Some welcome news for LNG producers as the spike in the oil price flows through to the gas price for many Australian producers due to contracts struck over a decade ago. However, it is a short term gain only, the LNG market is highly competitive and only going to get more competitive going forward – and the current major disconnect between oil and gas prices will likely accelerate the trend. The big issues for LNG are:

- There is significant export competition coming

- US economics will cap LNG prices

- Australia has a perverse sensitivity to gas prices

There is significant export competition coming

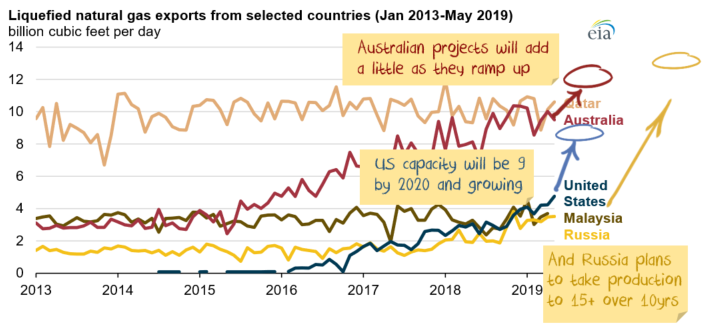

Australia is about to be the world’s largest exporter of LNG, but how long that mantle is maintained will be kept is anyone’s guess as projects in the US and Russia come online:

Advertisement

Until recently the US has been unable to export gas. Since the export ban was removed a host of LNG trains have been built and more are coming.