Explainer: Do taxes on property cause high house prices? No.

Housing industry lobbyists in Australia and abroad often claim that property-related taxes comprise a large and growing share of the price of new housing and are hence pushing up the market price of new and existing dwellings.

Land taxes, stamp duties on property transactions, GST on value-added investments, and other fees and charges are generally included in this analysis, as are many inferred price effects that are assumed to be due to regulations.

This note explains four reasons why the claims of this tax summation approach are not valid.

- Many of the included costs are not taxes on new housing.

- Adding indirect taxes double counts.

- Assumed price effects are implausible.

- Taxes on property assets reduce market prices, not add to them.

A persuasive tax story

Lobbyists for property owners and developers often circulate in the media personal stories about the burden of taxes on new home buyers. Behind these persuasion efforts typically lies an economic analysis of taxes and new housing by CIE economic consultancy based on a “tax summation” approach (and often not publicly available).

For at least two decades, the Housing Industry Association (HIA), Property Council of Australia (PCA) and the Urban Development Institute of Australia (UDIA), have used this strategy.

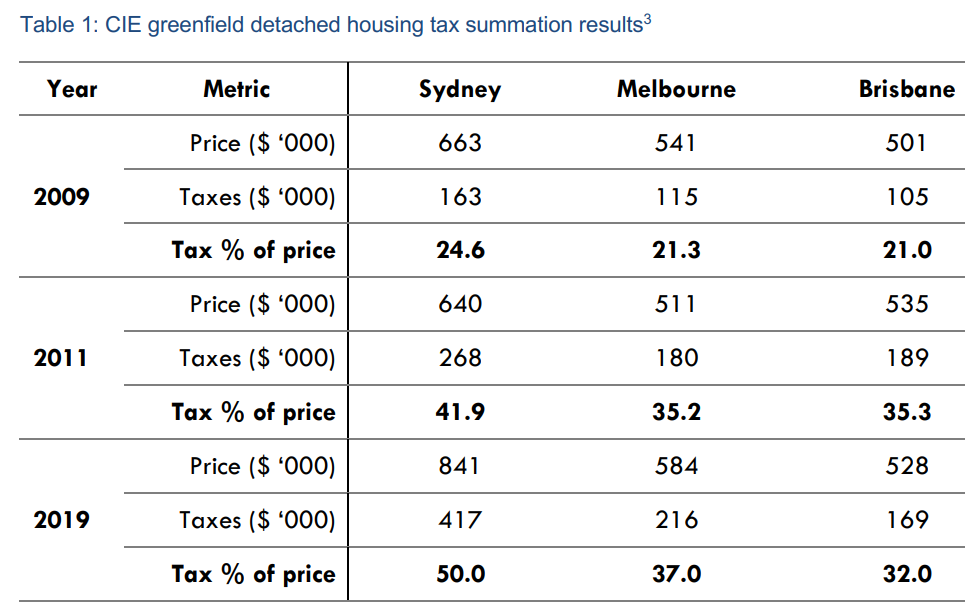

Three of these tax summation reports are summarised in Table 1. The estimated share of the median new dwelling price that reflects total taxes was 24.6% in Sydney in 2009 and 50% in 2019. In that time, Sydney dwellings increased in price from $663,000 to $841,000. Total estimated taxes related to the production of new dwellings went from $163,000 to $417,000.

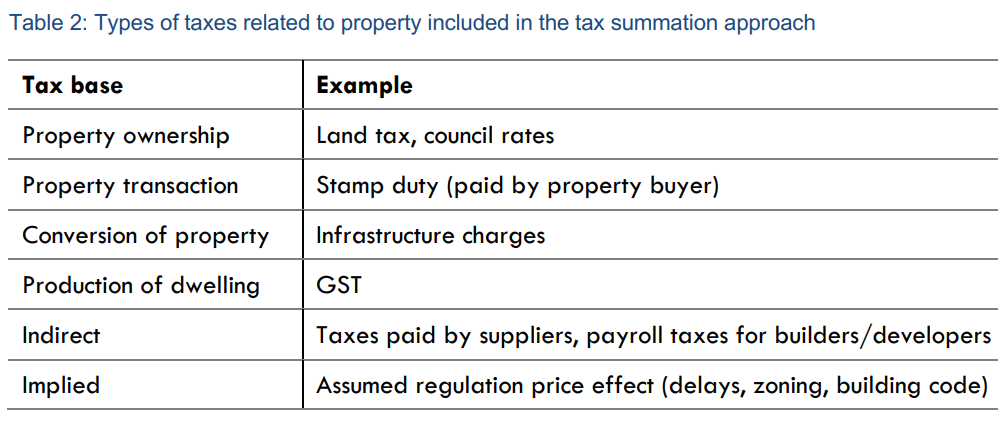

The economic reports that sit behind these claims use a tax summation approach. All taxes, fees, or charges that are related to property ownership, transactions, or housing production, are added together and compared to the market price of a new dwelling. Table 2 shows the typical inclusions in the tax summation approach. The included taxes and charges are often levied on a different property-related activity (known as the tax base).

Indirect taxes are an unusual inclusion in the tax summation approach. For example, in their 2003 report, HIA included payroll taxes paid by construction and development companies as a tax on new housing. In a 2015 report, the cost of broadband connections was included alongside an assumed cost of complying with building codes. GST on the value-added in property development is also often included as an indirect tax on new housing.

One of the largest components in the tax summation approach is a price-effect due to regulations. For example, zoning regulations are assumed to add significantly to the price of developable sites. Potential delays in planning approvals are assumed to add risk and require higher margins for developers, with this additional margin counted in the tax summation approach.

The overall argument is that if these taxes and charges were removed, the market price of both new and existing dwellings would fall by the total tax amount.

International example

In the United States, the lobby group for homebuilders, the National Association of Home Builders (NAHB), based their recent analysis on a series of survey questions that required builders to estimates the percentage of costs due to comply with particular regulations. These percentages were added together and applied to the market price of housing. In 2021 the typical new home was $394,300, the sum of surveyed percentages was 23.8%, and the implied tax burden was $93,870.

Lacking economic sense

Not a tax on producing new housing

Land taxes and council rates paid by property owners are not taxes on the production of new housing. They are recurrent taxes on the ownership of property whether housing is built or not. They are therefore not a cost of producing new dwellings.

In fact, building and selling dwellings faster reduces the amount of these taxes paid. These taxes incentivise faster new housing development.

Indirect taxes

It makes little sense to include some of these identified indirect taxes, like, payroll taxes for developers and builders. Just as the taxes paid on wages by the workforce would not be included, nor the GST that the workers’ pay when they buy lunch.

Because the economy is circular in its exchanges (money flows between households and businesses and back) if you add indirect taxes from supply chains your summation will double and triple-count (and more) taxes paid. If all industries took this approach to adding up the taxes they pay, the total would be more than all taxes paid across the economy.

Assumed price effects

The largest components in the tax summation approach are the assumed price effects of zoning, delays, and building codes.

For example, HIA’s 2011 report assumed that $40,381 was an “excessive land price” for each dwelling site, being 29% of their total summation of $141,545 in taxes associated with new dwellings. This approach amounts to relabelling of property asset values as regulatory costs.

The cost of delay attributed to planning also relies on questionable assumptions. HIA’s 2011 report attributed $38,094 to delays. Several assumptions compound to generate such figures.

1. The time taken to approve an application means new dwellings are sold slower than otherwise would occur.

2. The choice of what planning application is made is irrelevant. Yet applicants choose whether to apply for a project design that is likely to be quickly approved or one that is likely to not be approved or involve time-consuming processes.

3. That the choice of when to make a planning application is unaffected by the time taken to approve. If property owners know in advance the time required, they can apply sooner and factor this into their project schedules.

If these assumptions do not hold, then there is little economic meaning in these cost estimates.

Major flaw: taxes reduce asset prices

Some taxes and charges are directly related to developing housing, such as infrastructure contributions. In the build-to-order Australian housing market, the stamp duty paid by the buyer of a new home is also arguably a tax triggered by the production of new homes.

It is important to note that stamp duty and GST are levied as a percent of value and only rise if the value rises. Thus, they are not contributing to price rises, but are the result of them.

But more importantly, since property is an asset that is priced based on expected future returns — be it a development site or a new dwelling — the known additional costs that come with owning the asset reduce its market price rather than add to it.

Tax obligations reduce the net return of the asset. Hence the market value of an asset will be lower to account for those tax obligations.

This means that, for example, because buyers know they must pay stamp duty on property purchases, they will reduce how much they are willing to pay the seller by the tax amount so that the total cost reflects their willingness to pay for that asset return. If stamp duties were removed, buyers would spend that tax amount on paying the property seller more instead.

The same logic applies to infrastructure charges. This additional cost is factored into the price paid for a site by a developer. Higher charges reduce the value of developable sites but do not affect the price of new housing, which is instead prices based on its economic returns, not its input costs.

This fact is so uncontroversial it has persisted from the classical economists of the 18th century to modern industry practice manuals and financial assessment tools used in property development.

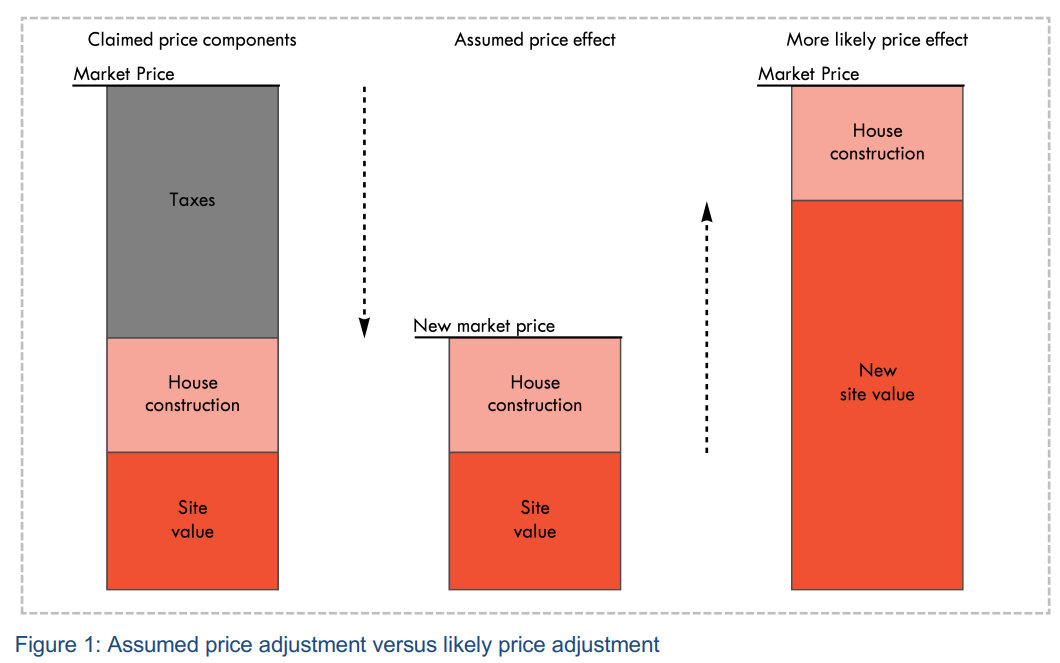

Figure 1 shows the claim made by housing industry lobbyists and the more accurate asset pricing view of taxes and their price effect. The left column takes at face value the claim that 50% of the price new detached dwellings is due to taxes, with the remainder as site value and construction cost. The next column of shows the implied logic of the price effect on housing assets if the taxes involved with property ownership, transfer and development were removed.

If this price effect was true, property industry groups have been lobbying to wipe trillions in asset value from homeowners and landlords. The more accurate view is that when taxes are removed from property ownership or development the value of these taxes is transferred to the owners of development sites through higher asset values. The right column of Figure 1 shows this effect, where taxes involved with developing housing are removed and this results in a rise in value of development sites with no effect on new housing prices.

Property owners lobby to remove taxes on development to increase their site values.

Final remarks

While it is certainly valid to examine the effect of property taxes on the incentives to convert property into new housing, the tax summation approach commonly used by property lobbyists is not valid. Taxes on property ownership are generally very efficient taxes for the very reason that they reduce property asset values and can incentivise investment in new housing.

Dr Cameron K. Murray is a Post-Doctoral Research Fellow in the Henry Halloran Trust at The University of Sydney. He is also co-author of the book Game of Mates: How Favours Bleed the Nation. You can find Cameron’s work at Fresh Economic Thinking.