In a recent post I explained how home rents are mostly wasted spending arising from futile price-competition amongst potential tenants. I likened this to Richard Dawkins’ analogy of energy used to create tree trunks being waste from the perspective of the tree, because the only purpose of the trunk is to win the futile competition for sunlight through investment in height amongst a group of uncooperative forest trees.

I explained how tenants could instead cooperate, by unionising, and exert their bargaining power on landlords to cooperatively reduce rents. This post will look at some examples of how the rental canopy is lowered in practice, and how price-competition amongst tenants can be limited by well-written regulations.

The best place to start is wartime. Is such times economic efficiency is a priority, and laws and regulations that cut off wasteful competition are more easily passed.

Almost universally, strict rent controls were put in place across Europe, the US, and Australia, during the major 20th century wars. These had the effect of containing nominal rental prices despite inflationary pressures from the wartime economic build up. In terms of the primary objective of lowering the ‘rental canopy’, they worked very successfully.

Advertisement

In modern times the main approach to pruning the rental canopy is to enact tenancy laws that restrict the pricing power of landlords for existing tenants. Indeed, almost every wealthy country has laws that improve the bargaining position of tenants, with government agencies tasked with ensuring there is full cooperation amongst tenants, and that landlords cannot sidestep these protective laws. They do this, because it works. It reduces rental prices. Even economists know this.

“It is possible to design a set of rent regulations that results in an improvement in efficiency over the unrestricted market equilibrium”

In France, tenancies are secured with automatic rollover of leases and limits on rent increases set by the L’Indice de Référence de Loyers (IRL), which is currently the consumer price index excluding rent and tobacco. In Germany, tenancies are secured in a similar way, with rental increases limited to local conditions, such as to a maximum of 15% over three years in Munich. In Denmark, there are four different rental control systems, all of which ensure tenant security and limit landlord’s power to increase rents. In all cases, tenant security is assured because landlords must justify the reason for asking a tenant to leave, even when the lease is expired, with very few reasons made acceptable by law, such as extensive renovation, or occupation by the landlord (summaries of European rental laws are here).

Such rules avoid the situation where landlords try to severely hike the rent at the lease expiry, and, if the tenants cannot pay, force them to leave. In the absence of legal protections, landlords are able to squeeze out existing tenants and get new ones at market prices, forcing more tenants into futile price competition with each other. Even the mere threat of this power means that existing tenants are often forced to meet the market price each year. The ‘market’ outcome is that the landlord has all the bargaining power.

In Australia, this situation is the norm. Landlords can increase rents without limit after each contract, typically one year, and ask tenants to leave without any reason at lease expiry.

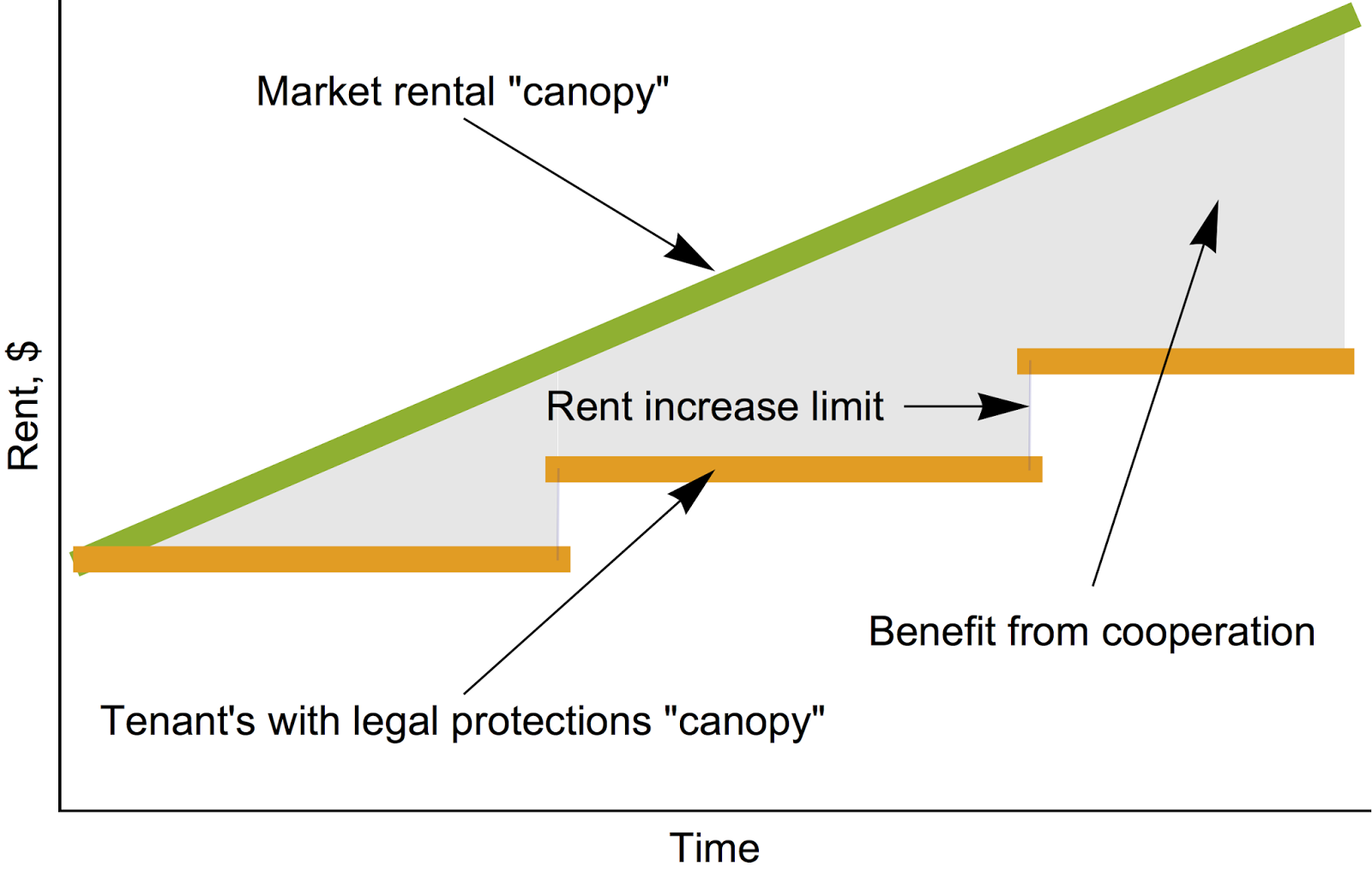

The graph below gives an idea of how limits on rental increases and a secure rental tenure system can result in tenant paying below market rents. This occurs over time if the rental increase limit is below the growth rate of local market prices. The total value of the benefit from these laws for this example tenant is shaded in grey. For society as a whole, the benefit is the sum for all tenants of the difference in the actual rental price paid to the market rental price.

How big could the gains for Australian renters be if we adopted similar tenancy laws to what is fairly standard n Europe? Let us take the situation of secure tenant rights and coupled with limiting rental price increases to CPI.

In Sydney for example, the housing component of CPI has increased 55% in the past decade, while the CPI itself has only increased 25%. In Melbourne it is 51% and 25%, and Brisbane it is 50% and 30%. With these figures in mind, a realistic rental price saving of 20% on market prices is possible for long term tenants in the major capitals.

With $60 billion in total housing rents paid to landlords each year, even small rental savings across a small share of tenants results in big savings. If just one quarter of tenants made a 20% saving on market rental price, that would amount to $3 billion per year saved. If half of tenants made those savings, that’s $6 billion.

The security given by these tenant protections also means that tenants are able to invest in improving the property – with curtains, lights, gardens and other beautification projects – without fear of losing there investment because they will soon be forced to leave. Indeed, unlike Australia, tenants are often obliged to bring their own curtains, lights, and sometimes kitchens, when they rent a new home in countries with such well-established tenant protection laws.

Adopting world’s best tenancy rights would undermine futile rental-price competition and be a $3 billion win for Australian tenants.