Renting Aussie families earn less than home owning pensioners

We hear about the struggles of age pensioners and retirement. What about the struggles of everyone else? How do they really compare?

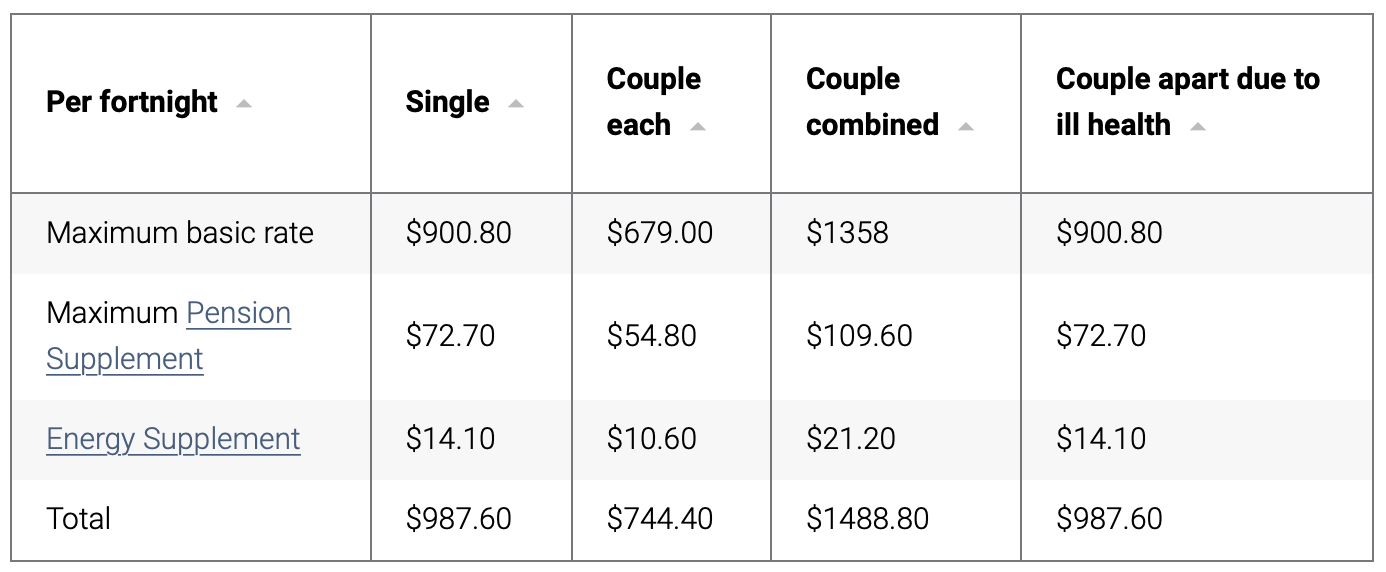

The age pension is $25,690 per year for a single and $19,350 for each pensioner living as a couple. This is what you get as a homeowning household.

People like to say that this isn’t that much.

Compared to the median household before tax income of $89,000, and the average of $116,000, it doesn’t appear like much.

But adjustments are needed to make a fair comparison.

You can’t say a family of four making $89,000 is better off financially than an age pension couple with a $38,700 pension just because one number is bigger than the other.

A fair comparison would adjust for

- household size,

- renting compared to homeownership,

- taxes, and

- family welfare payments.

After you adjust for these factors you can have a more accurate comparison of genuine purchasing power and quality of life.

A fair comparison

This comparison considers two neighbouring households—one a homeowning couple on the age pension, and next door, a renting family of four with a single income earner.

How much before tax income does that family need to have the same spending power as the pensioners?

We start by adjusting for housing size. A family of four obviously needs more money to be as well off as a couple. But how much more? The ABS uses an equivalisation process to adjust for different household sizes. They consider that a second adult needs only 0.5 times the income of the first for that couple to have the same spending ability as the first person living alone. This is why the couples aged pension is only 50% higher than the singles. Couples have many economies of scale from co-living.

An extra child aged under 15 years is considered to have costs equivalent to 0.3 of the first person. This seems a bit light to me. That would mean only $150 per week extra if there was a “couples with a child under 15” age pension. It would be tough to feed, clothe, transport, and educate my children for $7,800 per year each. I think a 0.5 weight is probably closer to the mark, but I’ll make it 0.4 in this analysis.

Remember also that pensioners get a variety of discounts on many daily expenses, and can also more easily take advantage of off-peak pricing for many services.

So when we add that up, the family would need $59,100 after tax per year (that’s 2.3x the single age pension) to have the equivalent spending power as our age pensioners.

Next, we adjust for renting versus owning. There is a huge amount of variation here. From $300 per week rental houses in regional areas to $800 per week homes in the capital cities. Perhaps the best way to deal with this is to run with low, medium, and high, rental scenarios of $300, $550, and $800 per week.

However, ownership has costs too, typically $100 to 150 per week. So we can subtract ownership costs of, say, $150 per week from the rental needs of the family for a like-for-like comparison.

Our scenarios for annual total after-tax incomes needed for these families to be equally financially well off as a home-owning age pensioner are (in round numbers):

- Low rent area – $67,000

- Medium rent area – $80,000

- High rent area – $93,000

Two more adjustments are needed—taxes and family welfare payments.

Legendary tax and transfer expert David Plunkett took these numbers and ran them through his tax and transfer model that accounts for all the welfare and taxes that affect this example family. We do one model where the main earner has a HELP debt (an income-contingent higher education loan) and one where they do not.

The before-tax incomes needed (net of superannuation) for a renting family of four with one income earner to be as financially well-off as a home-owning age pensioner in the three different locations are:

- Low rent area – $63,400 ($68,800 with HELP debt)

- Medium rent area – $95,300 ($123,900)

- High rent area – $128,000 ($153,000)

What do we learn from this?

First, the family welfare system works. The family earning $63,400 ends up with more income because they pay less tax than what they receive in family welfare benefits. Despite its often cumbersome administration, the welfare system is pretty amazing at keeping people out of poverty.

Yet weirdly, if this family had HELP debts they would be forced to repay over $5,000 of HELP debts and would therefore need to earn $68,800 to match the age pensioner household in the low rent area.

This leads to the second observation of extremely high effective marginal rates (EMTRs) faced by families in Australia. Going from the Low to Medium scenario requires the family to have an additional $13,000 net income. To get that, however, they have to earn an additional $32,000 of gross income. That’s a 60% EMTR across that whole income range. For those with HELP debt, the EMTR between the Low and Medium scenarios is a whopping 78%!1

The third and final observation is just how much income a family needs in Medium and High rent areas to be equally as well-off financially as their age pensioner neighbours.

A before-tax income of $128,000 is needed in high rent areas. Somewhere between 60-70% of full-time workers make less than that. A family of four making less than that income, while renting next door to an age pensioner couple in a High rent area, will actually be paying a huge amount of tax (up to $35,000) to subsidise the income of their pensioner neighbours who in reality have a higher disposable income than the family does.

Even in Medium rent areas the $95,000 needed to match the financial well-being of a home-owning age pensioner is above the median full-time earnings nationally and only a couple of thousand below the average full-time earnings. The family here pays $15,000 in tax while being worse off financially than a homeowning age pensioner couple.

This analysis suggests that there are many families renting in our expensive towns and cities doing worse financially than age pensioners. The craziest part of this story is that so many people think it is really important that families in these situations spend 10% of their income buying financial products in their superannuation. Yet in every case, the age pensioner is already better off financially than they are.

Dr Cameron Murray is co-author of the Book Game of Mates. Subscribe to his written work at Fresheconomicthinking.substack.com.