September 2021 Australian property market affordability update

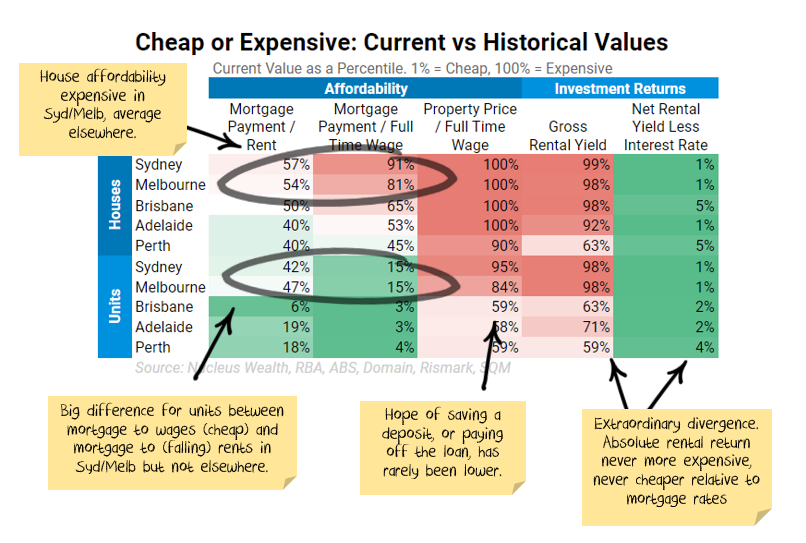

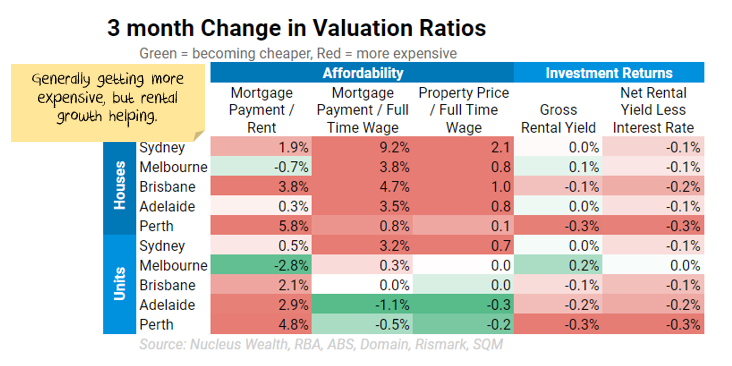

Australian property market prices continued to climb over the last month, with the past six months seeing some of the strongest growth on record. Mortgage fixed interest rates rose slightly, standard variable rates fell slightly but remain significantly above fixed rates. There are some extraordinary divergences in affordability. It has never been cheaper in some markets to service a mortgage, but never more expensive to save for a deposit or pay off the loan.

In general, housing valuation and affordability statistics worsened over August. For investors, rental yields have never been lower in an absolute sense, never higher relative to mortgage rates.

Regulatory actions in the background are worth watching. We are not expecting rising interest rates, but markets are starting to price them in. Last week the Reserve Bank of Australia had to intervene to keep interest rates in their desired range. We note even without official interest rate rises, bank funding costs will rise due to other regulatory changes. It is likely this will flow through to higher interest rates even with no official rate rises.

The Federal Government and Reserve Bank have successfully distorted conditions to encourage as many people as possible to borrow as much as possible. An investment in housing is basically a vote of confidence in their ability to keep force-feeding the market.

We run an Australian property market calculator to help investors or potential homeowners determine the returns on Australian property. The idea we want to illustrate is that there are a number of key inputs into housing valuation. Interest rates are the most important, but the other limiting factors are:

- Mortgage Payments to Rent: comparing the cost of a mortgage with the cost of renting the same house. Using this ratio to constrain house prices, we assume that people will prefer to rent when the ratio gets high rather than buy.

- Mortgage Payments to Wages: assuming when the ratio gets high, people rent because they cannot afford to buy.

- Property Prices to Wages: assuming when the ratio gets high, people rent because they cannot save enough money to afford a deposit. We treat this as less important than the above two ratios.

- Rental Yield: Rental yield is the annual rent divided by the property price. By using this ratio to forecast prices, you are assuming when the ratio gets low investors will not buy property as they are not getting a return that is high enough.

For the details charts for the above locations see the property detail update. For more on how and why we use these ratios see our residential real estate forecasting methodology.

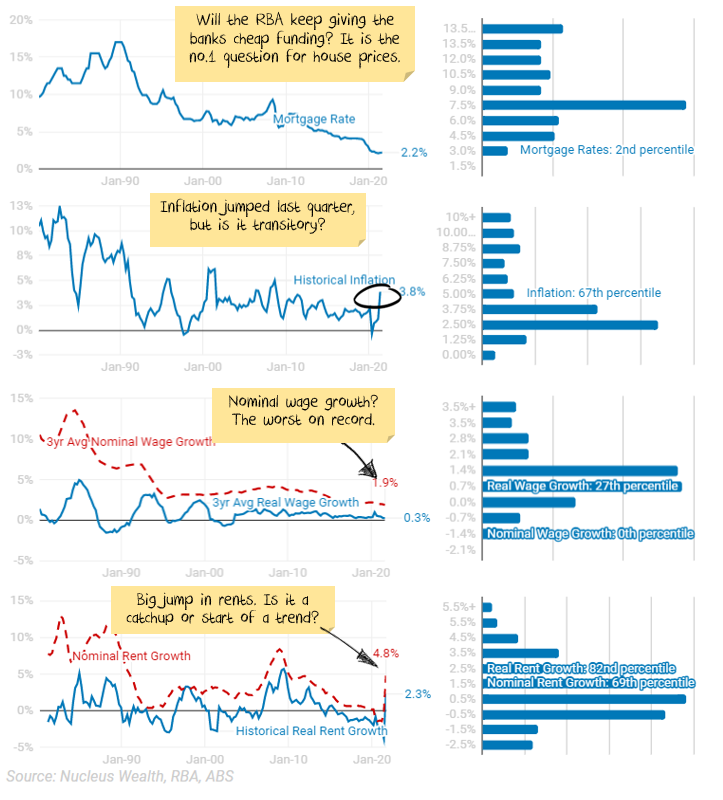

Australian mortgage rates can go lower but look like rising first.

There are effectively two different interest rates at the moment, the floating rate and the three-year fixed rate.

- The floating rate is determined mainly based on the Reserve Bank of Australia. It reduced the floating rate to 0.1% in March 2020, which reduced the standard variable rate from banks to around 4.5%. This is unlikely to change.

- In March 2020, the Reserve Bank also introduced a facility where they lent directly to the banks at 0.1% for three years. This facility (and other market interventions) allowed banks to drop three-year fixed mortgages to around 2%. Its name is the Term Funding Facility. It ended at the end of June.

When you adjust the factors in our property market calculator, you find that with low inflation, wage growth and rent growth that interest rates become even more important for determining property prices. But forget about the cash rate. The important factor is three-year fixed interest rate. This has risen very marginally. It seems likely the three-year rate will continue to rise unless we see further government or Reserve Bank intervention.

The short/medium term supply myth

Don’t get me wrong. The number of houses that get built matters eventually. But, in the short and medium term, affordability matters more.

The reason is that the stock of houses dwarfs the year to year supply numbers:

- Each year Australia builds 100,000-200,000 dwellings

- There are about 11m houses

- 11% are unoccupied (i.e. second homes, holiday homes, unleased properties etc)

- At last census, there were 2.6 people per occupied dwelling

Do you want to absorb 350,000 new dwellings? Fewer flatmates per house, more young adults moving out. It doesn’t even show up in the rounded ratio of 2.6! Officially the number of people per occupied dwelling was 2.64. Change that to 2.55 and there are 350,000 new homes occupied.

How about another 150,000 new dwellings? Same trick with the rounded unoccupied rate of 11%. Change it from 10.5% to 11.4%.

Net effect: you could spend three or four years building another 500,000 dwellings, the population could stay the same, every new home could be bought and there would still be 2.6 people per house and 11% unoccupied.

I’m not arguing that supply doesn’t matter. It does. But over five year periods, affordability plays a far larger role.

Macro factors

Australian Property Market Outlook

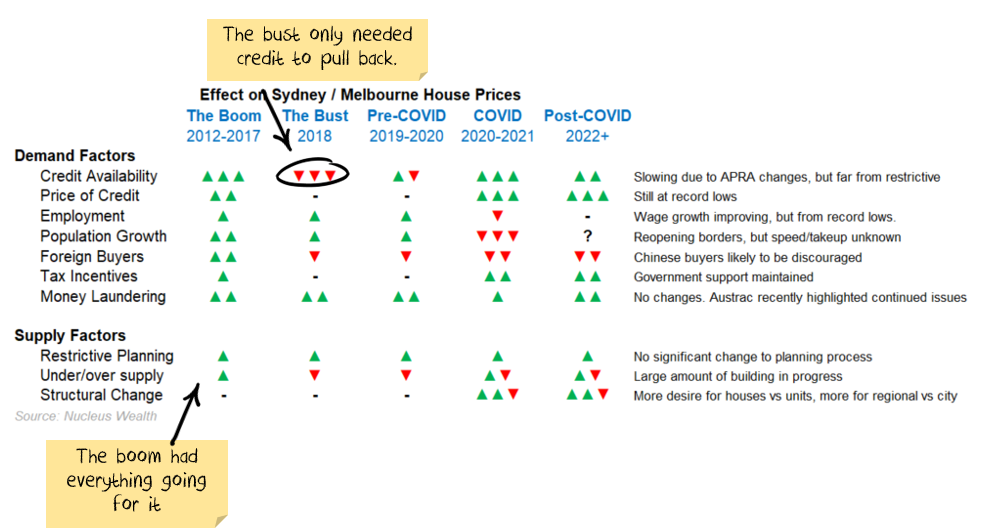

Property prices have been ripping higher in recent months. This has dented a number of affordability measures, but ongoing conditions appear as positive as they have been for some time.

On the one hand, plummeting immigration, pandemic disruptions and the end of eviction/mortgage payment moratoriums aren’t helping. A boost in supply is in progress, spurred by new home building. Rental growth jumped this quarter, but the last few years have been very weak. And Australia starts with a larger private debt burden than just about any other country.

On the other, we have a burning political desire to keep Australian property market prices high and pump more debt into the economy. Wage growth is low, meaning interest rates can stay lower for longer. We have a roadmap to much lower interest rates to help. There is a structurally higher demand for houses vs units due to the fear of more lockdowns.

Australia is stuck in a debt trap. We’ve got so much debt we can’t raise rates because it makes it more difficult for people to pay back debt. To get more growth we have to cut rates, so people borrow more and the cycle goes on.

In the meantime, there are other ways to keep the property party going. Once mortgages were for 20 years, then 25, now 30. Soon it will be 50. Japan has 100 year mortgages. Many people will never pay their mortgage back, so owning a home might become like renting – just that it’s renting from the bank.

Sources:

Nucleus Wealth has compiled this data using a range of different sources.

We use Domain for more recent data quarterly property prices and rents, cross-checked with SQM to fill any short-term moves. Older information is from Rismark and the Australian Bureau of Statistics to fill time series.

For economic data, we use either Reserve Bank of Australia or Australia Bureau of Statistics data. For older data, we have had to estimate some factors due to differing definitions over time.

————————————————-

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.