What chance does a political party promising to radically reduce home prices to improve affordability have of getting elected?

The electoral calculus is simple. There’s no chance. If they say they want to, they are lying. This reality is why the Federal Budget included policies to boost housing demand but do not expand the supply low-cost housing alternatives.

The reality is that the richest seven out of ten households own $7 trillion of housing wealth in Australia. That’s $7,000,000,000,000, or seven million-million dollars. Every single 1% price decline wipes off $70 billion from the balance sheets of these households.

Yet we find ourselves in the bizarre situation where politicians are obliged to talk like they want home prices to be lower and “more affordable” but must act in ways that support higher home prices. We can only conclude that our housing market is exactly where we Aussies want it.

Consider these figures from a recent working paper I produced with Josh Ryan-Collins. Bank lending for housing grew from 20% of GDP in 1990 to 80% of GDP today. Business lending for investment grew from 35% to 40%. We have used the power of banking to bid up house prices by trading them with each other while neglecting investment across the business community. No one saw a problem with this because it helped house prices grow.

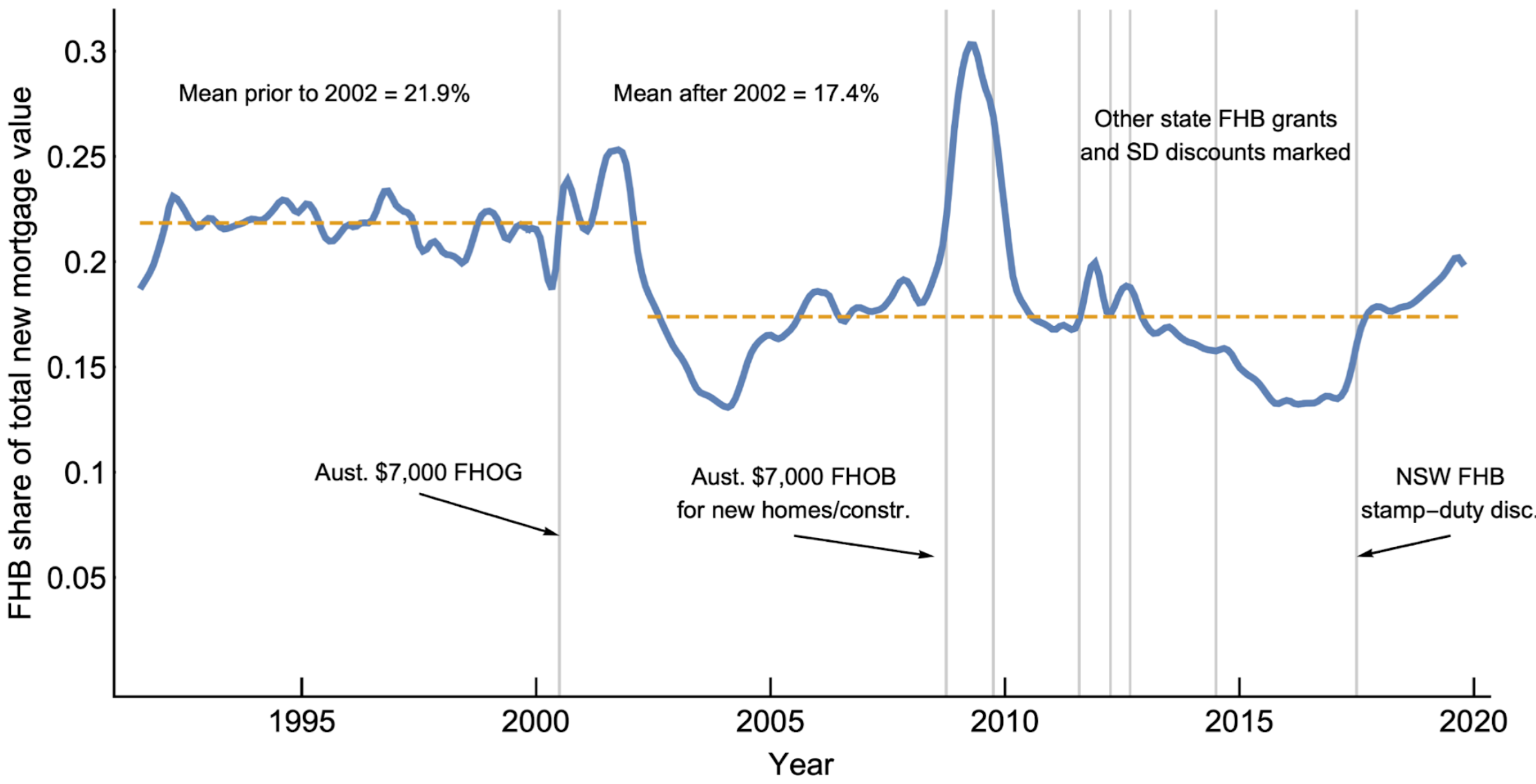

While the media celebrated the ‘booming’ real estate market, during the 2010s homeownership rates fell from 70% to 65% – back to levels last seen in the 1950s. The main difference between now and then is that governments of the 1950s intervened strongly to get more people into homeownership with public loans for new homes, direct public land provision, and rent controls on landlords that prompted many to sell to owner-occupiers. The state also provided extensive public housing alternatives, with nearly 15% of new supply being public housing in the 1950s compared to just 2% across the past decade.

You can see why our housing situation is so attractive for the homeowning cohort by comparing the economic returns from housing to wages. In the seven years to June 2019, the median Sydney home earned as much from rent and capital gain as the median Sydney full-time worker! This is astonishing. Capital growth of all land, not just residential, went from 9% of GDP on average between 1960 and 1980, to 17% of GDP since 2000, roughly twice the relative return to landowners than just 40 years ago.

Reversing these trends will benefit younger generations who are resigning themselves to the fact that homeownership is beyond their reach. While the “bank of Mum and Dad” has helped shift some housing wealth down the generations, it has entrenched inequalities. Waiting for inheritances won’t work either. The average age of receiving an inheritance is 64 years.

Housing is a defining social issue of our time. We have many technical solutions in our working paper, but the sheer economic value at stake and the political realities of this mean that change won’t be easy.

The problem with making home ownership more affordable is not a small elite locking the majority out: a lot of us (ie homeowners) have a lot to lose if we want to share the joy of a home of one’s own.

This was first published at Sydney Business Insights.