Uncertainty is nothing new when it comes to investing. In fact, the world. and life in general, are inherently uncertain. I want to explore some concepts and give some practical ways to overcome this in the investment context, particularly in regards to investing in growth assets, such as the Australian & US stock markets and the Australian property market.

The conversations I’m having with many clients at the moment is they are sitting on the sidelines or unwilling to invest more capital due to market uncertainty. They all seem to be saying similar things but expressed in different ways. The number one cause is fear. Fear of the future, fear of the unknown and fear of a downturn. Many people are saying the markets are so high and valuations are stretched. People are fearful of inflation and interest rate rises and the likelihood that it will be negative for property and stock valuations. There is also a lot of lingering fear in society around COVID and how it is going to affect our lives going forward into the future. A potential cause of this uncertainty is people are often overly influenced by the media. Seeing negative headlines can produce a fear response and often this is stronger than the positive news stories and people can be overcome by this. However, if you can see through that negative bias and understand there are actually many more things to be optimistic about as a long term investor, this will leave you in good stead.

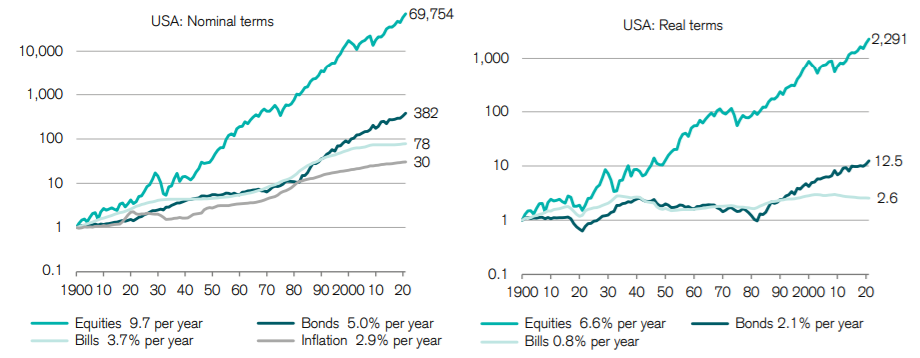

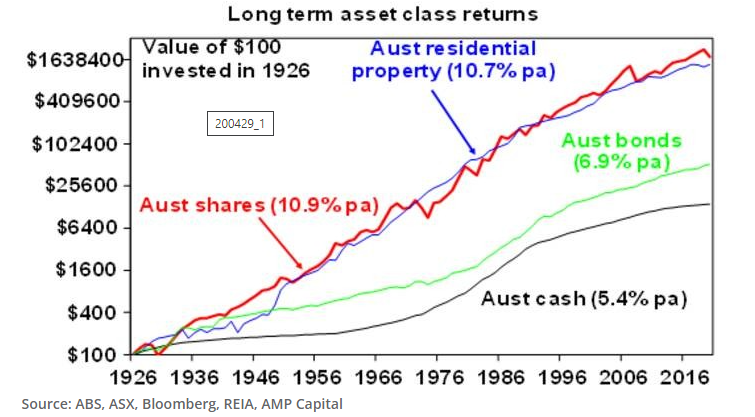

If we look to the past there has always been uncertainty in many forms. There have been wars, famines, booms and busts, almost every imaginable event under the sun and markets have always gone on to make all-time new highs.

I want people to ask themselves the question, Is now really any different to the past?

If you look at the stock market or the property market and the growth of your capital over the last 100 plus years, you will see all these events and exceptional returns. If you align your capital with these markets you are likely to be handsomely rewarded over the long term for making that investment and taking that risk. With this understanding, you have to embrace uncertainty if you want to reap the rewards that markets can offer. Volatility is just the risk that you have to take to achieve those higher long term expected returns from growth assets. What is meant by volatility is the natural ups and downs of the market and hence the risk of capital loss.

I believe this uncertainty is just human psychology playing out and often it is irrational when looking at the positive drivers for business and property over the long term.

Source: Credit Suisse Research Institute – Credit Suisse Global Investment Returns Yearbook 2021 Summary Edition

What people may not understand is that markets in the short term work on supply and demand rather than just reflecting fundamentals. What I mean by that, is that if there are more buyers than sellers the market will rise and conversely if there are more sellers than buyers markets will fall. This is independent of the fundamental value of the underlying securities. Warren Buffet has famously said – ‘In the short run, the market is a voting machine, but in the long run, it is a weighing machine’. So in the short term, anything can happen but over the long term, the returns that tend to show up are very likely to be positive and reflective of business growth.

What are the risks of investing now?

Often when people are looking at the market, they are always looking to the past and not what the future of the chart may look like. There is timeless wisdom that says it is about ‘time in the market rather than timing the market’ and that still holds true today. If you are a speculator rather than a long term investor your risk of the capital loss is always higher as you are trying to get in and get out in a short time period for a profit. The greatest risk with any investment is generally in the short term after you make the investment as there is the highest chance that your investment will fall and you would be in a negative equity position. The longer your time horizons are and the longer you hold your investment for, the lower your true risk of capital loss is because you have time to ride out any short term corrections. There is also more chance that your investment will increase over time with the natural appreciation of markets and therefore your risk will reduce. This is especially true if you are reinvesting dividends and paying down debt also. For the long term investor, the inevitable market pullbacks will likely be inconsequential in the big picture, especially if you are saving and investing regularly over that time period (and reinvesting dividends and paying down debt) and taking advantage of compounding returns. However, the risk of volatility is always there, as that is inherent in markets and remember, you only lose if you sell when the markets are down.

What are the risks of not investing now?

Many people are waiting for the market to fall and then they will invest. However, this can be a risky strategy that leaves many investors on the sidelines for years not knowing when to get into the market (or back into the market). With capital sitting in cash in the current climate you are receiving a negative real return after inflation is taken into account which is not a great strategy..

You might be waiting for a pullback that never comes. You may miss the boat and markets might take off again and you miss out on potential gains. There are numerous examples of this in the past like the GFC & COVID. People who got scared out of the markets, crystallised losses when moving to cash. They then missed the recovery and were left sitting in cash with a very low return outlook compared to riding out the volatility; often uncertain about when to get back into the markets. If they hadn’t sold and stayed invested they would be much better off now than before these events.

How to combat uncertainty

Often people know what to do but they can’t get themselves to do what they know they should do. The link here is found in behavioural finance, getting yourself to take action in the face of uncertainty and doing what you know you should.

One way to mitigate the numerous biases and errors humans are prone to is to have a plan and stick to it.

You cannot control the market but it is wise to focus on what you can control:

- your asset allocation,

- whether you invest or speculate,

- when and how much and how often you can invest.

If you are going to regularly invest. Just do it and stick to your plan, regardless of what the market is doing. It’s best to automate this as much as possible to mitigate investor biases and human emotion. To reap the higher expected returns from growth assets and take advantage of compound returns you are best to invest regularly and stay invested for the long term.

However human emotion can get in the way, we saw many investors spooked out of the market like during the 1987 crash, The Dotcom bust, the GFC and the Covid-19 event. Thus derailing even the best plans. Hence why an automated plan is best.

If you have some capital and are sitting on the sidelines waiting to invest. There are essentially 2 options:

- one-off lump sum investing, and

- dollar-cost averaging.

Lump-sum investing is where you put all your capital into the market at once whereas dollar-cost averaging is where you drip feed your capital into the market over a set period of time. – In this Vanguard white paper ⅔ of the time investors are better off with a lump sum investment rather than dollar costs averaging into the market.

Lump-sum investing gives you more exposure to the market sooner and Vangurad’sresearch shows that investors get better outcomes by lump-sum investing as they have more capital in the market for longer. This may be more difficult psychologically if you are concerned about the value of your investment decreasing in the short term but gives you better long term outcomes more often than not. ⅓ of the time this doesn’t work in your favour and if you are concerned about your investment falling in the short term then dollar-cost averaging is easier to handle psychologically, is a lower risk strategy but is also a form of market timing which is very difficult to do as you are expecting the market to fall. One advantage of dollar-cost averaging is if markets do fall you can dump the rest of the money in when it is lower and ride the next wave up from a lower entry price and increase returns. However, this is not as likely and you still have to time the market.

Additionally, you can outsource to a professional money manager that factors in the uncertainty and the likelihood of market corrections. Nucleus Wealth takes this uncertainty into account with our active asset allocation within our tactical portfolios. This is the perfect style of fund that takes into account the uncertainty and manages that risk for you.

Having access to a financial adviser is an important step to having a solid plan and implementing these understandings.

If you would like to speak with me or one of the team at Nucleus Wealth to discuss your personal investment situation please book a call here as there is no cost to have a conversation to see if we can help.

Final Thoughts

Uncertainty is nothing new and it needs to be expected and embraced. The stock market is ultimately a reflection of human endeavour and in my opinion, human nature has not changed and people are always going to innovate and create new products and services and bring them to the market. From my perspective, the future is bright regardless of what is happening in the fleeting short term. My bet is that history will likely repeat itself and we will look back at this time in the future and wonder what everyone was worrying about and were very glad we invested for the long term when we did.

————————————————-

Samuel Kerr is a Senior Financial Adviser at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Samuel Kerr is an Authorised Representative of Nucleus Advice Pty Limited, Australian Financial Services Licensee 515796. And Nucleus Wealth is a Corporate Authorised Representative of Nucleus Advice Pty Ltd.