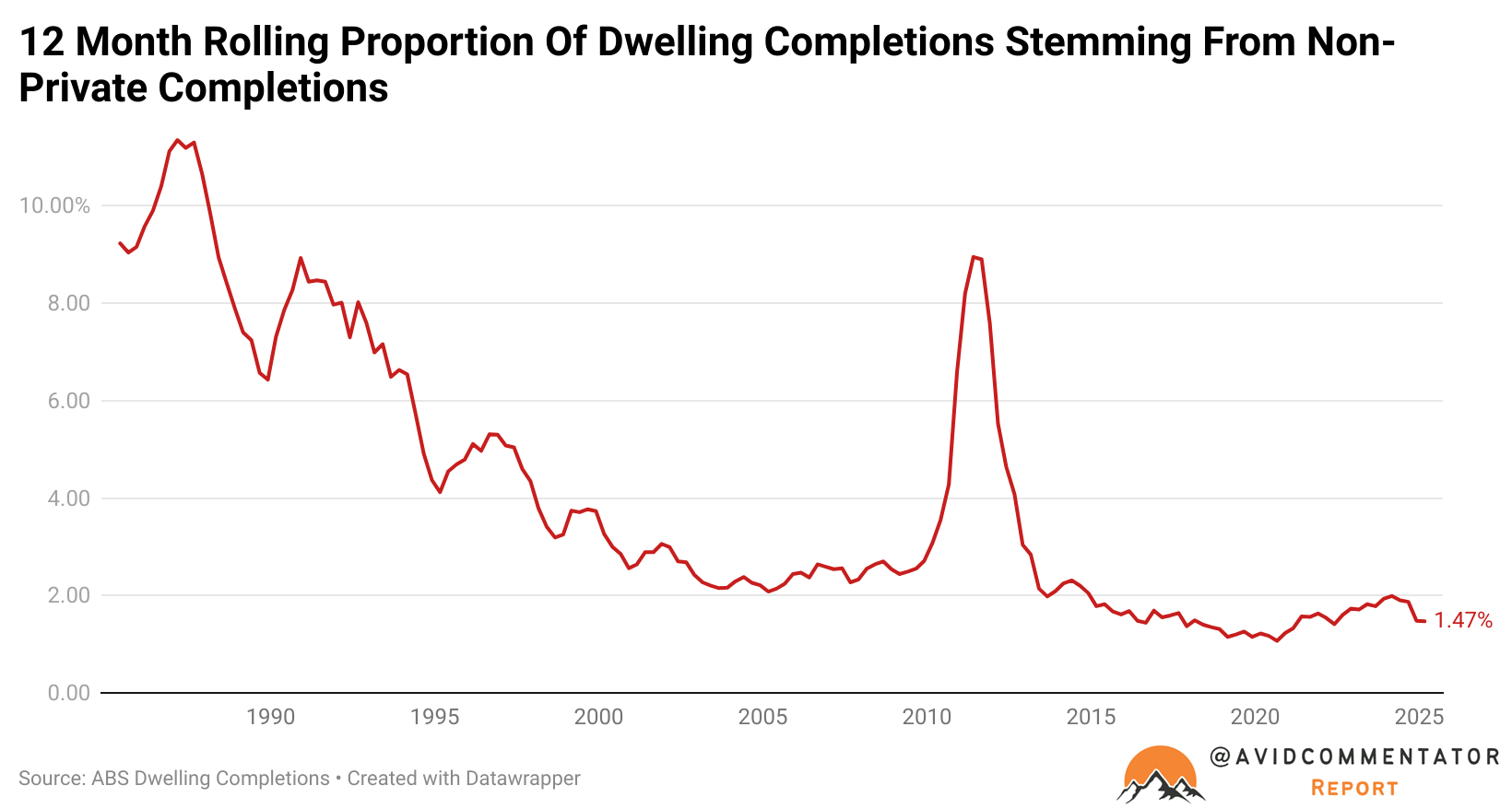

Meanwhile, despite the Albanese government pursuing its Housing Australia Future Fund and Social Housing Accelerator, the proportion of homes completed for the non-private sector is indicating that the share of dwelling stock stemming from public and social housing is continuing to dwindle.

While this outcome is not surprising for observers of housing policy and the construction sector, it is a stark departure from the performance of the previous Rudd/Gillard Labor government, which provided a major stimulus to public and social housing construction.

As the chart below indicates, the level of completions for the non-private sector surged dramatically during that era, growing the proportion of housing stock held by public and social housing for the first time this century.

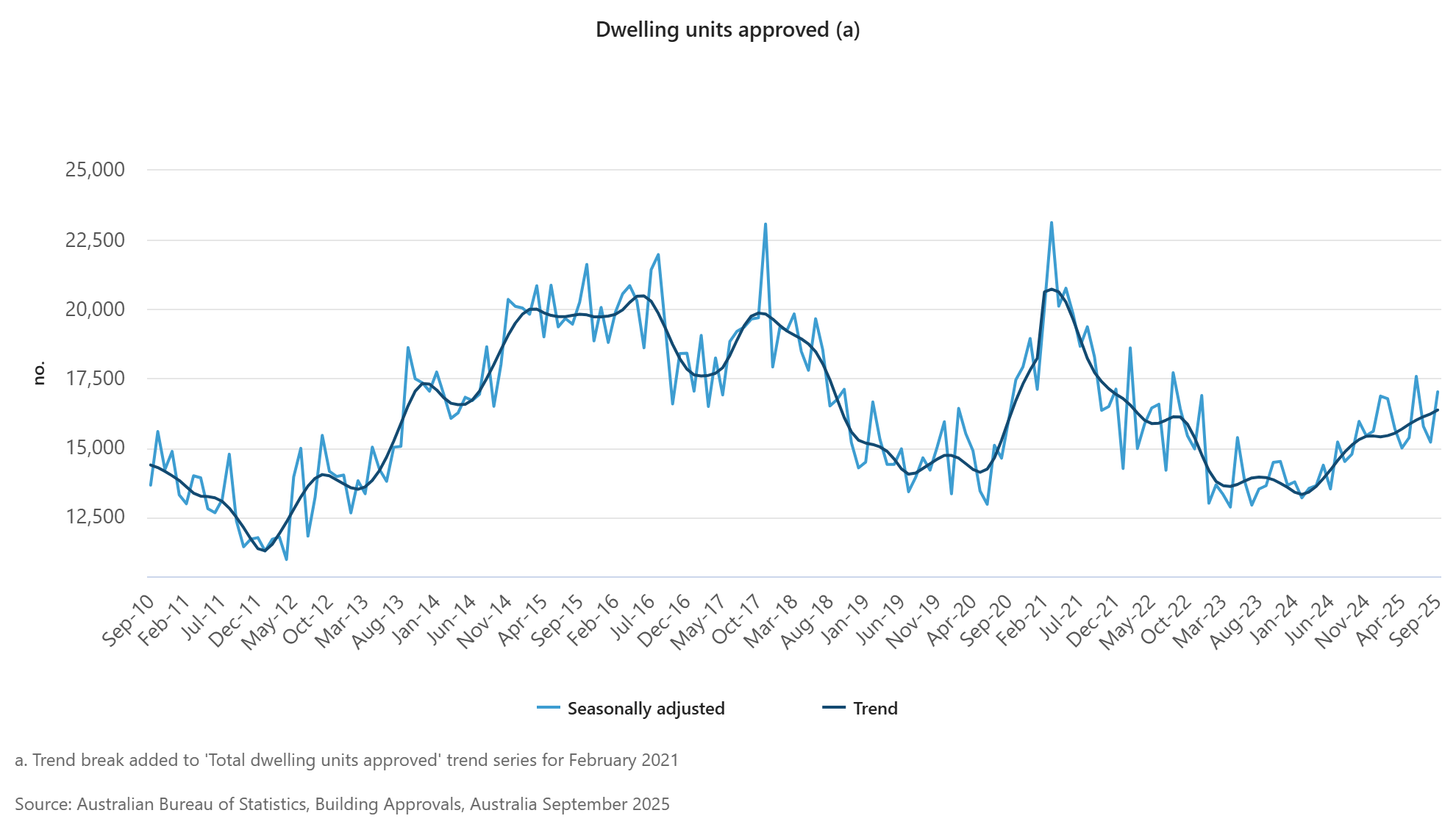

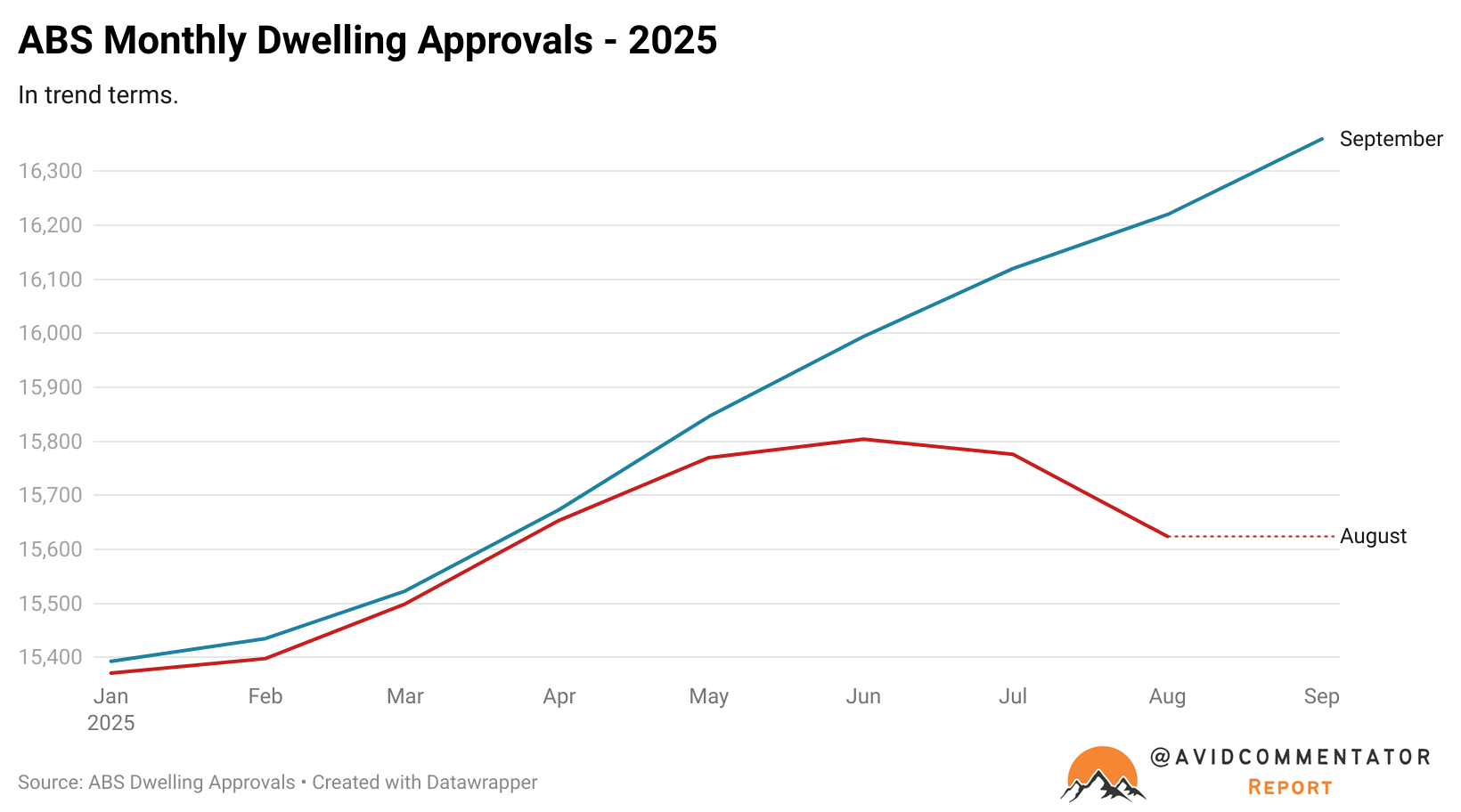

Meanwhile, the latest news on building approvals from the ABS was more promising.

For September, the number of dwellings approved rose 12%, following a 26% rise in non-detached house approvals for the month.

This is the latest round of the ongoing volatility in non-detached house approvals.

In terms of private sector houses, that figure was up 4% for the month.

Revisions to the previous data in trend terms also reveal a significant positive shift in the trajectory of approvals.

The Takeaway

Despite making the issue of housing a major focus of the Albanese government, what they have delivered is:

- Still anaemic growth in the number of dwelling completions

- The highest level of housing price growth in almost four years

- A decade high in the growth of annualised credit growth flows to property investors

- A rental crisis that persists years after it ended in most other nations

- Building approvals that are still weak despite successive rate cuts

While the government can sometimes seem like a ship adrift in the changing tides of residential construction cycles, in 2025, this situation is increasingly a result of policy choices.

It is a well-known fact that the construction sector is facing significant challenges and is shifting its focus from the laborers who physically construct homes to a more white-collar workforce, resulting in a significant increase in costs and a decrease in output per worker.

Yet this issue and others are largely left undisturbed, despite the government’s very public push for improving productivity.

Ultimately, improving productivity and increasing housing supply growth have costs that policymakers have so far been unwilling to pay.