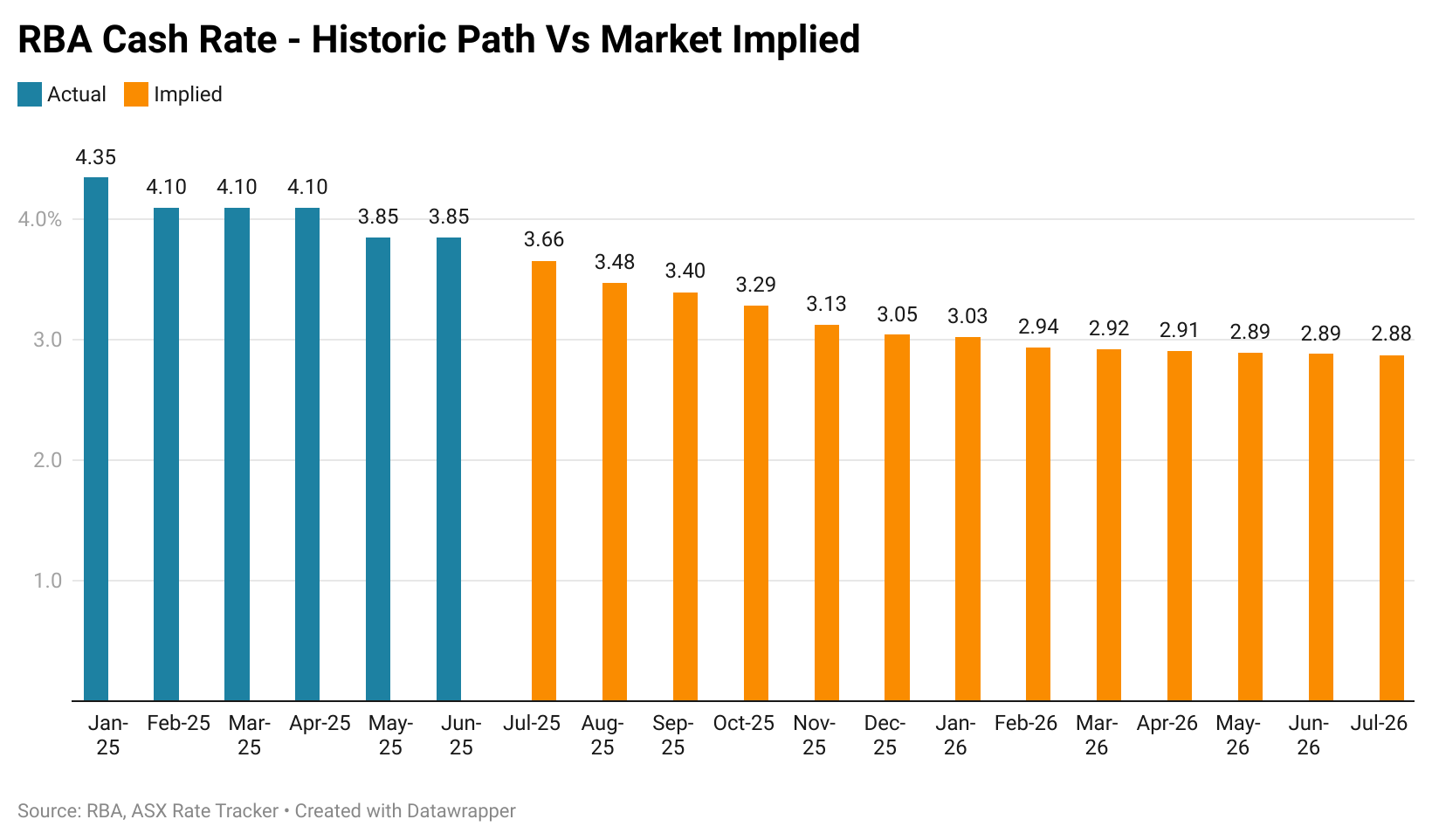

As the global economy continues to decelerate amidst a backdrop of escalating trade conflicts and war in the Middle East, interest rate futures markets are increasingly pricing in additional rate cuts from the RBA.

As of the latest close of the futures market, roughly 3.9 rate cuts are priced in by the market over the next 12 months.

If a further four rate cuts were to be realised, it would put the total cut to interest rates to 1.5 percentage points before a very gradual rise in expected rates coming in Q4 2026.

Which raises an interesting question: is this magnitude of rate cuts normal for an RBA cutting cycle? And if not, what is normal?

History of Mortgage Rate Cuts

The history of cuts to Australian mortgage rates can be divided into two distinctly separate eras.

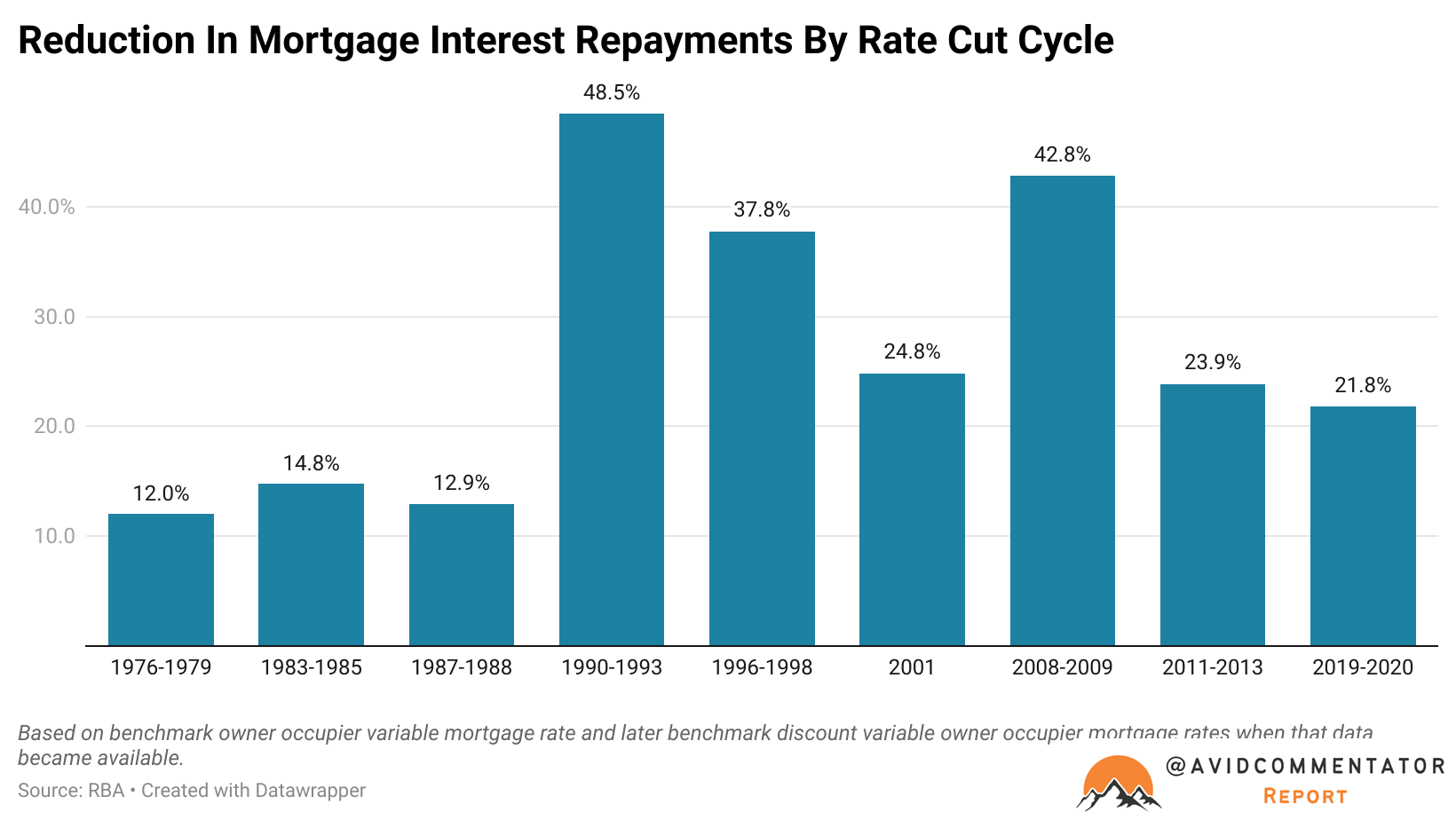

Between 1959 and 1989, the largest relative reduction in mortgage rates was 14.8% during the 1983-1985 rate cut cycle. The smallest was in 1975, which reduced the relative mortgage rate by just 2.3%. Half of the rate cut cycles during this period were of 0.5 percentage points or less.

Since then, the relative decreases in mortgage rates have gotten dramatically larger. The largest in Australian history occurred between 1990 and 1993, during which mortgage rates were cut by 48.5% in relative terms.

The next closest challenger comes from the Global Financial Crisis era rate cuts of 2008-2009, during which mortgage repayments were cut by 42.8%.

It’s here that we need to make a bit of a distinction. We could look at every rate cut made since 1959, but that would be skewed by all manner of small rate cuts. Instead, we will be focusing on rate cuts, which saw actual mortgage rates as recorded by the RBA falling by at least 1.0 percentage points.

On this metric, the average relative reduction in mortgage rates since records began in 1959 is 26.6%, with a pre-1990 average of 13.2% and a post-1990 average of 33.3%.

Part of the issue with comparisons in the last 30 years is that the sample size of rate cuts that occurred under “normal” conditions is relatively limited. The rate cut cycles of the 1990s recession and GFC era are significantly larger than the others that have occurred in the post-1990 era.

If we remove those from the equation due to them occurring as a result of either a major economic downturn or the GFC, the average rate cut cycle changes dramatically. The average reduction in mortgage rates falls from 33.3% to 27.0%.

If we superimpose that on the peak rate of payable variable owner-occupier rates based on data from the RBA, it comes to a fall in mortgage rates of 1.75%.

With the market pricing in total mortgage rate cuts of 1.485%, this comes in right in the ballpark for a post-1990 rate cut cycle not playing out in some sort of crisis or recession.

The Impact On Households

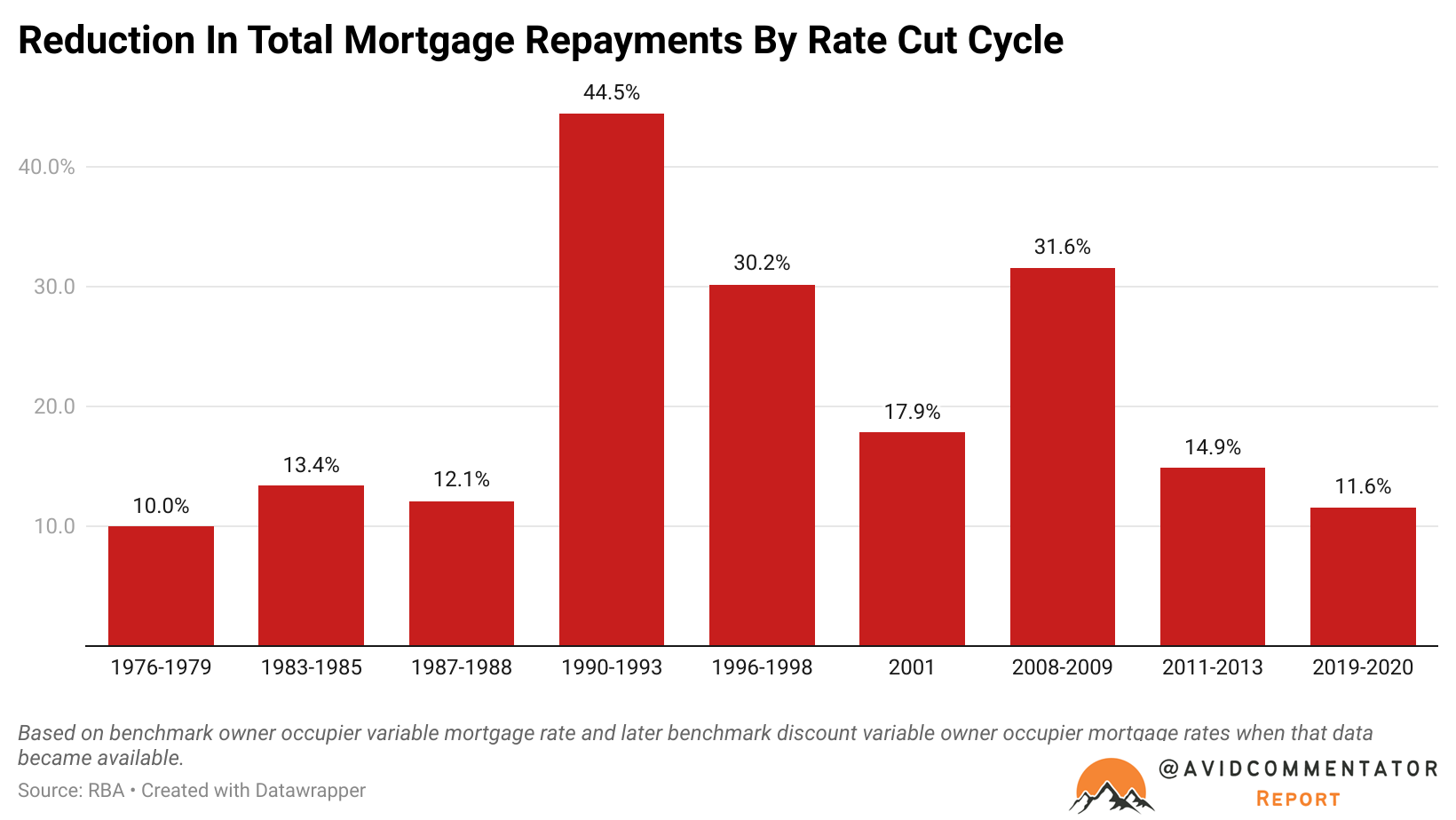

It’s worth noting that not all rate cut cycles are created equal, even if the reduction in mortgage rates is proportionally exactly the same. This is because, depending on the snapshot in question, principal repayments take up a larger or smaller proportion of overall mortgage repayments, leading to potentially significant different outcomes.

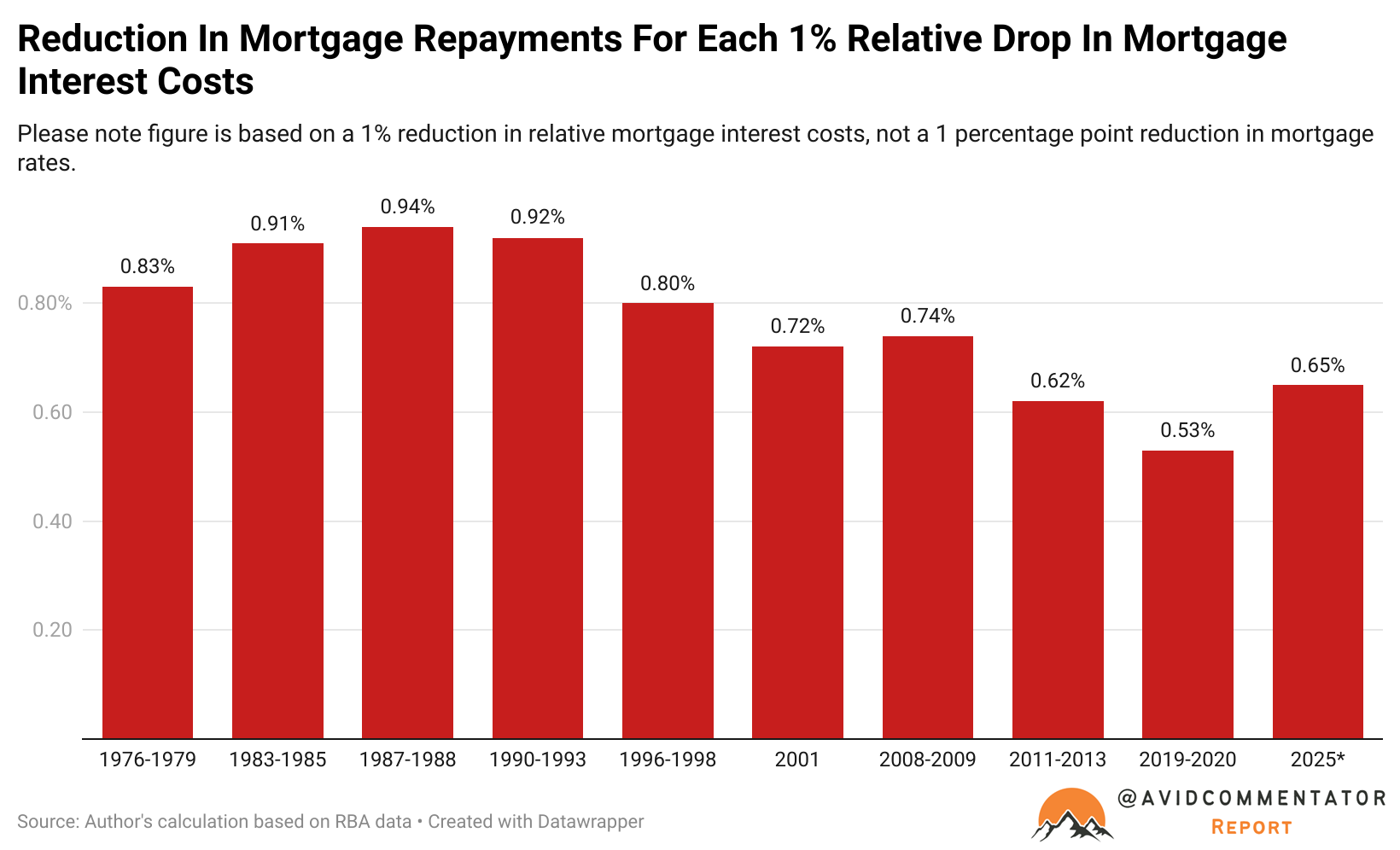

For example, during the 1990 to 1993 rate cut cycle, interest repayments fell by 48.5%, with total mortgage repayments falling by 44.5%.

If we compare that to even another “emergency” rate cut cycle, such as the one driven by the GFC, interest repayments fell by 42.8%, with total mortgage repayments falling by 31.6%.

The proportion of the decrease in interest costs to feeds through into the relative reduction in overall mortgage repayments can be quite dramatic. In the 1990-1993 rate cut cycle, for each 1% relative interest payments, total mortgage repayments fell by 0.917%.

Despite the GFC being another instance of “emergency rate cuts”, the impact on total required mortgage repayments was significantly different. In the 2008 to 2009 rate cut cycle, for each 1% relative interest payments, total mortgage repayments fell by 0.737%.

If the average non-crisis rate cut cycle were to play out in the present, for each 1% relative interest payments were reduced, total mortgage repayments will fall by 0.654%.

In short, rate cut cycles today are significantly less potent in terms of delivering overall savings to mortgage holders due to principal repayments being a significantly larger component of overall repayments.

The Boost From Rate Cuts

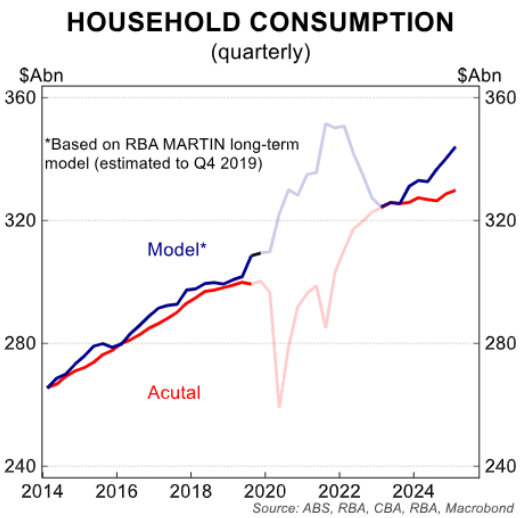

The current consensus expectation is that rate cuts will help to revive the consumer economy and significantly lift the growth levels of the consumer economy.

In the words of the recent Commonwealth Bank report on the May retail sales data: