Advertisement

Advertisement

For some, each rate cut is treated like nectar from the Greek Gods atop Mount Olympus.

Advertisement

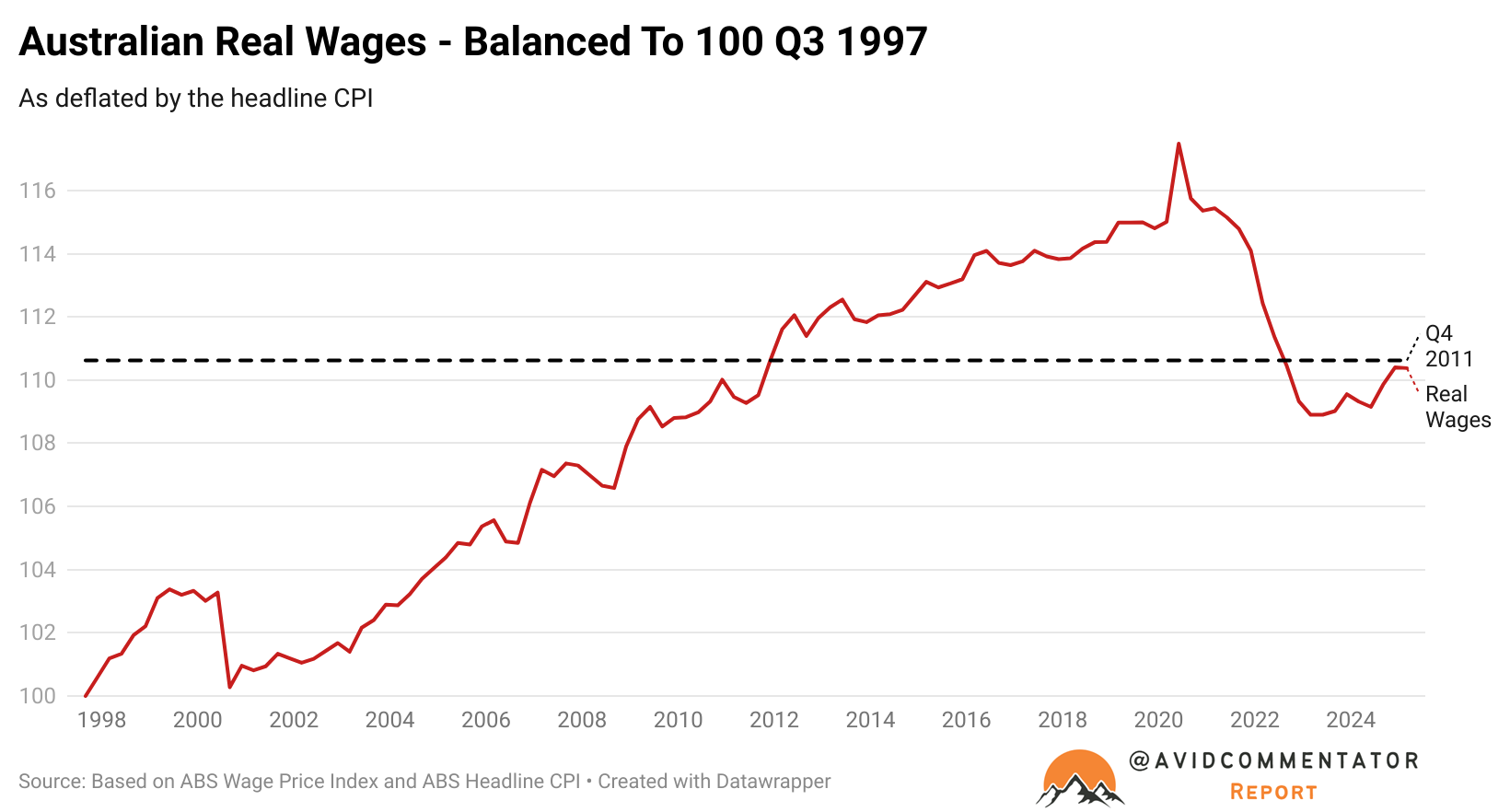

After all, over the last decade the pathway to greater levels of household disposable income for mortgage holders has often come from the RBA cutting rates, not from growth in real wages as it generally did historically.

With rates cut just yesterday and the expectation of more to come, let’s explore how they could impact the economy.

Advertisement

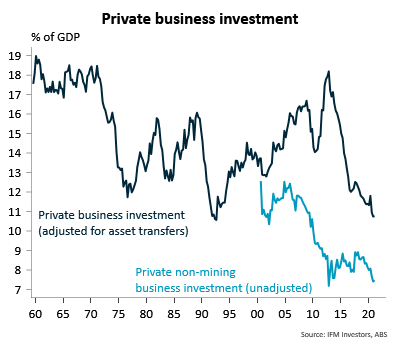

On paper, rate cuts are meant to stimulate the economy and inflation through increased levels of business investment.

But that isn’t really how things have worked in Australia since the conclusion of the mining boom, instead business investment remains depressed near recession levels vs GDP.

Which leaves two main avenues for impacting the economy, the direct impact of mortgage holding households having more cash to theoretically spend and the wealth effect.

Given the rise in household savings seen since the pandemic, there will be an even greater than normal blow to household incomes through lower rates, which partially negates the positive impact of flows to households.

On the other hand, early data from CBA indicates households are generally using the cashflow boost from rate cuts to rebuild buffers and savings, not use their windfall to increase spending to the degree one might expect.

“New data from the Commonwealth Bank shows that just 14 per cent of eligible home loan customers reduced their home loan direct debit repayments following the February 2025 rate cut.”

Advertisement

This may end up leaving us with the wealth effect as the main driver of lower rate driven growth.

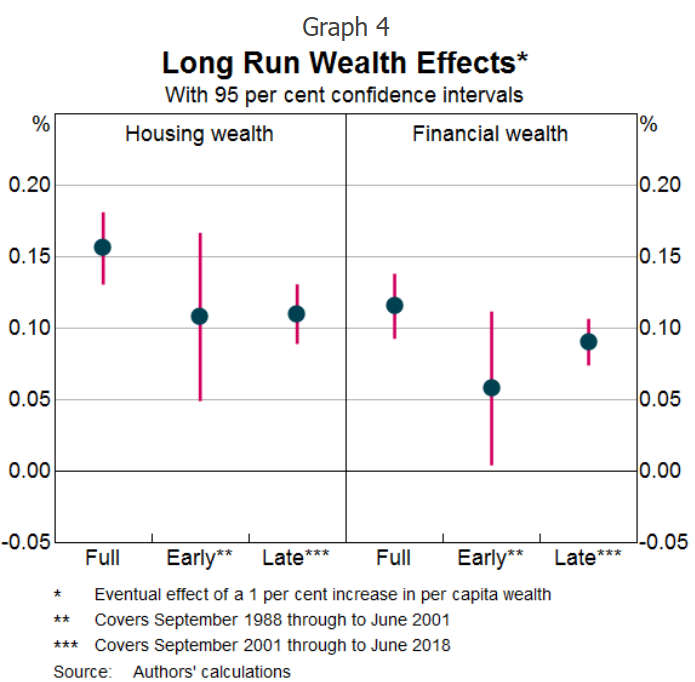

A 2019 paper from the RBA concluded that:

Advertisement

“a one per cent increase in the value of housing wealth will lead to a 0.16 per cent increase in the long-run level of consumption, while a one per cent increase in stock market wealth will raise consumption by 0.12 per cent”

Except the share market is at all time highs, the property market at a national level is growing strongly and at all time highs. So the wealth effect is arguably already in full swing.

While it may find another higher gear, the potential impact is arguably significantly smaller than most previous rate cut cycles.

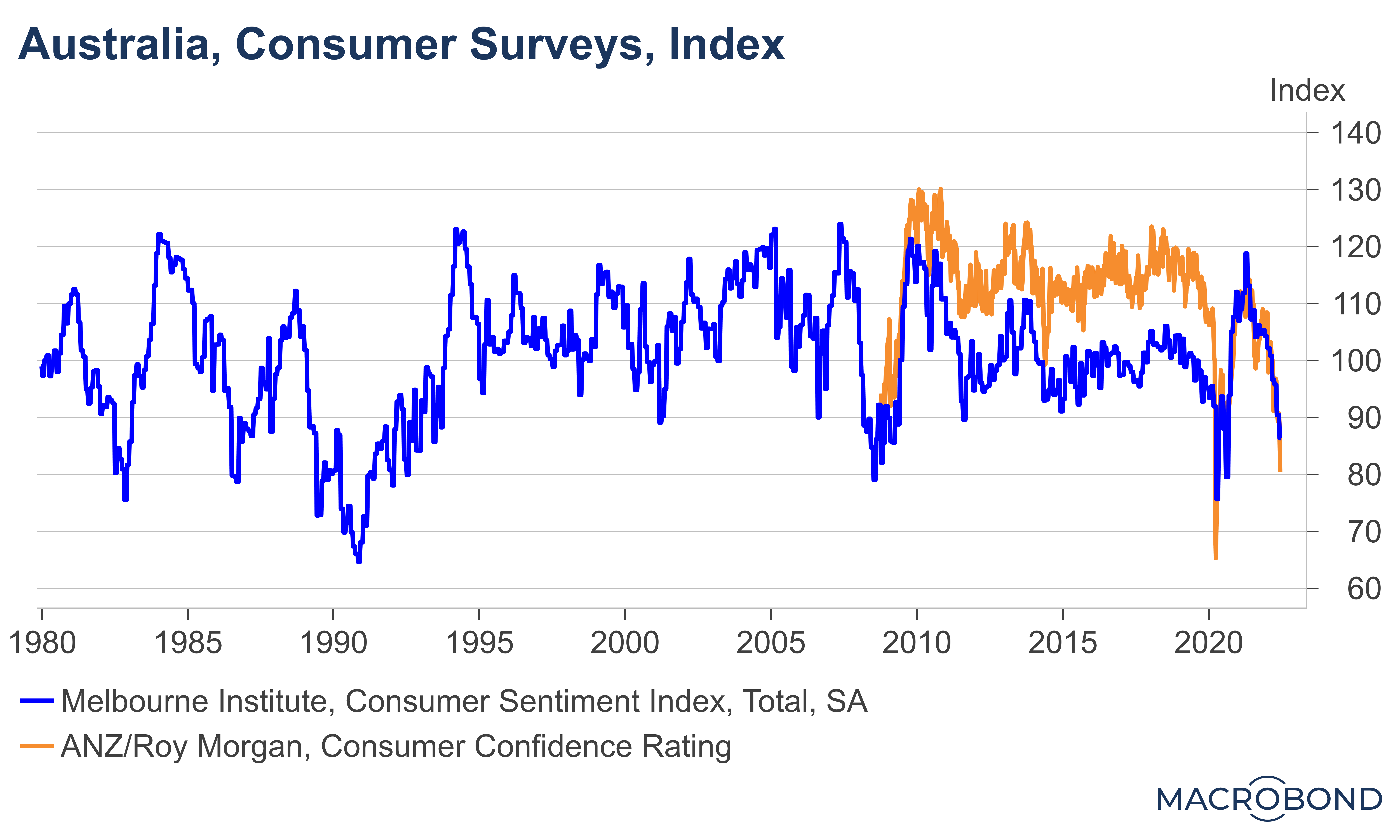

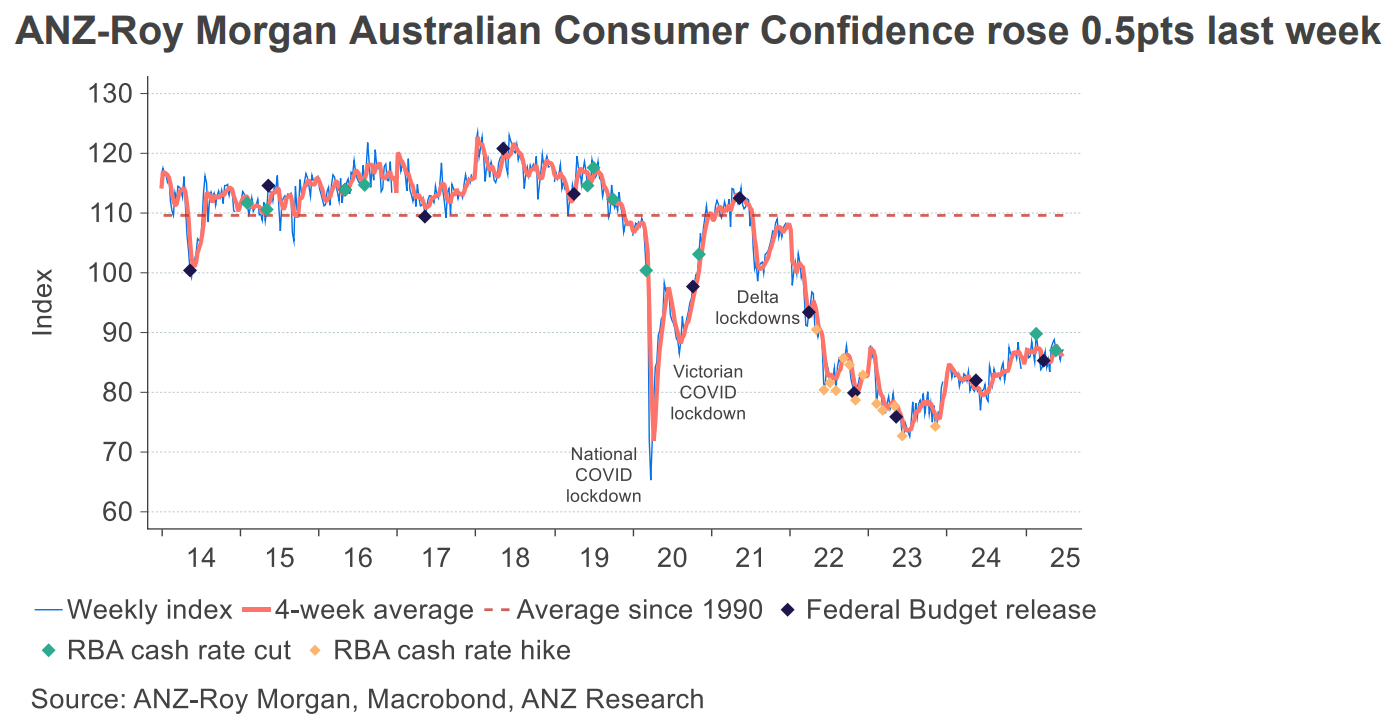

In time lower rates should in theory prompt significantly higher rates of consumer confidence, which remain near GFC and 1983 recession lows.

But whether it will be the case this time remains to be seen, as households attempt to claw their way out of a deeply challenging position.

Advertisement

In short, the forces that normally drive rate cuts to stimulate the economy are either already in effect or potentially somewhat blunted by changed conditions.

Which may leave the fate of the impact of lower rates in the hands of somewhat more intangible psychological effects such as consumer’s sentiment.

And it augurs lower rates than most expect.

Advertisement

About the author

Tarric is an Australian freelance journalist and independent analyst who covers economics, finance, and geopolitics. Tarric is the author of the Avid Commentator Report. His works have appeared in The Washington DC Examiner, The Spectator, The Sydney Morning Herald, News.com.au, among other places.