Angus Nicholson for Chris Weston, Chief Market Strategist at IG Markets

The release of the Fed minutes overnight largely confirmed that there will not be a rate rise in April, and there’s little in the statement or recent US data that pushes strongly for a rate rise in June either. The Department of Energy report took the lead from the API report and saw the first decline in crude oil inventories since the beginning of February. The collective effect was a renewed swoon in the USD and the continuation of a two-day rally in oil. These have been the dominant forces in Asia today that helped see energy and materials sectors perform strongly across the region.

Initially, this news was greeted positively early in Asian trade, but the region’s concern soon returned to the impressive resurgence in the strength of the yen. The yen gained another 0.6% in Asian trade, and looked set to break the 109 level. Bank of Japan (BOJ) governor Kuroda did not use his speech today to jawbone some weakness into the yen. But there seems to be a growing consensus that the days of the USD/JPY above the 110 level may have come to an end. While further stimulus is expected from the BOJ at their meeting at the end of the month, the focus is likely to be directed at supporting the equity market and perhaps buying provincial bonds. The pressure to support the Japanese economy is increasingly falling to the government, which may push them to start opening up the fiscal coffers and actually push through meaningful structural reforms.

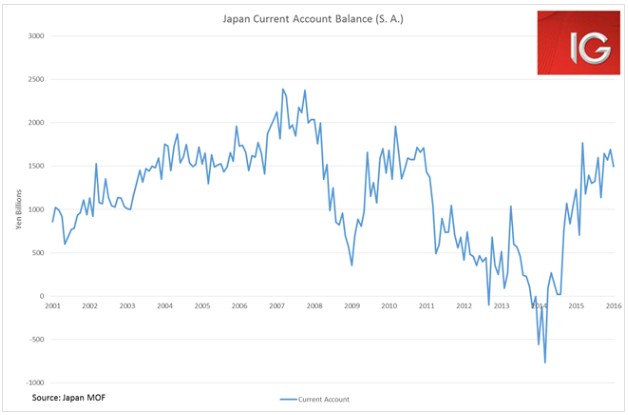

One of the reasons why the government and the BOJ may have eased up on their concerns about the strength in the currency is that they would be fighting a losing war against Japan’s strong current account balance, and also the steady influx of Japanese corporates repatriating their foreign earnings.

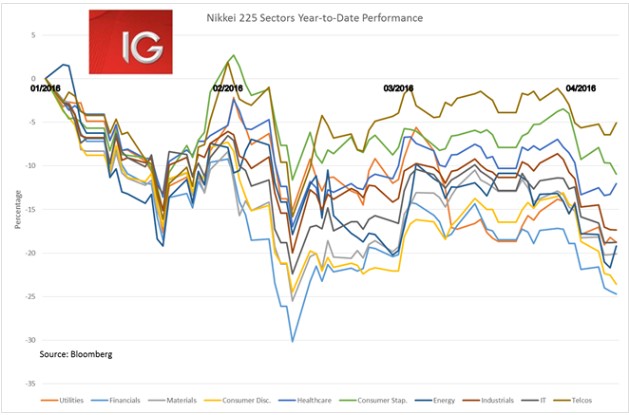

The Nikkei briefly looked like it was going to end its 7-day losing streak earlier in the session, but the further fall in the yen seems to have ended those prospects. It is a very mixed story of performance in the Nikkei, with its declines being dominated by the financial and consumer discretionary sectors, down 24.7% and 23.6% year-to-date, respectively. The telecommunications sector has comparatively outperformed, losing 5% year-to-date.

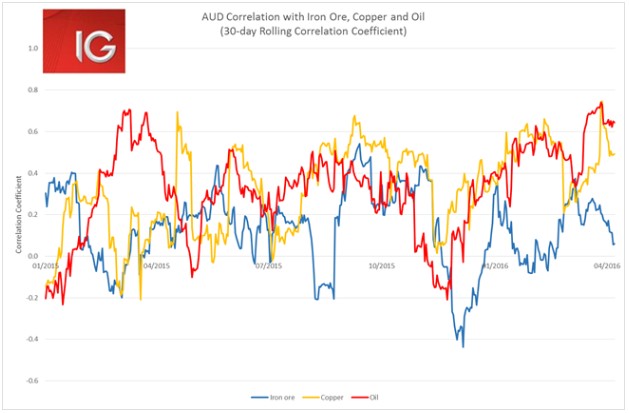

One of the most interesting aspects for Australian investors about the renewed surge in oil is what it means for the Aussie dollar. The Aussie dollar gained another 0.8% overnight as the oil price surged, and no doubt the US dollar sell off played a part in that as well. I’ve taken a little look at the which commodities the Aussie dollar is moving most closely alongside at the moment, and since the middle of March the Aussie’s daily moves have been most highly correlated with the oil price. The Aussie dollar has been far more correlated with the moves in the oil price than either moves in copper or iron ore prices. Certainly, this something to keep an eye on in the lead up to the oil producers meeting in Doha on 17 April. A large jump in the oil price in the event of some sort of deal could also see a similar move in the Aussie dollar.