Australia you’ve been conned, hoodwinked by APRA to ensure that the too big to fail taxpayer guarantee of Mega Bank (CBA, NAB, ANZ and WBC) continues unabated. Another example of the game of mates, where APRA gains by pointing to a job well done on system stability, even while the risk rests squarely on the shoulders of those who can least afford it. Whilst Bankers benefit by being able to drive credit creation, high returns on equity and exorbitant bonuses. A cosy cabal indeed.

On 19 July 2017 APRA released an Information Paper entitled “Strengthening banking system resilience – establishing unquestionably strong capital ratios”. A document which is meant to set capital standards and requirements that, in accordance with the Financial System Inquiry’s recommendation, substantially reduces taxpayer risk to the financial system by making banks “unquestionably strong”. In meeting this standard the Information Paper is a work of pure fiction.

Capital requirements are very important for many reasons besides the protection against losses (“unquestionably strong”). Whilst a bank’s weighted cost of capital and debt increases as the amount of capital increases (there is some academic debate on this), the much bigger implications are in Mega Bank’s ability to grow which is ever more limited by larger the capital requirements. Whilst banks can create money simply by lending, they can’t just create the capital to support the lending risk. As a bank grows credit it needs to raise capital and this must come from retained earnings or externally raised. As credit grows Bankers do not like to continually raise capital as it dilutes return on equity, a negative feedback loop that can maintain system stability if capital requirements are sufficient.

I believe that APRA should be subject to intense scrutiny on its Information Paper due to the immense importance to the Australian taxpayer. Sadly, except for a few mumbles from some market analysts, it would appear that no one is going to do the work. So I’ll try and shed some light.

APRA’s requirements for Mega Bank and Macquarie which use the Internal Rating-Based (“IRB”) approach to capital adequacy is as follows:

“….., APRA has concluded that it will be necessary to raise minimum capital requirements by the equivalent of around 150 basis points from current levels to achieve capital ratios that would be consistent with the goal of ‘unquestionably strong’”

Well, when APRA said 150 basis points, they actually meant for Mega Bank:

“In the case of the four major banks, APRA expects that the increased capital requirements will translate into the need for an increase in CET1 capital ratios, on average, of around 100 basis points above their December 2016 levels. In broad terms, that equates to a benchmark for CET1 capital ratios, under the current capital adequacy framework, of at least 10.5 per cent.

100 basis points or 1% of extra capital (CET1) doesn’t sound much to get to “unquestionably strong”. No wonder the market reacted positively. So how did APRA decide that a CET1 ratio of 10.5% (or an increase of roughly 10%) for Mega Bank would make them unquestionably strong?

APRA firstly states its system goal:

“The nature of the business of ADIs is risk-taking. In establishing standards that will generate unquestionably strong capital ratios, the goal should be to further reduce the risk of failure of an ADI, and thereby the risk of a call on taxpayer support, but stop short of attempting to eliminate this risk altogether. In other words, unquestionably strong capital ratios should not seek to remove, or be perceived as removing, the risk of ADI failure.”

It’s in this statement or goal that we have the first of many problems. Where you have a well diversified financial system with many independent banks, I would agree with APRA’s goal. In Australia we do not have that diversity. We have Mega Bank that with its four divisions dominates market share with at least 80% share in all banking segments.

If a division of Mega Bank were to fail, in all likelihood Mega Bank fails. In these circumstances isn’t it more appropriate that Mega Bank is calibrated so that the risk of failure is eliminated? Besides protecting the taxpayer, wouldn’t this also encourage the creation of more banks that by default may allow some smaller banks to fail but create system stability?

In determining the actual capital/CET1 ratio APRA refers to a number of comparisons that it uses.

- International capital comparisons

- Rating Agencies

- Stress Tests

- Leverage Ratio

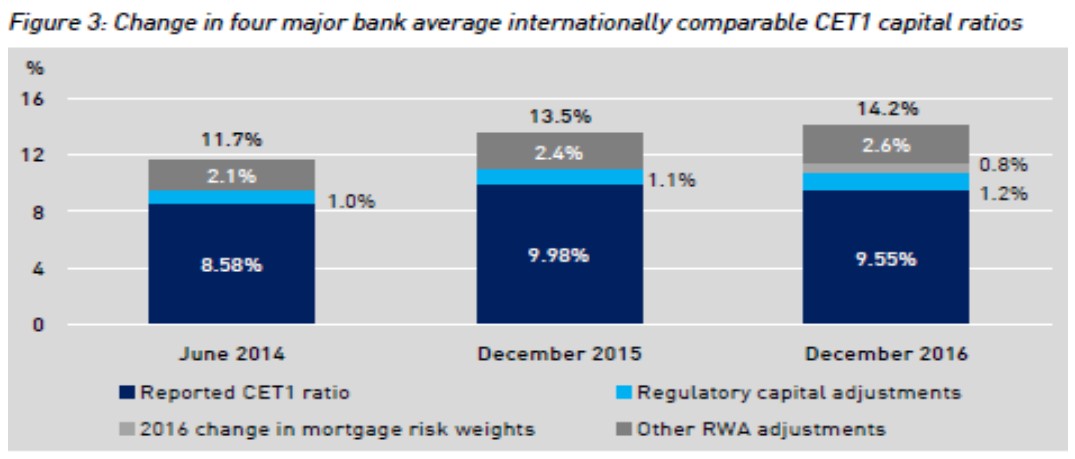

In comparing Mega Bank internationally APRA refers to the July 2015 paper, International capital comparison study. Using this study, APRA made adjustments due to its “conservative implementation of the Basel Committee’s framework”, as follows:

“These adjustments resulted in internationally comparable CET1 capital ratios approximately 300 basis points higher than the ratios calculated under the APRA standards applying at that time.”

A 300 basis point capital credit is absolutely massive especially compared to APRA’s extra capital requirement of 100 basis point. I and a number of others have debunked APRA’s comparison paper previously and I do not have the space to do that again. Except to point out that differences in definition of capital may have some validity and that accounts for 100 basis points. The other 200 basis points relates to IRB models which are impossible to compare between banks unless of course you had all the models which APRA does not.

I must admit that I have been struggling for years to get my head around what APRA, the ABA and PwC have been writing on this topic. Are they making capital adjustments on how Mega Bank would be regulated by say the PRA in the UK, or, if APRA were replaced by the PRA in the UK? The Basel II methodology is supposed to allow international comparisons. Notwithstanding the fact that if APRA are making adjustments to Basel requirements and then readjusting when determining unquestionably strong capital requirements, what the hell were the purposes of the adjustments in the first place?

But let’s use APRA’s own words to point to the study’s fallibility.

APRA are setting capital standards that are “UNQUESTIONABLY” strong. How then could APRA use its comparison study when it says in the study:

“……. both the FSI and APRA have noted that a direct comparison of banks’ capital adequacy ratios across jurisdictions is challenging. There is no single, internationally-harmonised measure of capital adequacy that is publicly available.”

Apparently international bank comparisons that are challenging with no measure publicly available leads to “unquestionable” benefits for Mega Bank.

Figure 3 below clearly shows the illusory capital that APRA and Mega Bank have created. Note dark and light grey. Fake capital?

Let’s move to APRA’s Rating Agency comparison. For this APRA turns to the discredited S&P.

“APRA has considered analysis based on S&P’s risk-adjusted capital (RAC) ratio, which S&P uses as an input in assessing the capital adequacy of a bank. This ratio differs from the Basel framework calculation of regulatory capital ratios and so provides an alternative means of assessing capital strength”

So what did that produce?

“The latest published average RAC ratio of the four major banks was 9.3 per cent, producing a capital strength assessment of ‘adequate’.”

What, “not unquestionably strong”?

Well actually, APRA adjusted the analysis. “APRA has adopted an economic risk score of 3 for the purposes of its analysis.” Whilst S&P assessed “Australia’s current economic risk score of 4 is representative of a heightened risk environment,”. APRA’s adjustment allowed Mega Bank to be in the “strong” range.

I’d suggest at this stage that APRA are struggling on the unquestionable front.

Next we turn to APRA’s stress tests of Mega Bank. APRA uses a 2 year old stress test.

“The results of APRA’s 2015 ADI stress test indicated that the four major banks’ CET1 capital ratios, on average, would be eroded by in the order of 350 basis points during the stress event”.

APRA concluded that “a major bank’s capital ratio eroded in the order of 350 basis points, a bank would need an operating CET1 capital ratio in the range of 10 to 11 per cent in normal times” consistent with APRA’s recommended increase as noted above. APRA believe that with a CET1 ratio of 8% after a stress event that Mega Bank would be able to operate as normal.

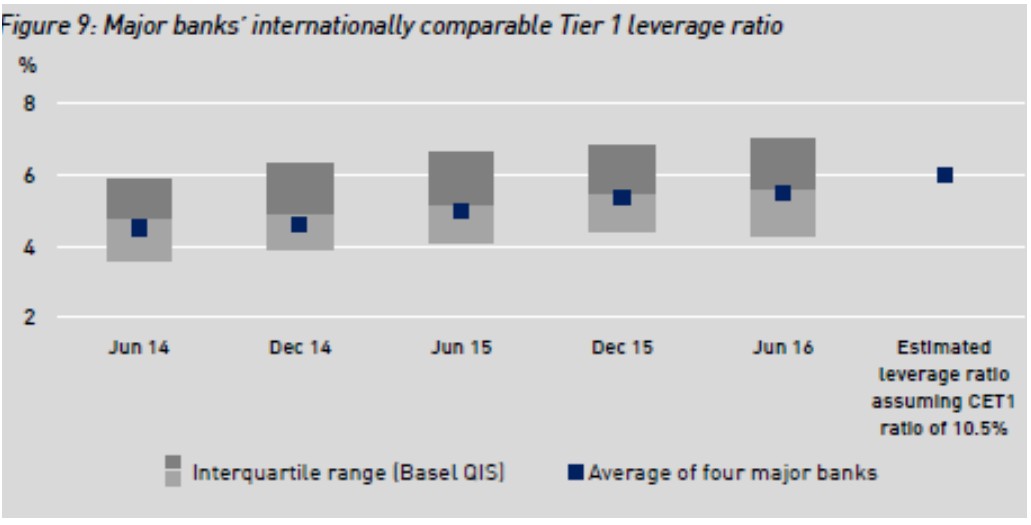

The conclusion I believe is questionable. Firstly the markets view of risk weighted assets would certainly have changed after any stress event certainly forcing extra capital to be raised (taxpayer funded?). More importantly is the leverage ratio discussed below. After APRA’s stress event, Mega Bank would have a leverage ratio of 2.5% or be geared 40 times based on assets. Would Mega Bank be able to operate normally on that ratio without significant capital injection. The answer is certainly not, unquestionably so.

Mega Bank sits at just below the median on the leverage ratio. Not top quartile but below half the bank’s international peers.

Figure 9 demonstrates the point.

Nevertheless we are fed this gem from APRA.

“As a large proportion of assets in the Australian banking system are residential mortgages, which benefit from lower risk-weights relative to other types of lending, the reported leverage ratios of Australian ADIs will generally be expected to be lower than those of overseas counterparts, all else being equal “

APRA may be partly correct on that statement but it’s unlikely to be correct on also adjusting risk weights on its international comparisons for residential mortgages on the basis that APRA requires higher risk weightings than international regulators on residential mortgages, all else being equal. I refer you to section 3.3.1 of APRA’s international comparison study.

It also should be noted that many international banking peers, especially in Europe, have large exposures to sovereign debt that has very low to zero risk weights. Perhaps APRA could have mentioned how this would decrease the risk weighted assets and therefore the leverage ratios of its peers?

Mega Bank is certainly not “unquestionably strong” based on international comparisons of leverage ratios.

APRA has made a very poor case for its actions in limiting Mega Bank’s added capital requirements to 100 basis points. The standard of “unquestionably” has been set by the FSI and adopted by the Government, the Australian people. Why is APRA so reluctant to enforce that standard? My view is that it’s this very question that allows APRA free reign. Why question APRA as they have no reason not be following the standard unquestionably?

APRA will act in their own interest. They have a responsibility for financial system stability – i.e. to protect the banks. If that’s best done via implied tax payer guarantees then so be it. They have promoted themselves historically as a strong regulator, when they’re just average. Any significant increases in capital requirements would show that they have been average.

Lastly, 80% of the financial system is with their mates at Mega Bank and as such is not in APRA’s interest to have an all out war with Mega Bank that perhaps a 300 basis point increase in capital may have. Besides, it’s just way too easy to fool the punters and the pollies.

To change the tone somewhat, someone at APRA sees the forest and indicates that matters may be changing significantly.

“The assumption that residential mortgages are relatively low-risk credit exposures, while generally appropriate when viewed at the level of individual loans, is open to challenge when the concentration of mortgage exposures within the overall balance sheet of the banking system is high and increasing, underwriting standards have become less stringent over time, and the capital framework does not adequately address this concentration…

A central element of the implementation approach for ‘unquestionably strong’ will therefore be strengthened capital requirements for residential mortgage lending. The design of these measures will seek to target higher risk lending, balanced against avoiding undue complexity in the prudential framework”

Mega Bank’s capital ratios may be unquestionably average but perhaps still on a path to “unquestionably strong”.