Australian dollar eviscerated as Fed unleashes QE4 to no effect

Thankfully, DXY finally got its safe haven mojo back last night as global markets crashed:

The Australian dollar was eviscerated:

The traditional gold panic sell began:

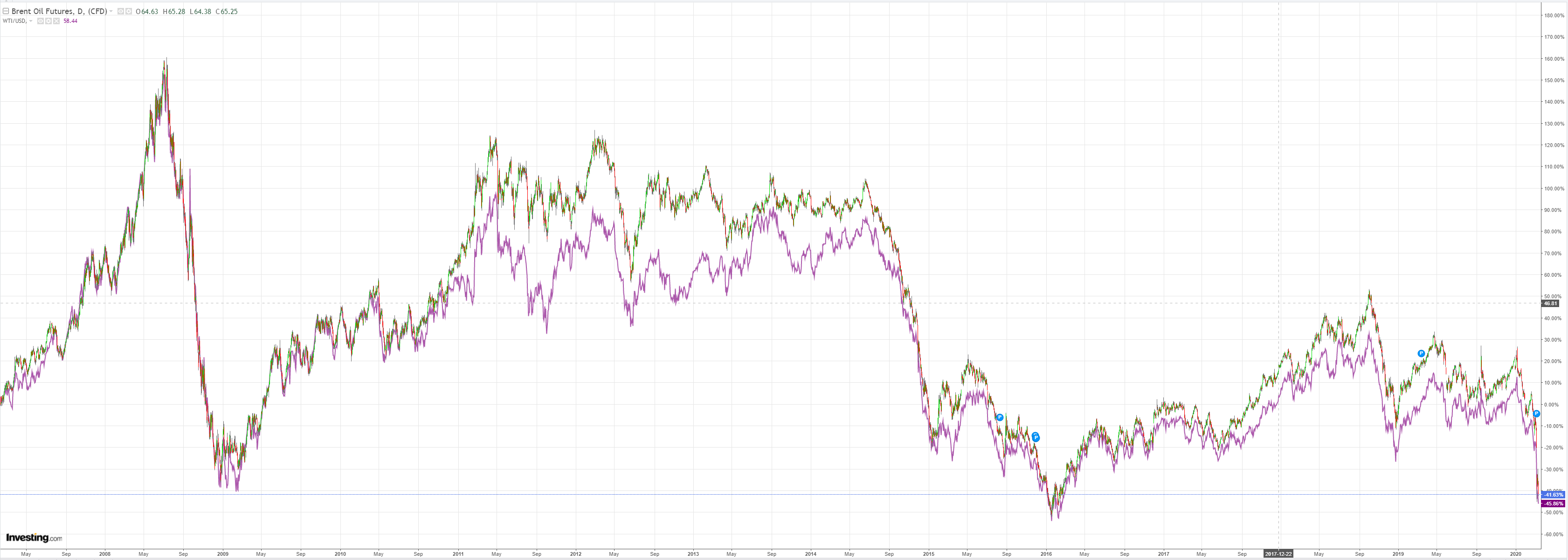

Oil is going to $10:

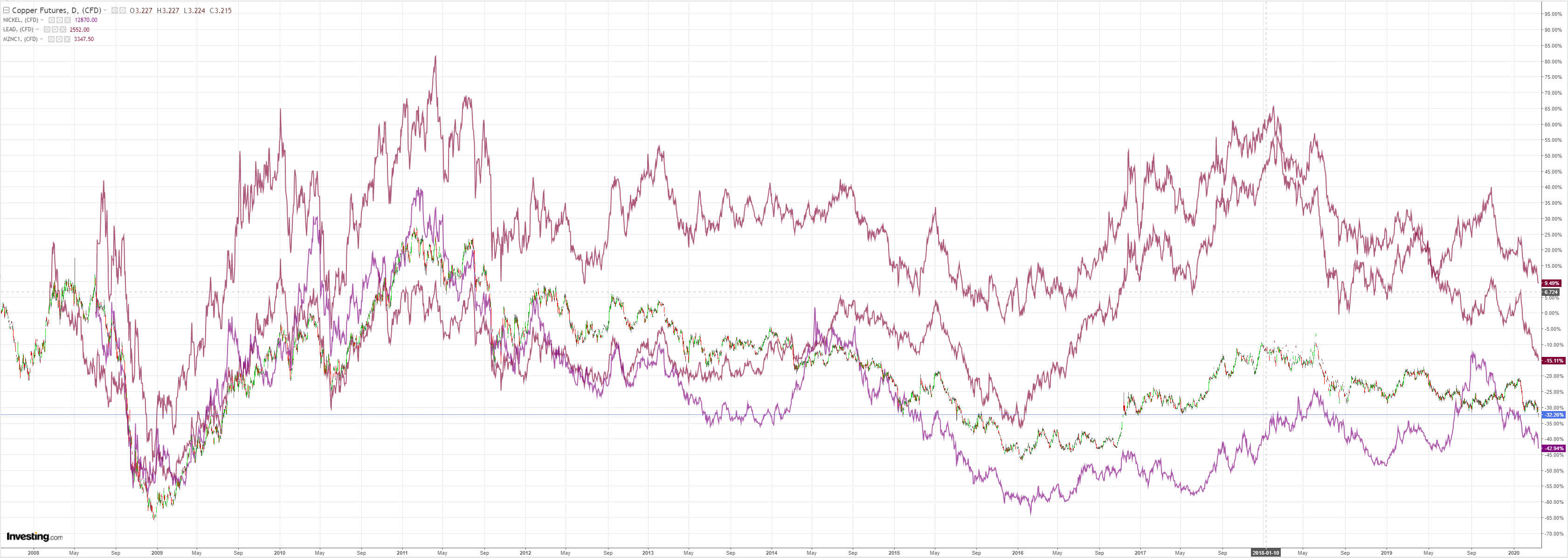

Base metals too:

Base metals stepped into a bottomless pit:

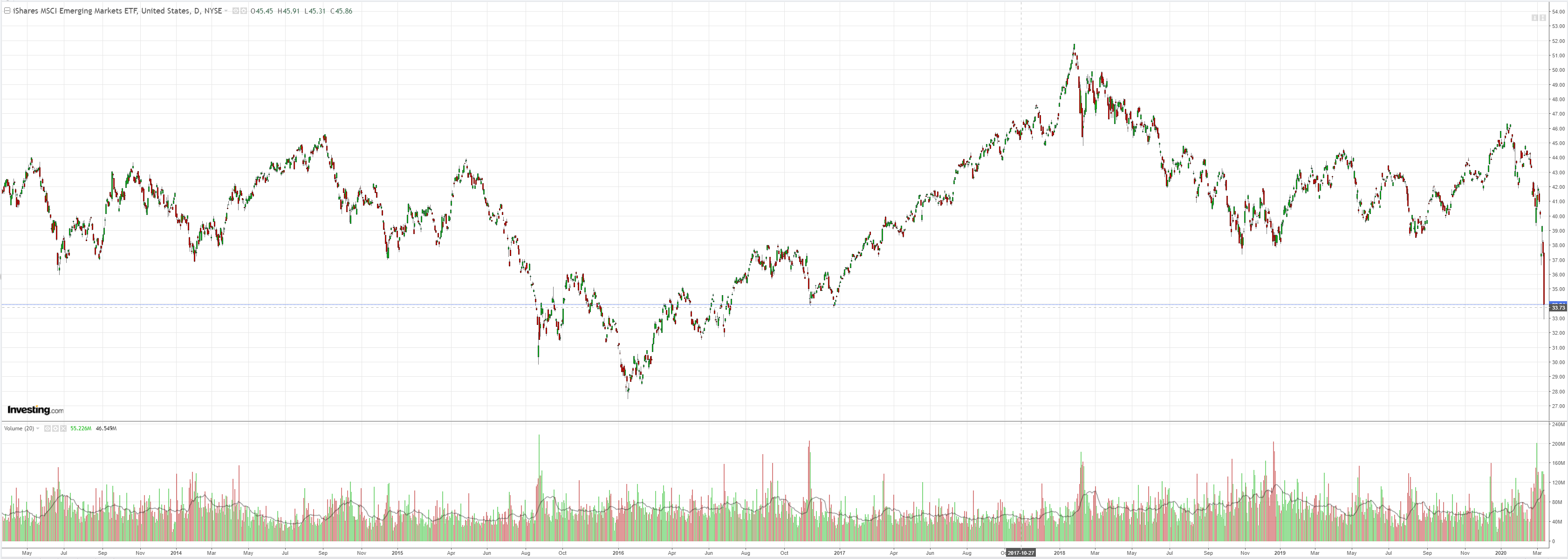

With EM stocks:

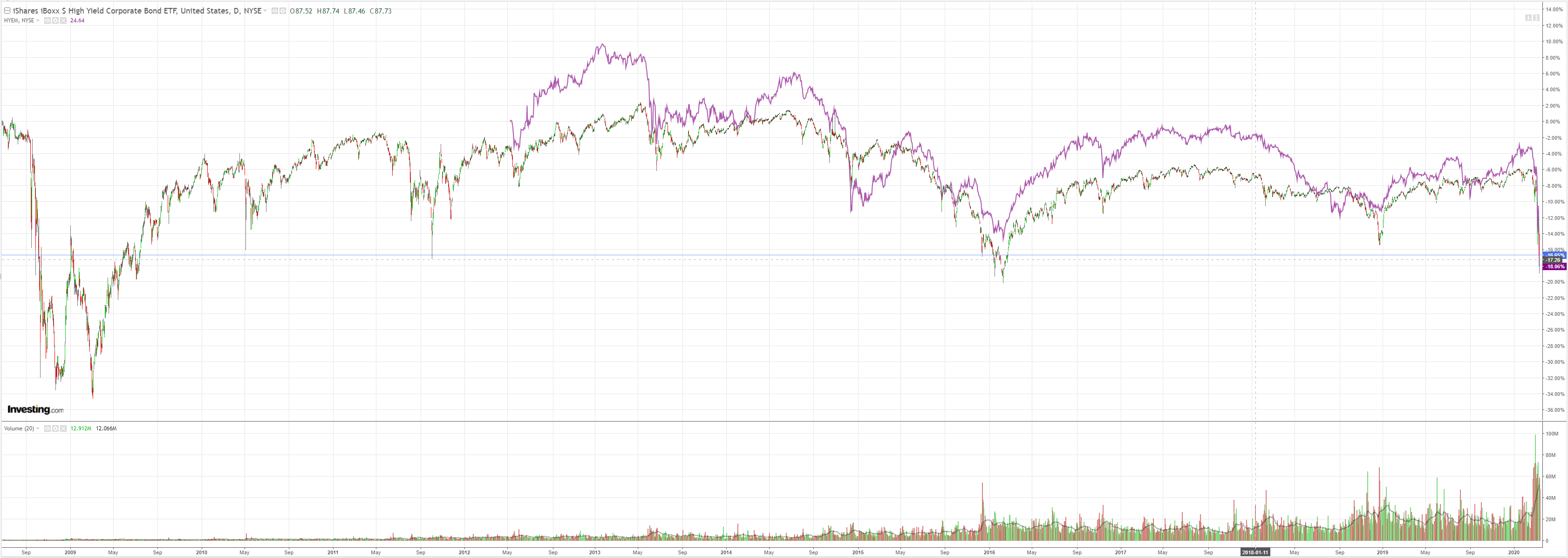

Junk crashed but stocks need to draw a bead on how much further it has to fall:

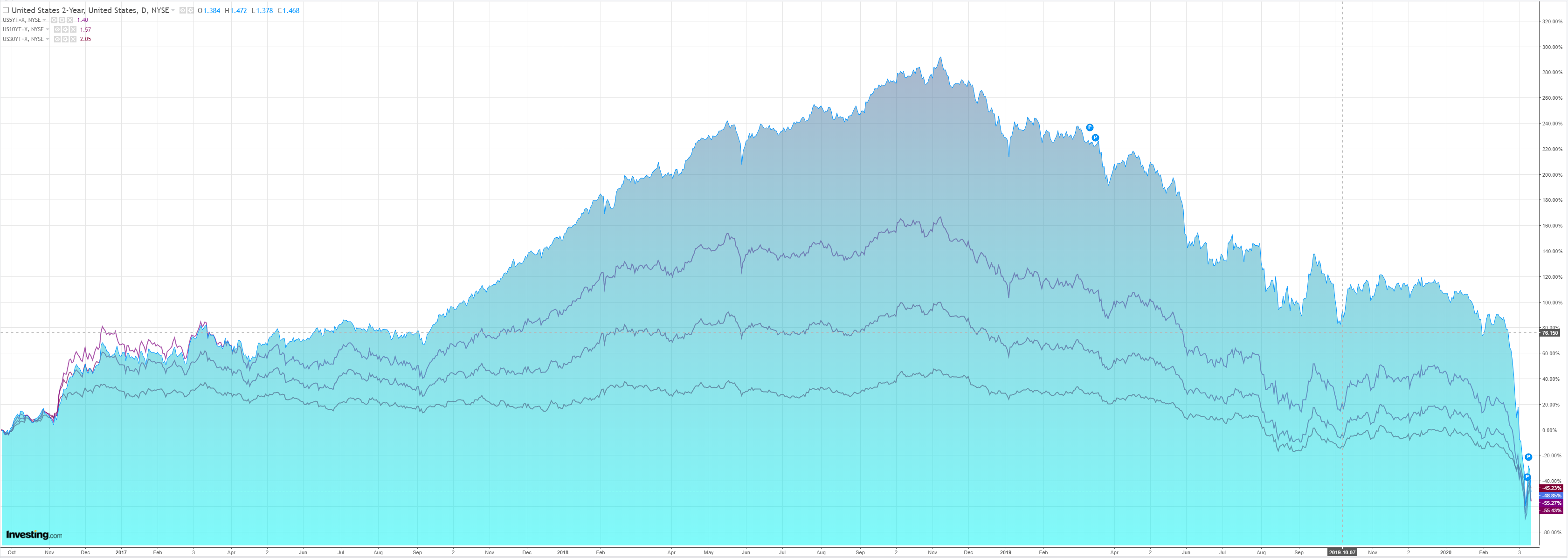

Treasuries were bid:

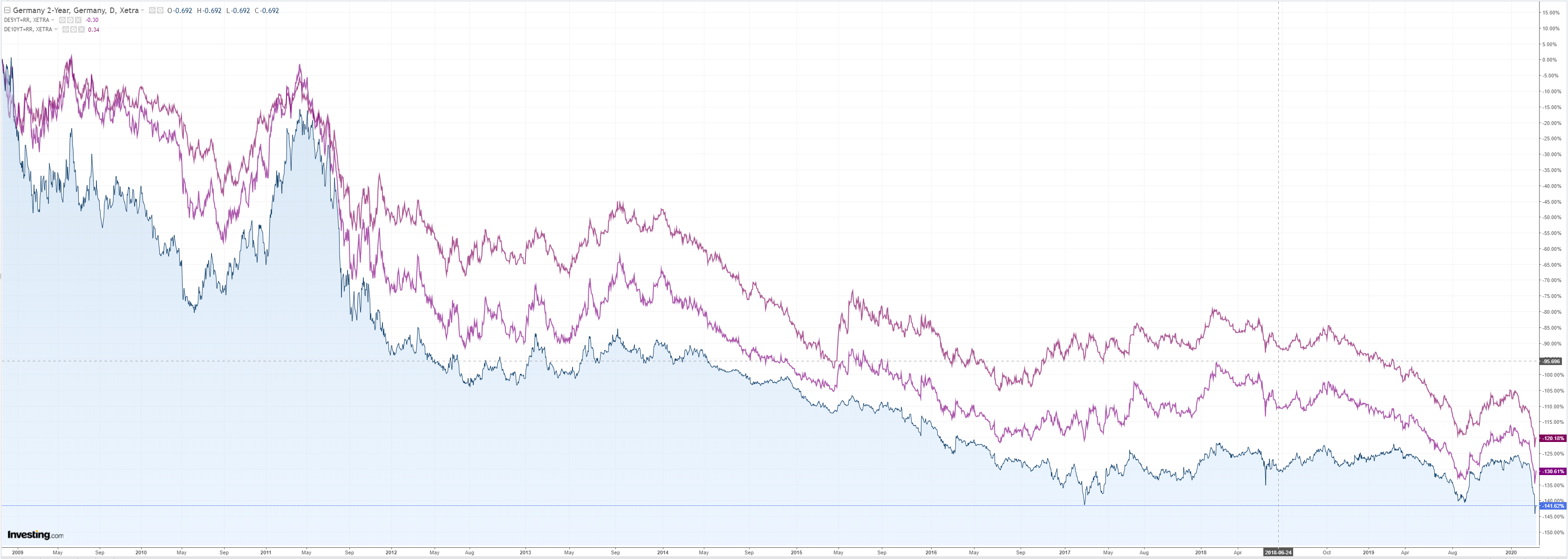

Bunds not:

Nor Aussie bonds:

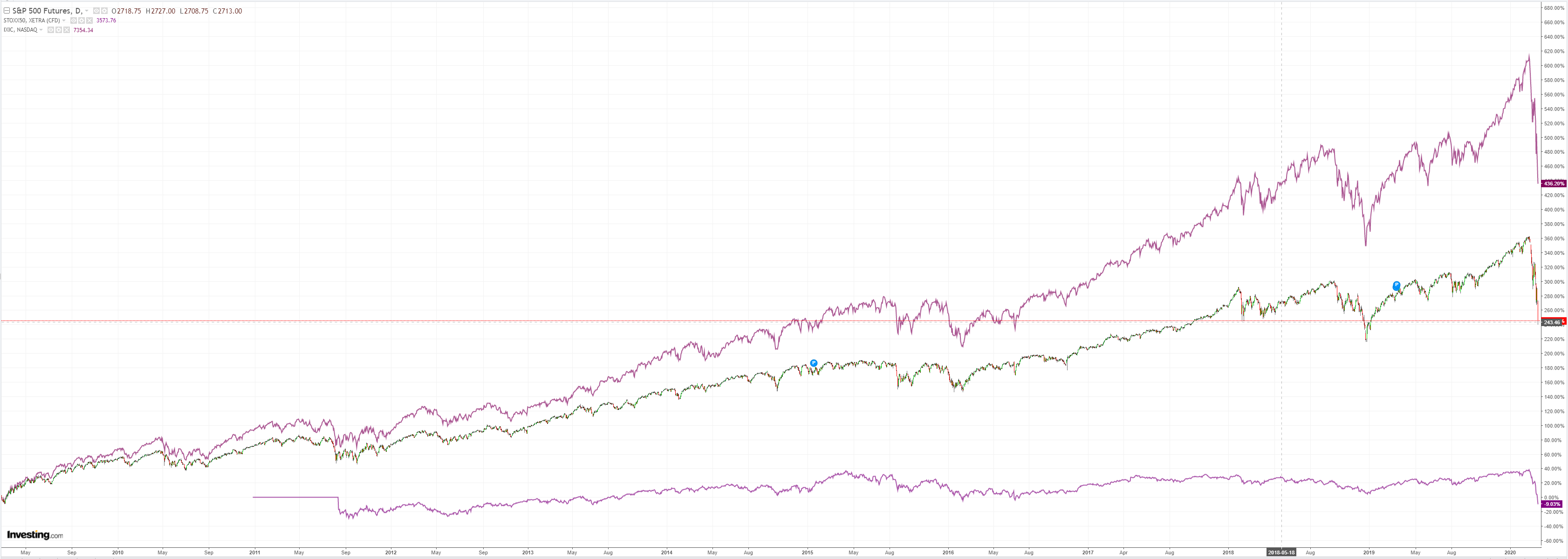

Stocks crashed but remain so very high:

Markets crashed. The ECB unleashed QE176:

At today’s meeting the Governing Council decided on a comprehensive package of monetary policy measures:

(1) Additional longer-term refinancing operations (LTROs) will be conducted, temporarily, to provide immediate liquidity support to the euro area financial system. Although the Governing Council does not see material signs of strains in money markets or liquidity shortages in the banking system, these operations will provide an effective backstop in case of need. They will be carried out through a fixed rate tender procedure with full allotment, with an interest rate that is equal to the average rate on the deposit facility. The LTROs will provide liquidity at favourable terms to bridge the period until the TLTRO III operation in June 2020.

(2) In TLTRO III, considerably more favourable terms will be applied during the period from June 2020 to June 2021 to all TLTRO III operations outstanding during that same time. These operations will support bank lending to those affected most by the spread of the coronavirus, in particular small and medium-sized enterprises. Throughout this period, the interest rate on these TLTRO III operations will be 25 basis points below the average rate applied in the Eurosystem’s main refinancing operations. For counterparties that maintain their levels of credit provision, the rate applied in these operations will be lower, and, over the period ending in June 2021, can be as low as 25 basis points below the average interest rate on the deposit facility. Moreover, the maximum total amount that counterparties will henceforth be entitled to borrow in TLTRO III operations is raised to 50% of their stock of eligible loans as at 28 February 2019. In this context, the Governing Council will mandate the Eurosystem committees to investigate collateral easing measures to ensure that counterparties continue to be able to make full use of the funding support.

(3) A temporary envelope of additional net asset purchases of €120 billion will be added until the end of the year, ensuring a strong contribution from the private sector purchase programmes. In combination with the existing asset purchase programme (APP), this will support favourable financing conditions for the real economy in times of heightened uncertainty.

The Governing Council continues to expect net asset purchases to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.

(4) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

(5) Reinvestments of the principal payments from maturing securities purchased under the APP will continue, in full, for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Only to be trumped by the Fed launching QE4:

The Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York has released a new monthly schedule of Treasury securities operations and has updated the current monthly schedule of repurchase agreement (repo) operations. Pursuant to instruction from the Chair in consultation with the FOMC, adjustments have been made to these schedules to address temporary disruptions in Treasury financing markets. The Treasury securities operation schedule includes a change in the maturity composition of purchases to support functioning in the market for U.S. Treasury securities. Term repo operations in large size have been added to enhance functioning of secured U.S. dollar funding markets.

- As a part of its $60 billion reserve management purchases for the monthly period beginning March 13, 2020 and continuing through April 13, 2020, the Desk will conduct purchases across a range of maturities to roughly match the maturity composition of Treasury securities outstanding. Specifically, the Desk plans to distribute reserve management purchases across eleven sectors, including nominal coupons, bills, Treasury Inflation-Protected Securities, and Floating Rate Notes. The distribution of purchases across sectors will be the same distribution as the Desk uses to reinvest principal payments from the Federal Reserve’s holdings of agency debt and agency MBS in Treasury securities. The first such purchases will begin tomorrow, March 13, 2020.

- Today, March 12, 2020, the Desk will offer $500 billion in a three-month repo operation at 1:30 pm ET that will settle on March 13, 2020.

- Tomorrow, the Desk will further offer $500 billion in a three-month repo operation and $500 billion in a one-month repo operation for same day settlement.

- Three-month and one-month repo operations for $500 billion will be offered on a weekly basis for the remainder of the monthly schedule.

- The Desk will continue to offer at least $175 billion in daily overnight repo operations and at least $45 billion in two-week term repo operations twice per week over this period.

These changes are being made to address highly unusual disruptions in Treasury financing markets associated with the coronavirus outbreak. Reserve management purchases into the second quarter will continue to be conducted with this maturity allocation. The terms of operations will be adjusted as needed to foster smooth Treasury market functioning and efficient and effective policy implementation.

Neither did much to calm markets. But both did help keep the Australian dollar higher than it should be.

Meanwhile, from Martin Place, ZZZZZZZZZZZZZZZzzzzzzzzzzzzzzzzzzzz…..

So, what can I say? We predicted it. Now it is here. What next?

More of the same with a much lower Australian dollar as the RBA eventually wakes up.