With the release of the latest national accounts data showing that household consumption had grown by 0.9% in inflation-adjusted terms and the ABS Household Spending Indicator showing spending up by 0.5% MoM in July and up 5.1% YoY, some are questioning whether rate cuts are working.

Before we get into the numbers detailing how rate cuts have impacted household cash flows, both positively and negatively, let’s look at how the economy is performing from a broader overview.

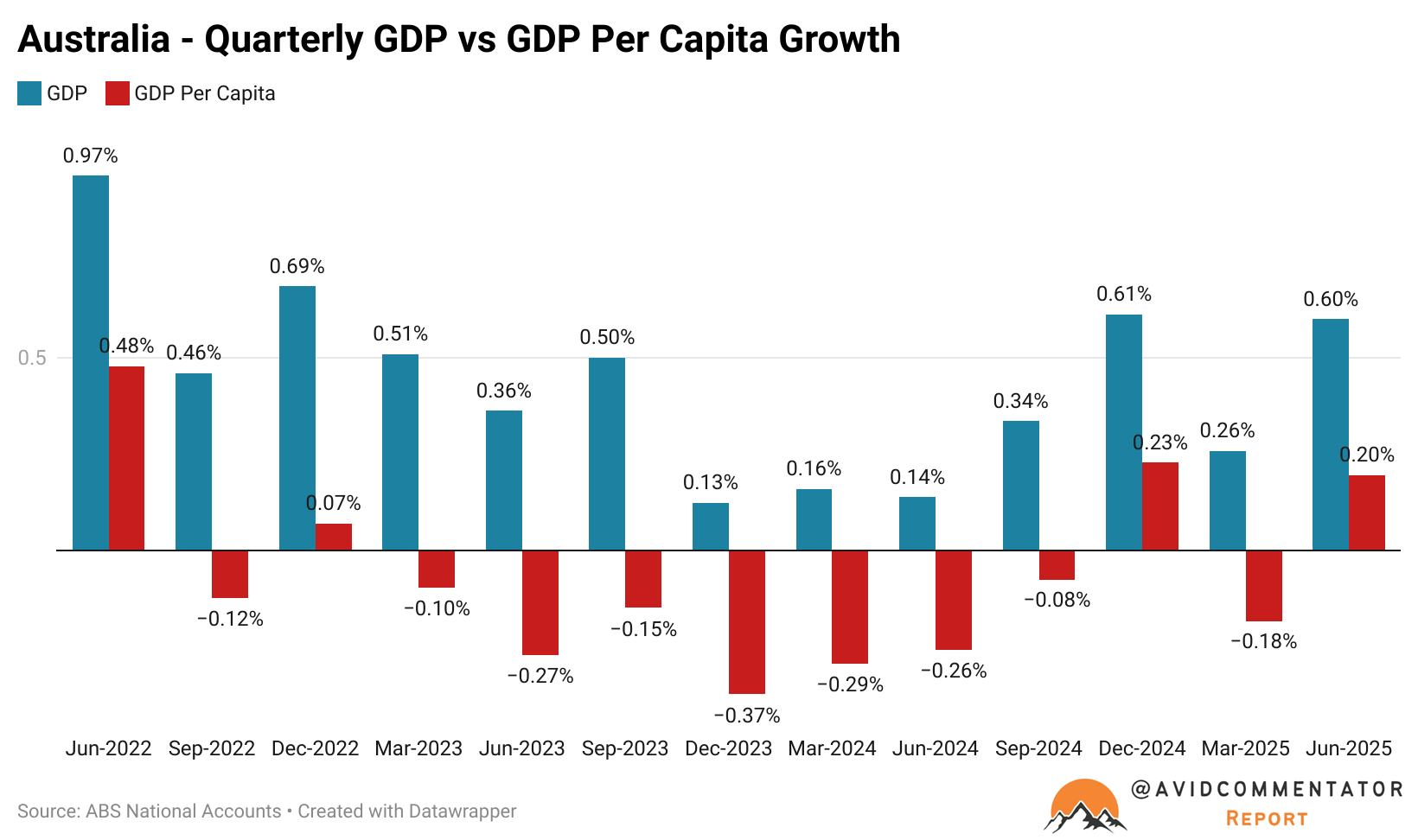

The last quarter produced overall quarterly growth of 0.6%, with per capita growth up by 0.2%.

This has prompted both optimism and caution from economists, with the relatively robust result for household spending growth in headline terms providing hope for a private sector-led boost to the economy.

On the other hand, others have counselled caution, noting that much of the rise came from holiday travel and recreation, which the ABS notes may have been unseasonably boosted by the proximity of the Easter and ANZAC public holidays this year.

The ABS also noted that household spending on electricity was a significant driver of the positive household spending result.

This is due to the impact of government electricity subsidies feeding into the data:

“Reductions in electricity rebates are treated as a shift in expenditure from government to households in the national accounts.”

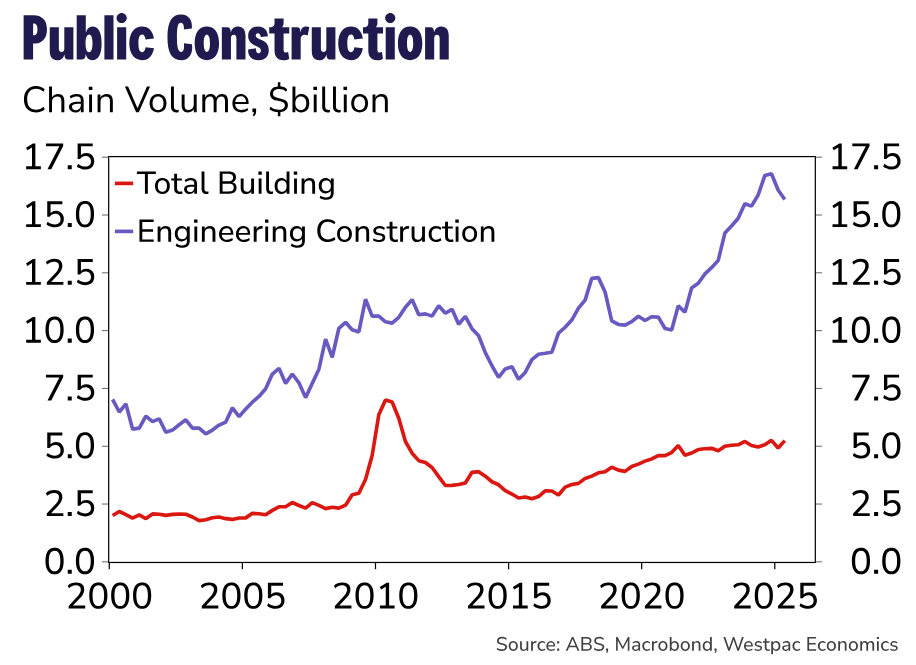

Amidst the pullback in public construction, which Westpac recently noted, the jury remains out on whether or not the handoff from a heavily government-supported economy to one more driven by the private sector will occur without significant economic downside.

A driver expected to play a significant role in that shift is rate cuts, but what does the actual impact look like in overall aggregate cash flow terms?

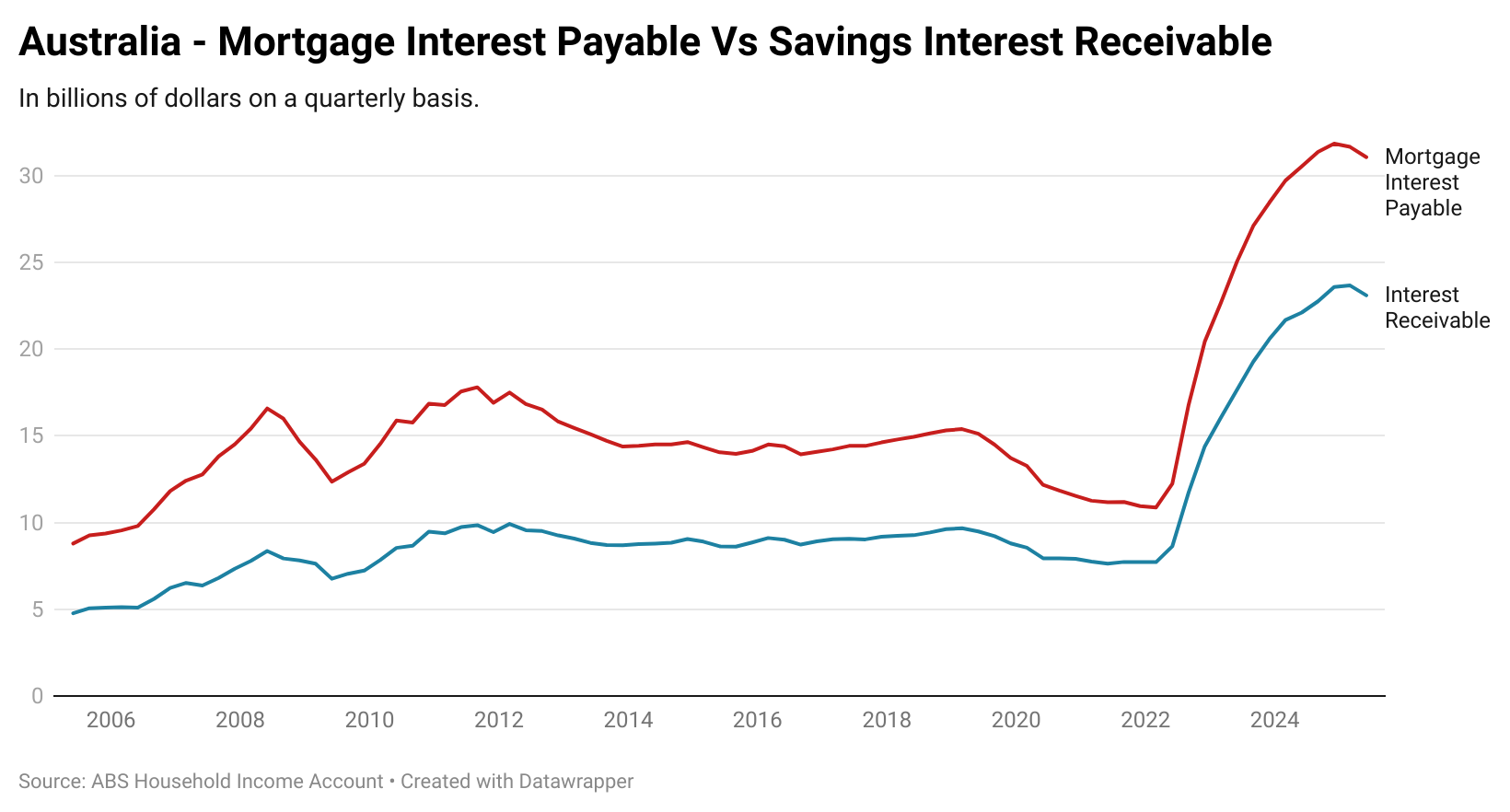

According to figures from the Household Income Account, which is contained within the quarterly National Accounts, households spent $31.07 billion on mortgage interest repayments in the June quarter.

This is down from a peak of $31.84 billion in the December quarter of last year.

While the outstanding total of mortgage debt has risen over the last two quarters, at an aggregate level, this represents a reduction in total mortgage servicing costs of $774 million per quarter.

But there is another side to this particular coin.

Over the years since the pandemic first hit our shores, households have collectively amassed a substantial savings warchest.

As rates have risen, this has resulted in a massive surge in flows of interest payments to households.

In the final quarter before rates began to rise in May 2022, total flows of interest payments to households came to $7.72 billion per quarter.

At the peak of flows in the March quarter of this year, this figure had risen to $23.67 billion per quarter.

As rates continue to decline, the windfall for the nation’s savers is diminishing, creating an economic headwind.

Overall, from their respective peaks, the flow of interest payments to households has declined by $567 million per quarter. In comparison, interest repayments by households on their mortgages have fallen by $774 million per quarter.

Even if we assume an average 30% tax on the interest payments to savers, we are talking about a net impact of approximately $375 million per quarter as a windfall for households.

However, this assumes that mortgage-holding households are pocketing the difference, not simply keeping their payments the same and paying down their loans faster.

While this is still technically a windfall for households pursuing this strategy, in the short term, it’s not a functional boost to household cash flows.

Based on the conditions above, the net physical boost from rate cuts thus far to household cash flows is less than 0.06% of GDP.

Ultimately, in the Australia of 2025, the means by which rate cuts may deliver a stronger economy has little to do with the extra cash households receive in net terms and everything to do with the impact on consumer sentiment and the wealth effect driven by higher asset prices.