…Labor’s proposed franking ‘scale-back’ also makes the near-term return of excess franking credits more attractive. Figure4 ranks the franking balances of companies relative to market capitalisation in the ASX150. Among the large caps, BHP Group and Rio Tinto have already announced off-market buybacks. Our survey of UBS analysts highlights that Woolworths and Wesfarmers are the most likely to surprise with off-market buybacks / capital returns in 2019.

Yep – no disagreement from me. My take is that Australian companies try to get rid of franking credits as fast as they can as franking credits are of no use to the company and are useful for shareholders. It makes sense to make sure that any excess franking credits have been used up prior to Labors changes.

We had a detailed look at Labor’s changes in a four-part series a few months ago (see here).

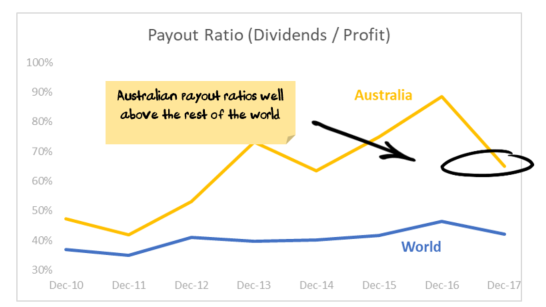

We highlighted the differences in payout ratios between Australian and World companies go away after you consider buybacks:

Advertisement

Source: Factset, Nucleus Wealth

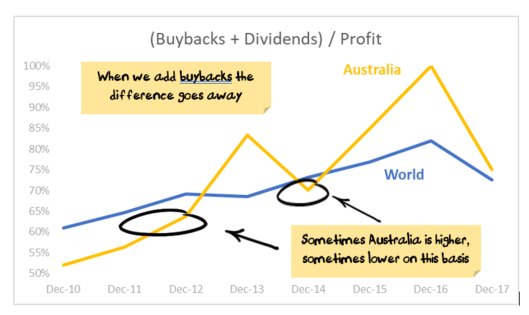

However, this is only half of the story… …companies return capital to shareholders through dividends or buybacks, and when you add the two together the difference between Australia and the rest of the world goes away:

Source: Factset, Nucleus Wealth

This indicates that the total payments to shareholders is similar for Australian companies vs the rest of the world – it is just that Australian companies tend to use dividends rather than buy backs.

The conclusions we drew were that the changes to franking credits would make little difference to Australian company’s preference to use dividends rather than buybacks – but UBS do make a good point that there will be a one-off rush to clear franking credits off balance sheets prior to the new rules being implemented.

Other conclusions we had:

Advertisement

Franking credits have distorted the Australian capital allocation, with a distinct preference for higher payout ratios in Australia and fewer buybacks.

However, this is at worst a neutral outcome, and probably a good discipline for Australian companies.

Franking credits are at least partially responsible for the stunted development of Australia’s corporate debt market.

Franking credits have been good for tax receipts, and support investment in Australia by domestic companies.

Labor’s changes are relatively minor, unlikely to make much difference to any of the above.

——————————–

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.